- United States

- /

- Metals and Mining

- /

- NYSE:SXC

Exploring Undiscovered Gems in the United States This December 2024

Reviewed by Simply Wall St

The United States market has remained flat over the past week but has seen a significant 32% rise over the past year, with earnings projected to grow by 15% annually. In this dynamic environment, identifying undiscovered gems involves finding stocks that demonstrate strong potential for growth and resilience amidst fluctuating market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Franklin Financial Services | 173.21% | 5.55% | -1.86% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Parker Drilling | 46.25% | -0.33% | 53.04% | ★★★★★★ |

| Morris State Bancshares | 17.84% | 4.83% | 6.58% | ★★★★★★ |

| Omega Flex | NA | 0.39% | 2.57% | ★★★★★★ |

| Teekay | NA | -3.71% | 60.91% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.65% | 11.17% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 7.11% | -35.88% | ★★★★★☆ |

| Pure Cycle | 5.31% | -4.44% | -5.74% | ★★★★★☆ |

| FRMO | 0.13% | 19.43% | 29.70% | ★★★★☆☆ |

We'll examine a selection from our screener results.

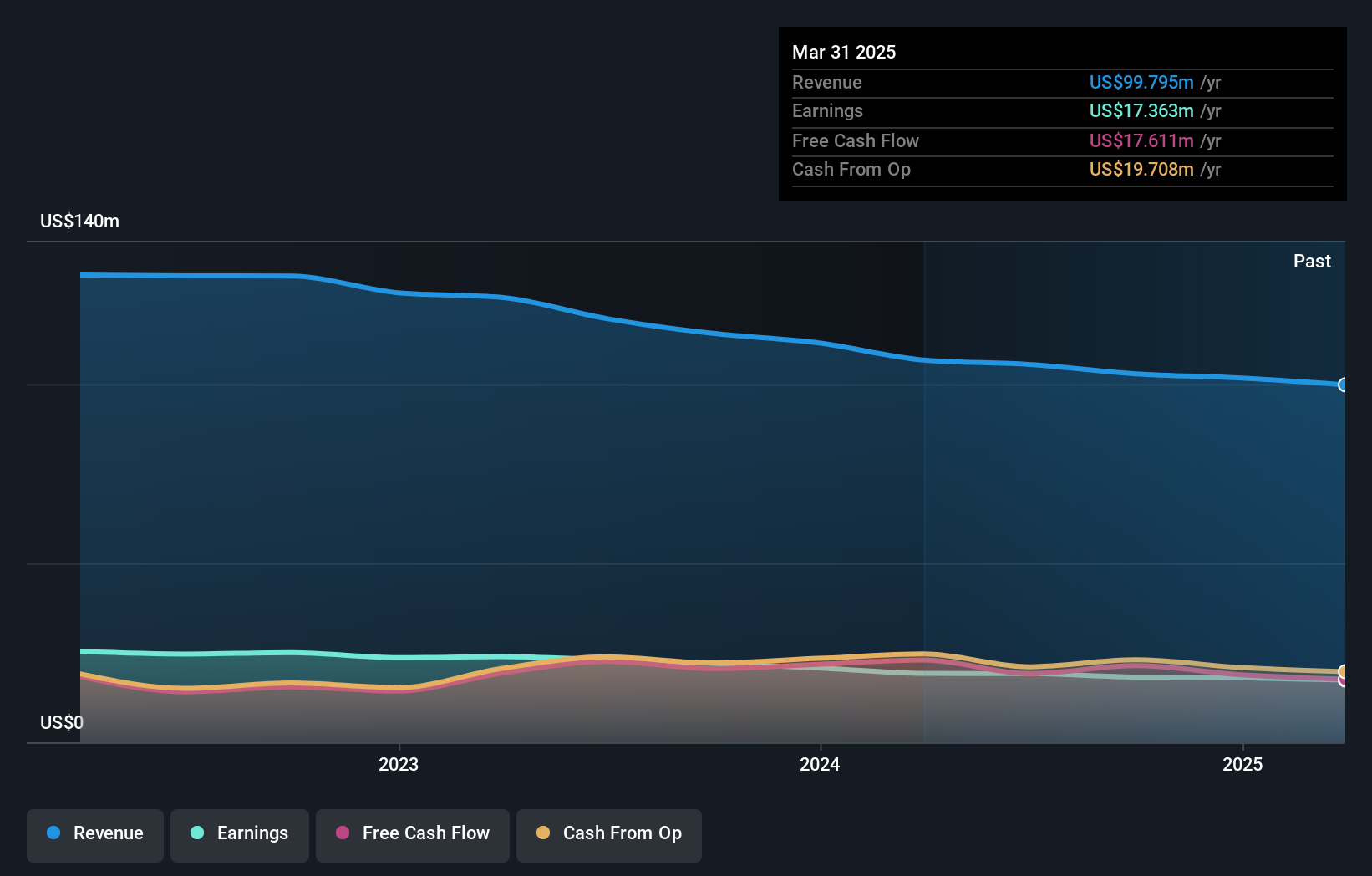

Omega Flex (NasdaqGM:OFLX)

Simply Wall St Value Rating: ★★★★★★

Overview: Omega Flex, Inc. manufactures and sells flexible metal hoses and accessories both in North America and internationally, with a market capitalization of approximately $498.86 million.

Operations: Omega Flex generates revenue primarily from the manufacture and sale of flexible metal hoses and accessories, amounting to $102.86 million. The company's financial performance is highlighted by its net profit margin, which reflects its ability to convert sales into profit efficiently.

Omega Flex, a nimble player in the machinery sector, has been debt-free for five years, highlighting its strong financial position. Despite this strength, it faced a challenging year with earnings growth at -17.4%, contrasting sharply with the industry average of 11.5%. For the third quarter of 2024, sales reached US$24.88 million and net income was US$4.62 million; both figures were lower than the previous year’s results at US$27.5 million and US$5.58 million respectively. The company trades at about 10% below its estimated fair value while maintaining high-quality earnings and positive free cash flow, suggesting potential undervaluation amidst current market conditions.

- Click here to discover the nuances of Omega Flex with our detailed analytical health report.

Explore historical data to track Omega Flex's performance over time in our Past section.

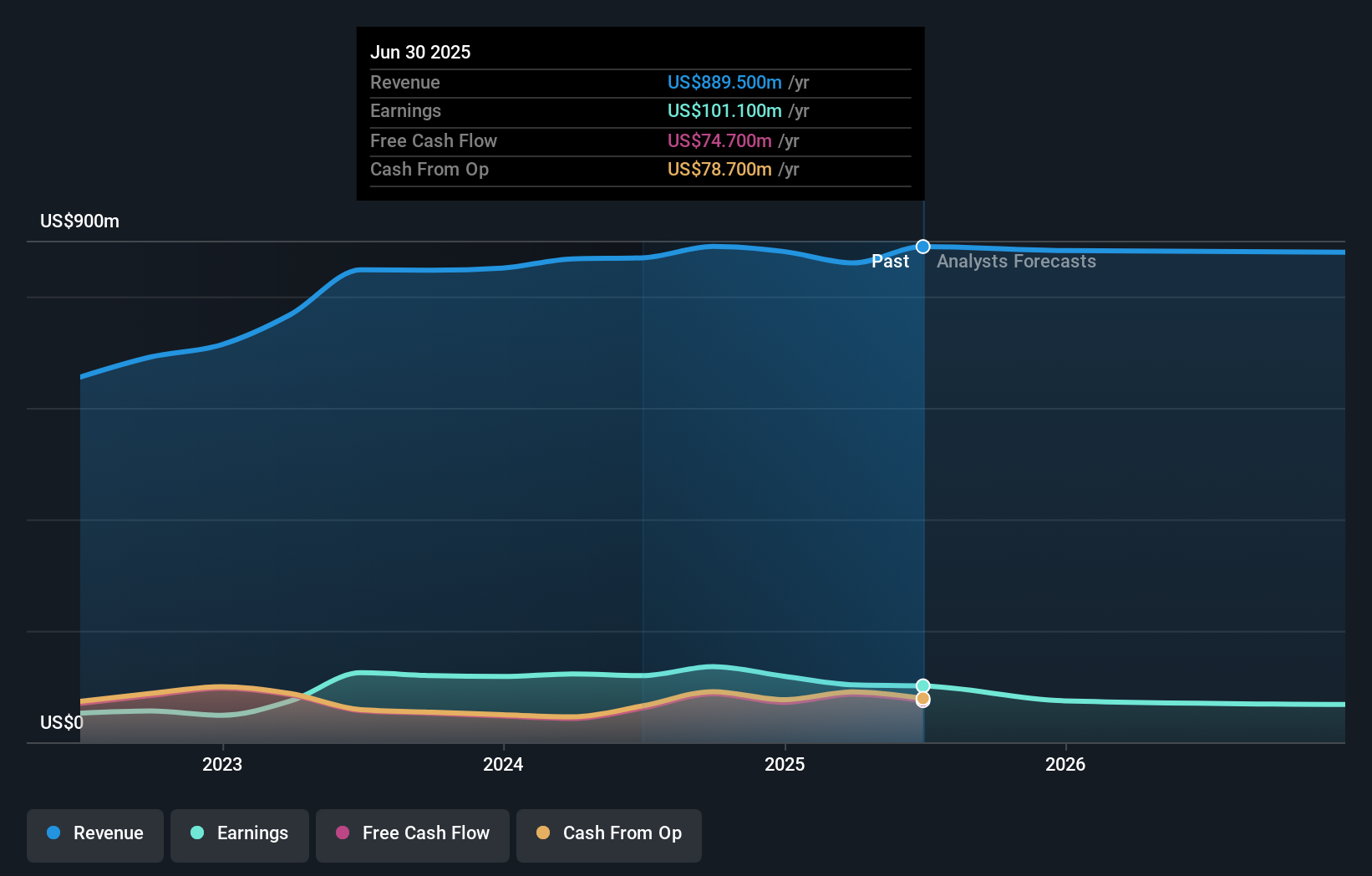

Employers Holdings (NYSE:EIG)

Simply Wall St Value Rating: ★★★★★☆

Overview: Employers Holdings, Inc. operates in the commercial property and casualty insurance industry in the United States with a market capitalization of approximately $1.32 billion.

Operations: Employers Holdings generates revenue primarily from its insurance operations, totaling $889.80 million. The company's financial performance is reflected in its net profit margin, which stands at 14.27%.

Operating in the commercial property and casualty insurance sector, Employers Holdings is a small player with no debt on its books. The company recently reported third-quarter revenue of US$224 million, up from US$203.5 million a year prior, and net income of US$30.3 million compared to US$14 million previously. Despite being 60% below fair value estimates, analysts foresee challenges with shrinking profit margins expected to drop from 15% to 8%. While earnings growth was strong historically, recent buybacks totaling over 1.5 million shares for US$61.39 million suggest strategic moves amidst industry volatility concerns.

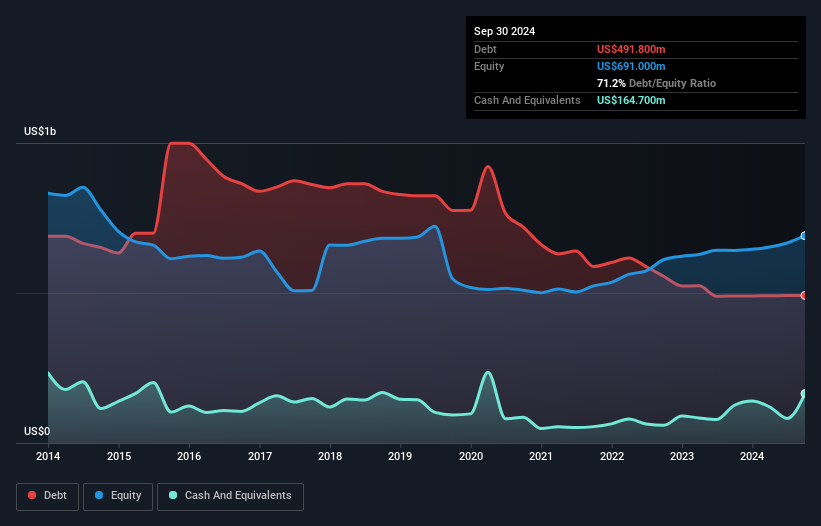

SunCoke Energy (NYSE:SXC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: SunCoke Energy, Inc. is an independent producer of coke with operations in the Americas and Brazil, and has a market capitalization of approximately $1.05 billion.

Operations: SunCoke Energy generates revenue primarily from its Domestic Coke segment, contributing $1.85 billion, and Logistics segment, adding $102.80 million. The Brazil Coke segment provides an additional $35.60 million in revenue.

SunCoke Energy, a player in the metals and mining sector, has shown impressive earnings growth of 55% over the past year, outpacing industry peers. Despite this, its net debt to equity ratio stands at a high 47.3%, although it has decreased from 141.7% over five years. The company’s interest coverage is robust at six times EBIT, reflecting solid financial management amidst high debt levels. Recent developments include a $12 million expansion in logistics capacity and favorable regulatory changes likely to enhance net margins. Trading below fair value by about 29%, SunCoke presents both opportunities and challenges for investors.

Taking Advantage

- Access the full spectrum of 231 US Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SXC

SunCoke Energy

Operates as an independent producer of coke in the Americas and Brazil.

Good value with proven track record and pays a dividend.