Advertisement

- United States

- /

- Medical Equipment

- /

- NYSE:SYK

Is Stryker’s Innovation Enough to Support Its Current Share Price in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious whether Stryker’s current share price is a bargain, fully valued, or overpriced? Let’s explore what is currently driving interest in the stock.

- Stryker’s stock has increased 1.1% in the past week and 0.7% over the last month, contributing to a modest 3.8% gain year-to-date. However, it remains down 4.2% compared to the same period last year.

- Recent headlines highlight Stryker’s ongoing innovation in medical technology and recent strategic acquisitions. These developments have sparked discussion about the potential for future growth and market expansion, influencing how investors evaluate both the opportunities and risks associated with the stock.

- Stryker currently scores a 0 out of 6 on our undervalued checklist. This raises important questions about how to value a high-quality healthcare name like this and points to an alternative approach to valuation that will be discussed at the end of the article.

Stryker scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Stryker Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a business is worth by projecting its future cash flows and discounting them back to today's value. For Stryker, this approach models the company's ability to generate cash over time, using both analyst estimates for the next several years and longer-term projections.

Stryker's current Free Cash Flow is approximately $4.1 billion. Analysts forecast steady growth, with Free Cash Flow expected to reach about $5.9 billion by 2028. Beyond five years, the forecast is extended based on moderate growth assumptions, resulting in FCF projections of over $7.2 billion in ten years. All projections are expressed in US dollars.

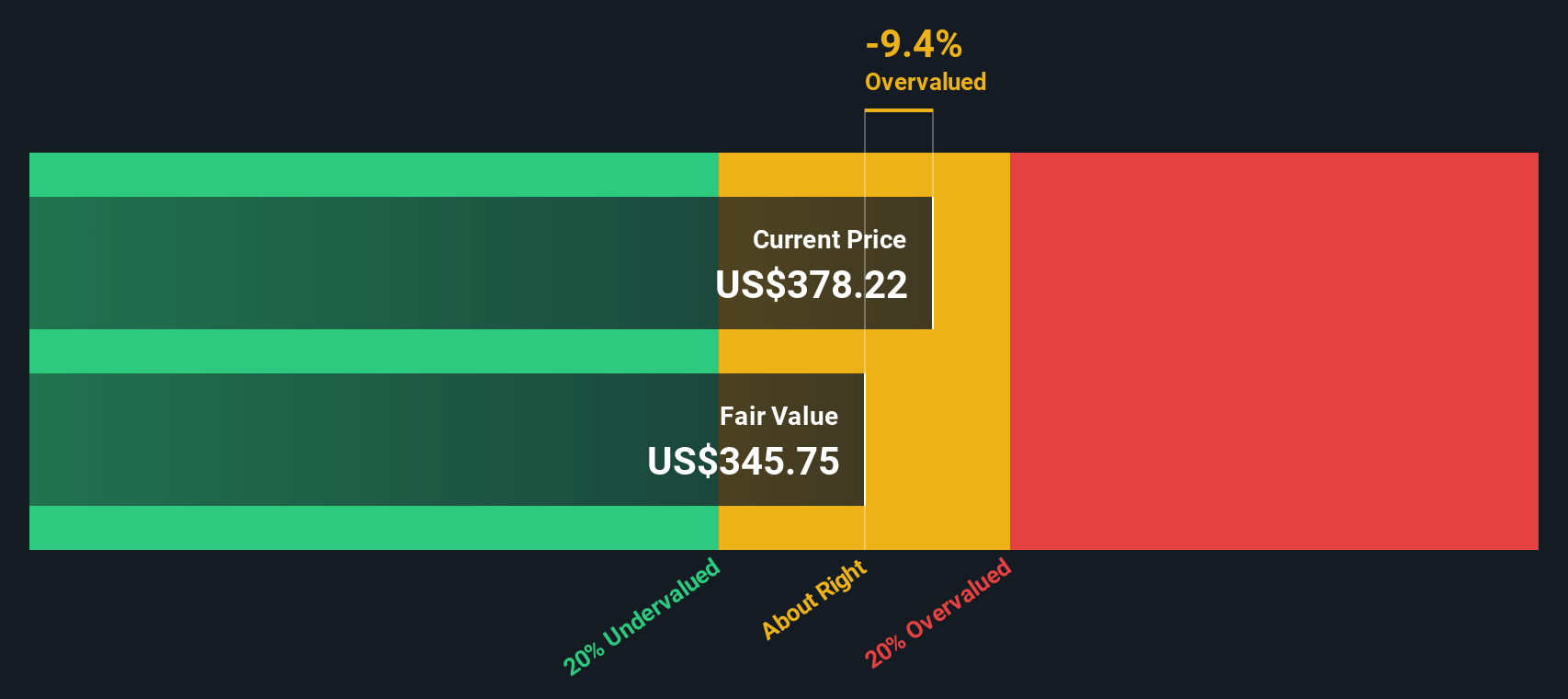

After discounting these cash flows back to present value, the DCF model estimates Stryker's intrinsic value at $300.25 per share. Compared to the current trading price, this suggests the stock is 24.0% overvalued.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Stryker may be overvalued by 24.0%. Discover 922 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Stryker Price vs Earnings

The Price-to-Earnings (PE) ratio is widely considered the most useful valuation tool for consistently profitable companies like Stryker. It allows investors to see how much they are paying for each dollar of reported earnings, which is especially important for established businesses generating reliable profits.

What makes a “fair” PE ratio is shaped by expectations for future earnings growth and the perceived risks of a company’s industry. High growth prospects and lower risk typically justify a higher PE, while slower-growing or riskier businesses should command a lower multiple.

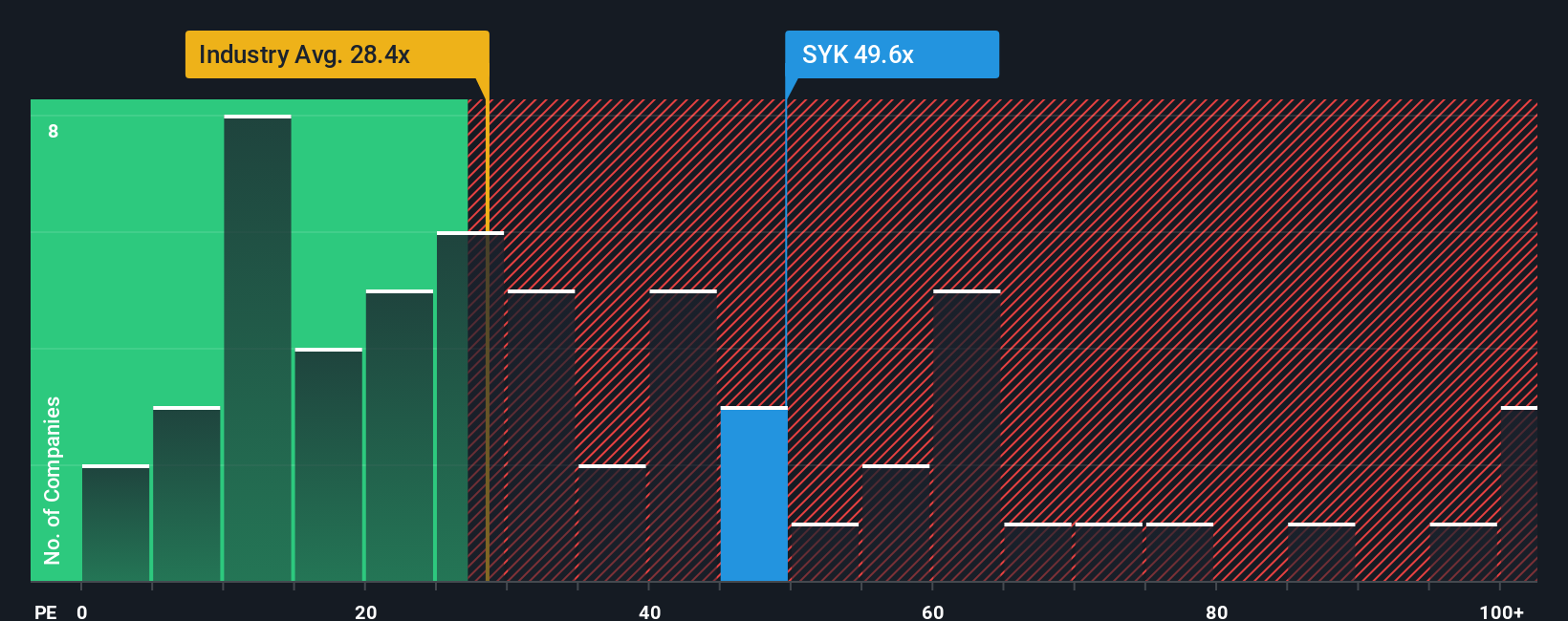

Currently, Stryker trades at a PE ratio of 48.4x. This not only sits well above the Medical Equipment industry average of 28.9x, but also exceeds the average for its direct peers, which sit at 43.0x. On the surface, this suggests Stryker is trading at a premium to both its sector and its competitors.

However, Simply Wall St’s "Fair Ratio" goes a level deeper. This proprietary metric forecasts what a reasonable PE multiple should be, based on Stryker’s unique mix of growth outlook, profitability, risks, market cap, and industry dynamics. Unlike simple peer or industry comparisons, the Fair Ratio offers a more holistic assessment of value that is grounded in the company’s specific fundamentals.

For Stryker, that Fair Ratio stands at 37.6x. This is notably below the current PE, indicating Stryker is priced above what its financial profile and growth prospects might otherwise justify.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Stryker Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative puts your own story and perspective around a company, letting you decide what you think Stryker’s future could hold and connect those beliefs to specific numbers like fair value, future revenue, earnings, and profit margins.

Think of a Narrative as a clear link between Stryker’s story, the business facts you care about, and the resulting value. You choose the catalysts that matter, estimate future performance, and see how your view compares to the market price. This approach makes it easy for everyone, not just analysts, to map out their view and track it over time via the Narratives tool on Simply Wall St’s Community page, which is trusted by millions of investors.

Narratives are designed to help you make smarter buy or sell decisions by putting your estimated Fair Value side by side with the latest market Price, and they refresh automatically as new earnings reports, news, or risks emerge. This ensures your view is always current.

For example, some investors see Stryker’s fair value as high as $465, focusing on its innovation and global expansion, while others set it as low as $316 due to risks such as regulatory delays and pricing pressures.

Do you think there's more to the story for Stryker? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SYK

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative