Advertisement

- United States

- /

- Household Products

- /

- NasdaqGS:WDFC

WD-40 (NASDAQ:WDFC) Will Pay A Larger Dividend Than Last Year At $0.88

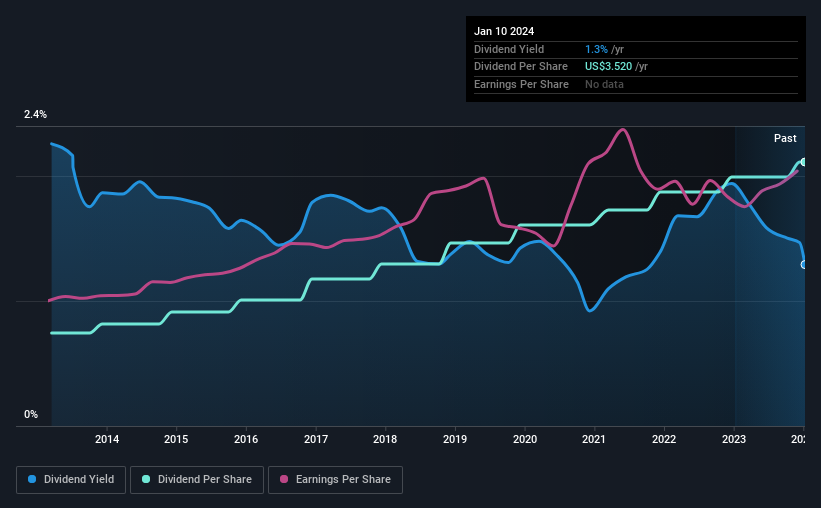

WD-40 Company (NASDAQ:WDFC) has announced that it will be increasing its dividend from last year's comparable payment on the 31st of January to $0.88. This takes the annual payment to 1.3% of the current stock price, which unfortunately is below what the industry is paying.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that WD-40's stock price has increased by 37% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

View our latest analysis for WD-40

WD-40's Dividend Is Well Covered By Earnings

Even a low dividend yield can be attractive if it is sustained for years on end. Prior to this announcement, WD-40's dividend was comfortably covered by both cash flow and earnings. This means that a large portion of its earnings are being retained to grow the business.

Looking forward, earnings per share is forecast to rise by 27.2% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 57%, which is in the range that makes us comfortable with the sustainability of the dividend.

WD-40 Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2014, the dividend has gone from $1.24 total annually to $3.52. This works out to be a compound annual growth rate (CAGR) of approximately 11% a year over that time. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

Dividend Growth May Be Hard To Achieve

Investors could be attracted to the stock based on the quality of its payment history. Unfortunately, WD-40's earnings per share has been essentially flat over the past five years, which means the dividend may not be increased each year. Growth of 1.6% may indicate that the company has limited investment opportunity so it is returning its earnings to shareholders instead. This isn't bad in itself, but unless earnings growth pick up we wouldn't expect dividends to grow either.

WD-40 Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Companies that are growing earnings tend to be the best dividend stocks over the long term. See what the 3 analysts we track are forecasting for WD-40 for free with public analyst estimates for the company. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if WD-40 might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:WDFC

WD-40

Develops and sells maintenance products, and homecare and cleaning products in North America, Central and South America, Asia, Australia, Europe, India, the Middle East, and Africa.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor