Advertisement

- United States

- /

- Pharma

- /

- NasdaqCM:VERU

Veru (NASDAQ:VERU) Has Us Worried With Its Last Reported Debt Levels

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Veru Inc. (NASDAQ:VERU) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Veru

What Is Veru's Net Debt?

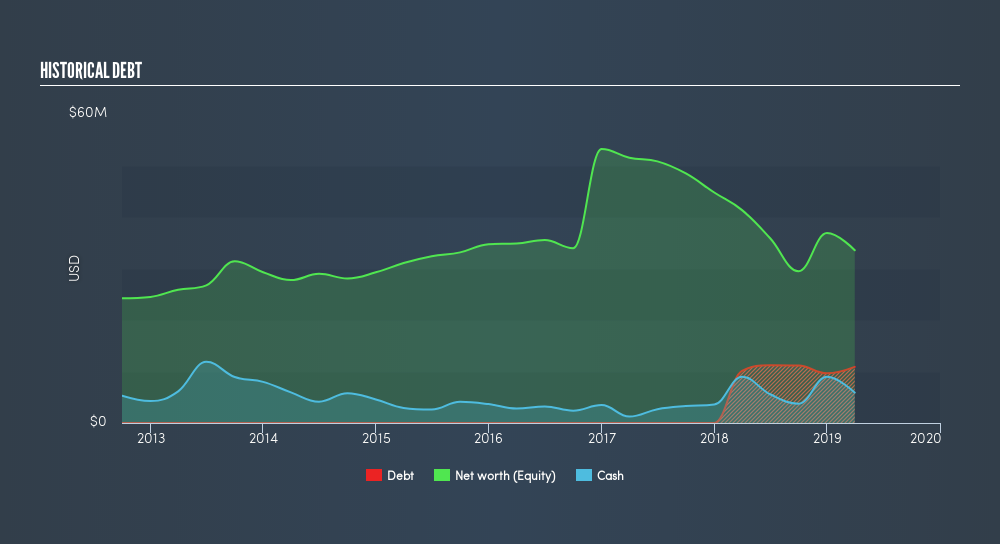

As you can see below, at the end of March 2019, Veru had US$10.9m of debt, up from US$10.1m a year ago. Click the image for more detail. However, because it has a cash reserve of US$5.90m, its net debt is less, at about US$5.00m.

A Look At Veru's Liabilities

According to the last reported balance sheet, Veru had liabilities of US$11.3m due within 12 months, and liabilities of US$6.20m due beyond 12 months. Offsetting these obligations, it had cash of US$5.90m as well as receivables valued at US$4.03m due within 12 months. So its liabilities total US$7.54m more than the combination of its cash and short-term receivables.

Given Veru has a market capitalization of US$135.0m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Because it carries more debt than cash, we think it's worth watching Veru's balance sheet over time. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Veru can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Veru managed to grow its revenue by 83%, to US$24m. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

While we can certainly savour Veru's tasty revenue growth, its negative earnings before interest and tax (EBIT) leaves a bitter aftertaste. To be specific the EBIT loss came in at US$11m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$11m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Veru insider transactions.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqCM:VERU

Veru

A late clinical stage biopharmaceutical company, focuses on developing medicines for treatment of metabolic diseases, oncology, and viral-induced acute respiratory distress syndrome (ARDS).

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor