- United States

- /

- Healthcare Services

- /

- NYSE:SEM

Is Select Medical (SEM) Undervalued After Recent Share Price Rebound?

Reviewed by Simply Wall St

Select Medical Holdings (SEM) has quietly outperformed the broader healthcare space over the past 3 months, even as the stock remains down sharply year to date. That mix of recent momentum and earlier weakness is exactly what catches valuation driven investors’ attention.

See our latest analysis for Select Medical Holdings.

At a share price of $15.01, the stock has clawed back some ground with a 30 day share price return of nearly 10 percent and an 18 percent gain over 90 days. However, that momentum still sits against a year to date share price decline of just over 20 percent and a negative 1 year total shareholder return, hinting that sentiment is improving from a low base rather than reflecting a fully rerated story.

If Select Medical’s rebound has you thinking about what else could be setting up for a turn, this is a good moment to explore healthcare stocks as potential next ideas.

With earnings growing faster than revenue, shares still below analyst targets and long term returns positive, investors now face a key question: Is Select Medical quietly undervalued or already reflecting its next leg of growth?

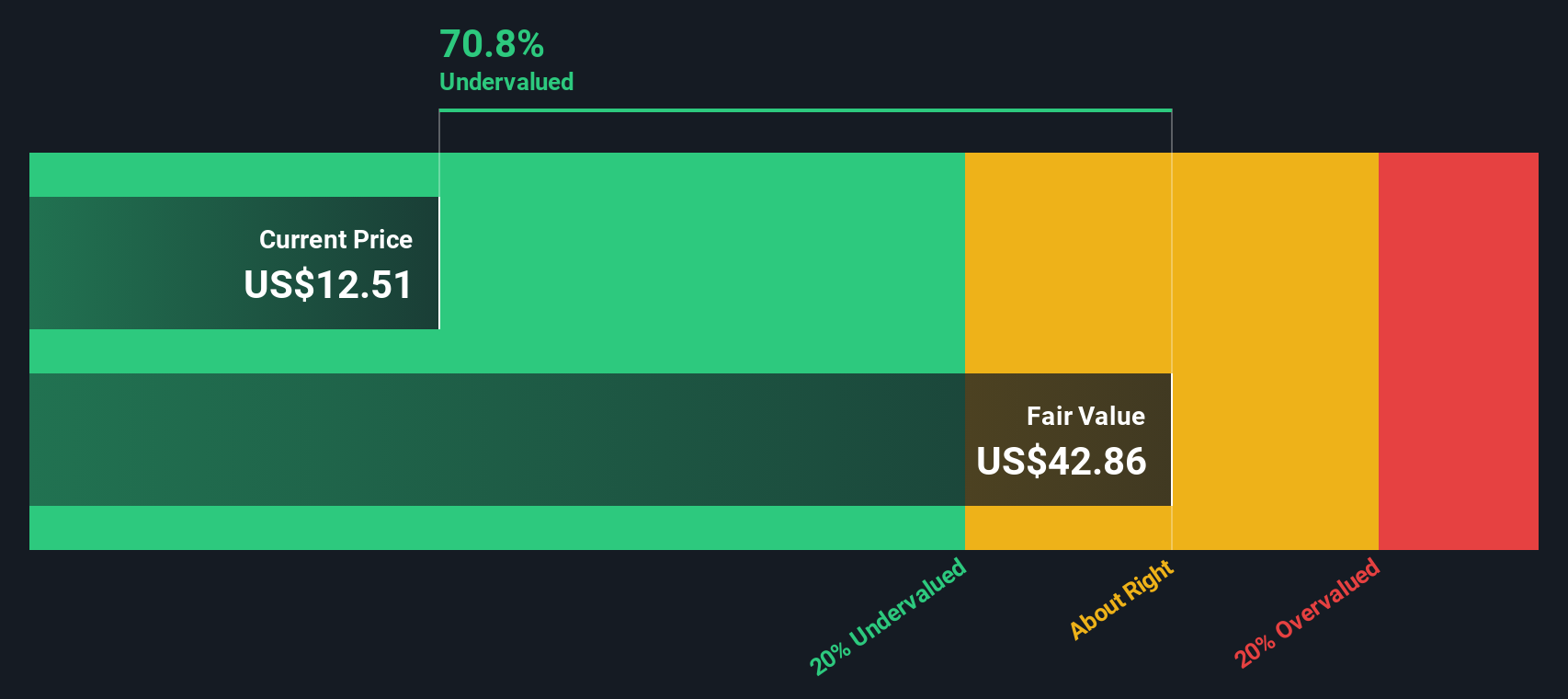

Most Popular Narrative: 15.8% Undervalued

With Select Medical Holdings last closing at $15.01 against a narrative fair value near the high teens, the gap points to meaningful upside if the story plays out.

Policy and payer shifts toward value based and cost effective care settings favor Select Medical's post acute and rehab offerings, potentially boosting occupancy rates and reducing earnings volatility as payers and hospitals increasingly steer patients to these lower cost, high quality care environments.

Curious how steady, mid single digit growth, rising margins and a leaner share count can still justify upside from here? The narrative hinges on a sharper earnings ramp than the past, a very specific future profit multiple and disciplined buybacks all working together. Want to see the exact financial path that backs this valuation gap?

Result: Fair Value of $18.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent Medicare reimbursement pressure and a heavy debt load could squeeze margins and cash flow. This may challenge the optimistic earnings ramp embedded in this valuation.Find out about the key risks to this Select Medical Holdings narrative.

Another Angle on Value

Our SWS DCF model is far less optimistic, suggesting fair value closer to $4.74, which would make today’s $15.01 share price look overvalued rather than cheap. If the cash flows do not ramp as expected, could the multiple led narrative be leaning too far ahead of reality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Select Medical Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 914 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Select Medical Holdings Narrative

If this view does not quite match your own, or you would rather dig into the numbers yourself, you can build a tailored narrative in just a few minutes: Do it your way

A great starting point for your Select Medical Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never rely on a single story, and you should not either. Use the Simply Wall Street Screener to uncover fresh opportunities before others notice them.

- Capitalize on mispriced potential by scanning these 914 undervalued stocks based on cash flows that may offer stronger upside than the market currently expects.

- Ride powerful technology trends by targeting these 24 AI penny stocks positioned to benefit from accelerating demand for intelligent automation.

- Strengthen your income strategy by reviewing these 12 dividend stocks with yields > 3% that can help support returns even when markets turn choppy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SEM

Select Medical Holdings

Through its subsidiaries, operates critical illness recovery hospitals, rehabilitation hospitals, and outpatient rehabilitation clinics in the United States.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion