Advertisement

- United States

- /

- Medical Equipment

- /

- NYSE:STE

STERIS (STE): Evaluating Valuation After Recent Share Price Surge

Simply Wall St

Reviewed by Simply Wall St

STERIS (STE) has caught the attention of investors after its shares climbed nearly 13% over the past month. With ongoing demand for infection prevention solutions, recent trading activity points to renewed market interest in the company’s steady revenue growth and expanding healthcare footprint.

See our latest analysis for STERIS.

Zooming out, STERIS has notched an impressive 31.5% share price return so far this year, with its momentum especially strong over the last month. While the total shareholder return comes in at 22.8% over the past year, investors are clearly responding to a sustained track record of growth and recent optimism around the healthcare sector.

Curious what else is trending in healthcare? Now is a smart time to check out See the full list for free.

Given this surge, investors face a crucial question: Is STERIS currently trading below its true value, or has the recent outperformance already priced in all of its promising future growth?

Most Popular Narrative: 5.4% Undervalued

With STERIS trading at $266.28, and the most widely followed narrative pointing to a fair value of $281.63, there is a notable gap between the current price and forecasted potential. This difference reflects positive expectations for future growth and stable earnings. It also sets a high bar for operational execution ahead.

Continued expansion of STERIS's consumables and services segments, with high recurring revenue and margin visibility, positions the company to benefit from increasing healthcare expenditures and adoption of best-practice infection control standards. This supports both revenue and margin expansion.

Want to know the formula the narrative uses to reach this fair value? One surprising growth driver stands out alongside ambitious profit projections. See what hidden tailwinds could justify paying a premium for this healthcare leader.

Result: Fair Value of $281.63 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, higher tariffs and shifting healthcare payment models could put pressure on STERIS's margins and growth, posing risks to the current optimistic outlook.

Find out about the key risks to this STERIS narrative.

Another View: Is Growth Already Priced In?

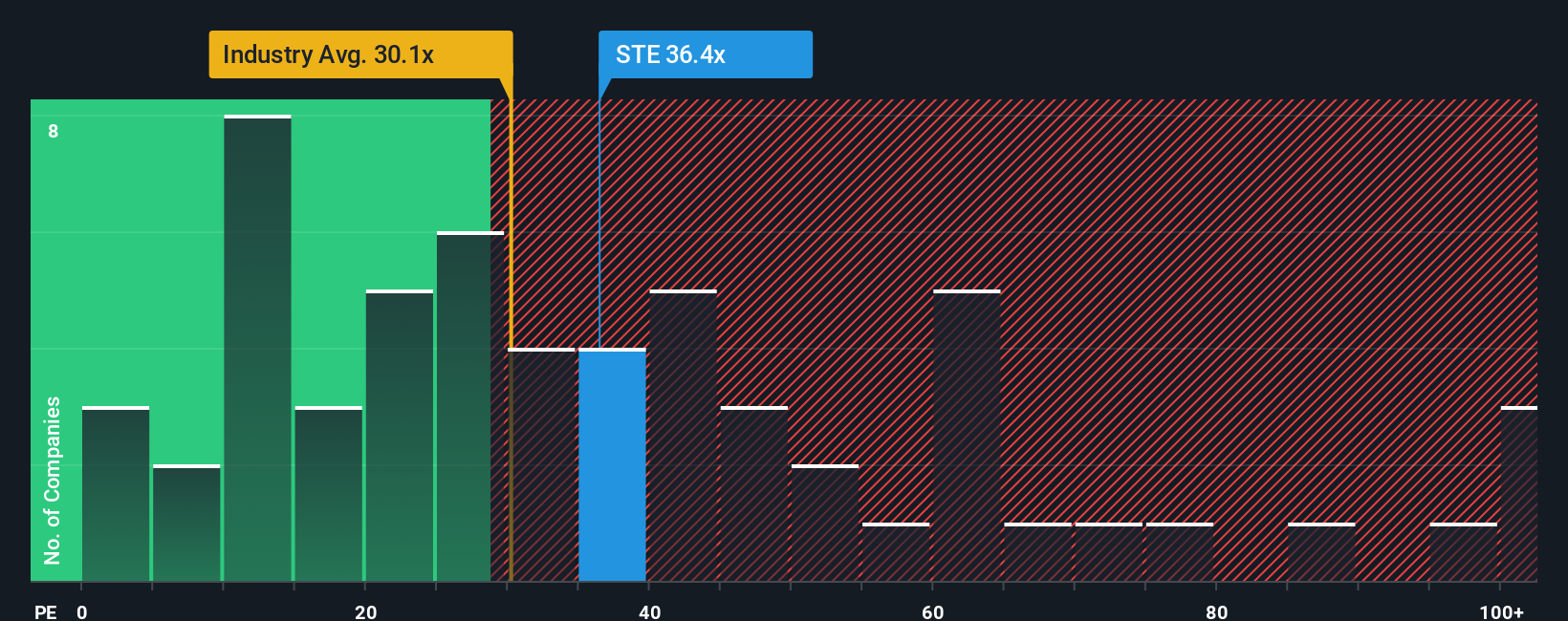

While the fair value model suggests STERIS is undervalued, a look at its price-to-earnings ratio paints a different picture. At 37.9x, STERIS trades much higher than peers at 25.2x and the industry average of 28.9x, and well above its fair ratio of 26x. This premium signals investors might already be paying up for much of the anticipated growth. So is there really room for more upside?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own STERIS Narrative

If you want to dig deeper, challenge the consensus, or add your own perspective, you can craft your own personalized outlook for STERIS in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding STERIS.

Looking for More Smart Investment Opportunities?

Don’t let today’s big gains distract you from fresh ideas that could boost your portfolio next. The right opportunity might be waiting, just a click away.

- Spot potential bargains and jump on these 920 undervalued stocks based on cash flows, where companies show real value based on their cash flow strength and market position.

- Tap into rapid innovation by checking out these 25 AI penny stocks, featuring businesses at the forefront of artificial intelligence breakthroughs that are transforming every industry.

- Unlock steady income potential when you review these 15 dividend stocks with yields > 3%, highlighting stocks with attractive yields and a solid history of rewarding investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:STE

Excellent balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative