Honest Company (HNST) stock has seen modest movement lately, with a 1-day gain of just under 1%. Investors are likely keeping a close watch on overall performance and recent trends as the company seeks to grow in a competitive sector.

Even with recent volatility, Honest Company's 1-year total shareholder return of -9.3% fares better than its steep 49.8% year-to-date share price decline. This suggests long-term holders have experienced less pain compared to short-term traders. Recent weakness might signal shifting sentiment or questions around future growth.

With Honest Company shares trading far below recent highs and showing some positive financial metrics, investors must ask whether there is overlooked value here or if the market is fully pricing in the company's growth prospects.

Advertisement

Most Popular Narrative: 49.8% Undervalued

Honest Company's widely followed narrative sets its fair value far above the current share price, signaling a potential gap between market sentiment and growth forecasts.

The company is capitalizing on the accelerating shift towards natural and clean-label products, evident from strong growth in sensitive skin, fragrance-free, and natural baby personal care items. This positions Honest to benefit from increasing consumer demand and supports future revenue expansion.

Want to know how bold projections for future profits and margins justify this aggressive upside? The narrative's pricing relies on crucial growth assumptions and a premium multiple. Which single metric lifts the valuation toward this high target? Click to see the full financial playbook behind the numbers that fuel market optimism.

However, slowing growth in core categories and continued exposure to tariff risks could challenge Honest Company's ability to sustain long-term revenue and margin expansion.

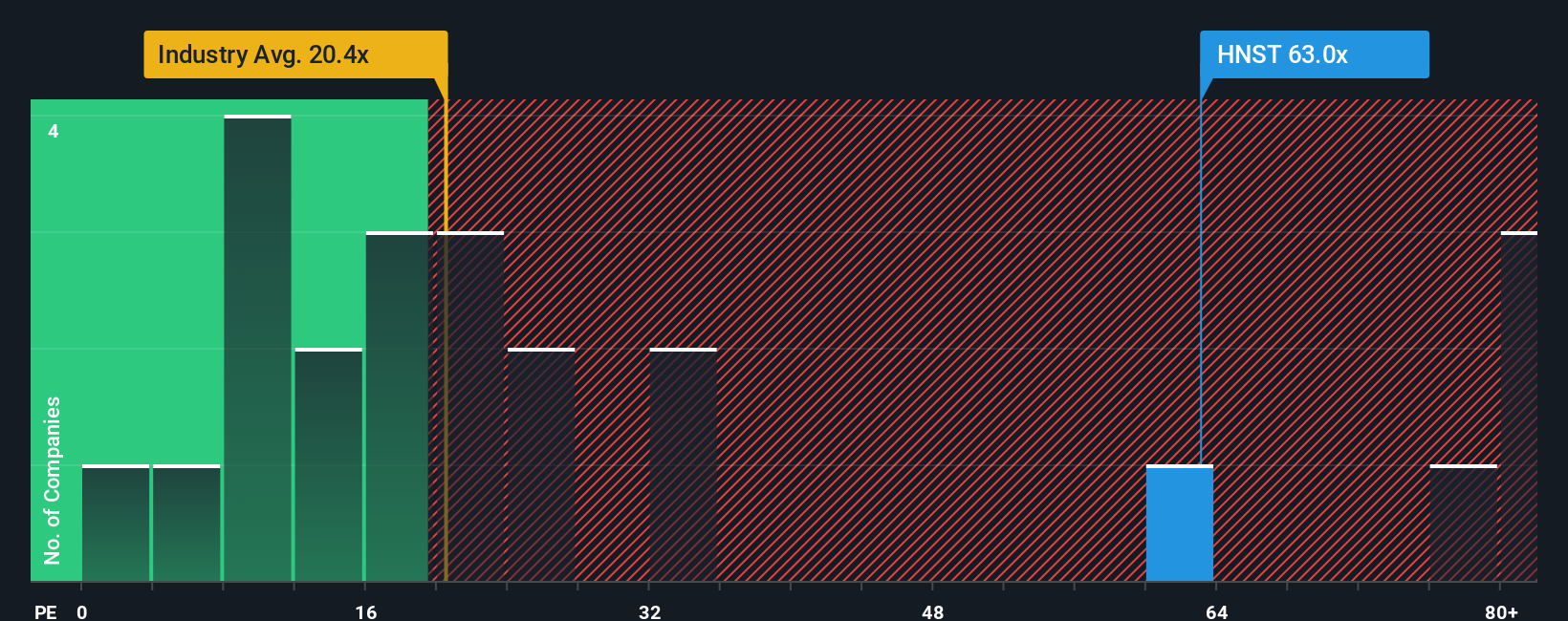

While analysts see Honest Company as potentially 49.8% undervalued, industry ratios suggest a different story. Shares trade at a price-to-earnings ratio of 58.6x, which is much higher than the Personal Products industry average of 19.4x, the peer average of 14x, and the fair ratio of 19.7x. This large gap could mean a greater risk of a market re-rating or a missed value opportunity, depending on whether those high multiples are justified. How should investors interpret this disconnect?

If you think the story looks different based on your research or want to run the numbers your own way, you can easily craft a narrative yourself in just a few minutes. Do it your way

A great starting point for your Honest Company research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more smart investment ideas?

You’re only seeing part of the opportunity. Widen your scope with carefully selected stocks that can boost your results well beyond Honest Company’s story.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Honest Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.