Advertisement

- United States

- /

- Household Products

- /

- NasdaqGS:WDFC

A Look at WD-40 (WDFC) Valuation Following Strong Earnings Growth and Improved Financial Momentum

Simply Wall St

Reviewed by Simply Wall St

WD-40 (WDFC) posted its fourth quarter and full-year earnings, reporting higher sales and net income compared to last year. Earnings per share climbed for both periods, which signals ongoing financial progress for the company.

See our latest analysis for WD-40.

WD-40’s latest financials appear to have provided a modest boost in sentiment, with the share price rising 1.2% over the past day and 5.5% over the week. Still, recent momentum has yet to change the longer-term picture. The stock’s total shareholder return sits at -22.6% for the year, offset by a strong 33.4% gain over three years. This reminds investors that WD-40’s performance can swing with broader market cycles and investor expectations.

If solid results have you wondering what other resilient companies might be out there, now's a great moment to broaden your investing horizons and discover fast growing stocks with high insider ownership.

With shares rebounding in the short term but still down significantly over the past year, investors may be wondering whether WD-40 is undervalued after its latest results, or if the market is already pricing in all future growth potential.

Most Popular Narrative: 27.6% Undervalued

WD-40's current share price of $200.98 sits noticeably below the widely-followed analyst fair value estimate of $277.50. The stage is set for bold expectations, with financial assumptions that break away from recent performance trends. Let’s look at a key catalyst that underpins this valuation perspective.

The company's focus on premiumization of products, with targets for a compound annual growth rate for premium products exceeding 10%, is poised to improve net margins by shifting the product mix towards higher-margin offerings.

What is the hidden lever behind this price target? Premium products. The narrative's valuation hinges on ambitious profit mix shifts and a premiumization push far beyond the company's historical averages. Want to see which financial forecasts and margin moves give this estimate its edge? The full story is just a click away.

Result: Fair Value of $277.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks remain, including uncertainty around WD-40’s planned divestitures and volatility from foreign currency shifts. These factors could pressure future earnings and margins.

Find out about the key risks to this WD-40 narrative.

Another View: What Do Multiples Say?

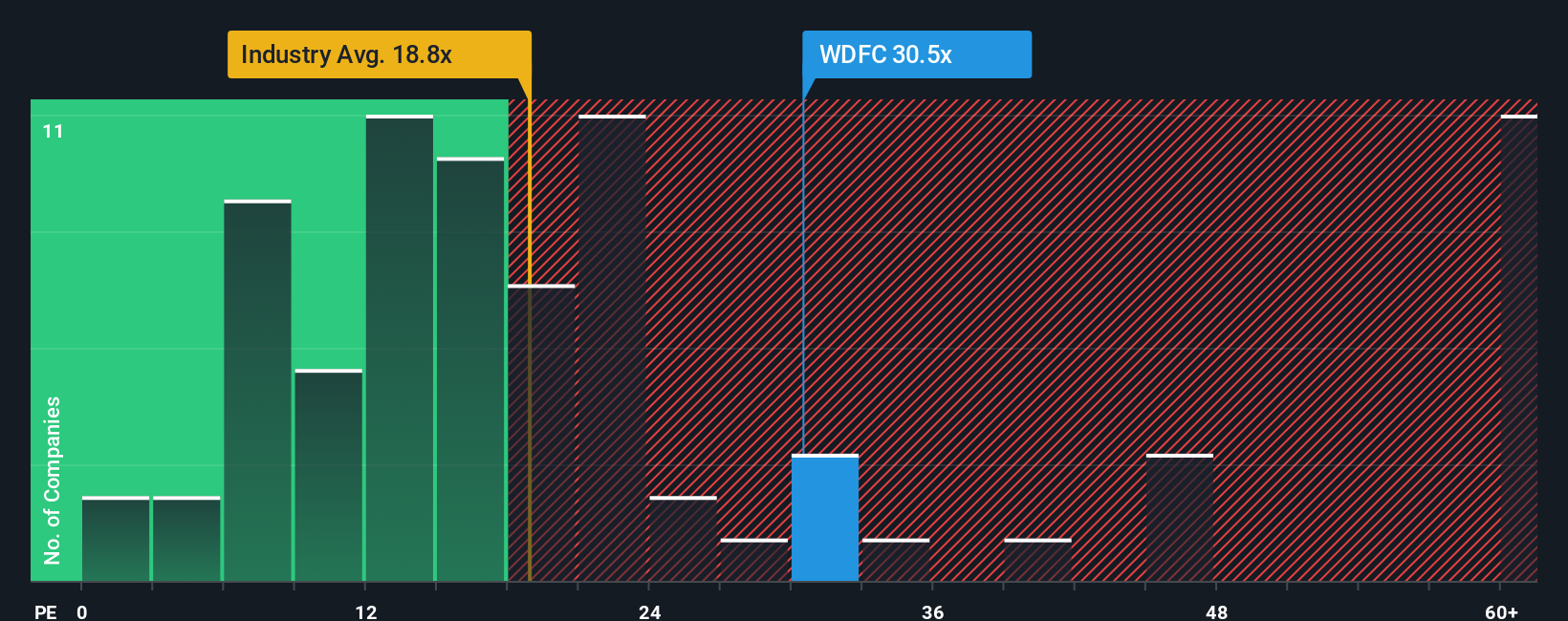

While analyst forecasts point to WD-40 being undervalued, the company's price-to-earnings ratio tells a different story. At 31.5x, it is more than double the industry average of 14.8x and well above the fair ratio of 16.3x, suggesting investors are paying a premium. Could this make the shares riskier if growth stumbles?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own WD-40 Narrative

If you see these numbers differently, or would rather dig into the details on your own, know that building a custom narrative is quick and easy. Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding WD-40.

Looking for More Investment Ideas?

Expand your portfolio with handpicked stocks tailored to your interests. Act now, because the best opportunities won't wait for the hesitant investor.

- Start building tomorrow’s gains by focusing on steady income streams in the market with these 17 dividend stocks with yields > 3% offering yields above 3%.

- Tap into sectors at the forefront of medical technology by researching these 33 healthcare AI stocks for innovation-driven companies powering the future of healthcare.

- Unleash the potential of cutting-edge digital assets by analyzing these 80 cryptocurrency and blockchain stocks shaping the world of decentralized finance and blockchain technology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if WD-40 might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WDFC

WD-40

Develops and sells maintenance products, and homecare and cleaning products in North America, Central and South America, Asia, Australia, Europe, India, the Middle East, and Africa.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor