Advertisement

- United States

- /

- Medical Equipment

- /

- NYSE:RMD

Is ResMed Stock Fairly Priced After Recent Regulatory Updates and Market Optimism?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering whether ResMed's current share price offers a real bargain or is already priced for perfection? You're not alone. Many investors are diving into the numbers seeking an answer.

- ResMed shares have climbed 4.1% over the last week and are up 11.6% year-to-date, but the ride hasn't been without a few dips, as seen in the -1.6% change over the past month.

- Recent news has focused on regulatory updates and healthcare industry innovations, helping to explain some of the recent moves in ResMed's stock price. For example, broader sector momentum and optimism around sleep apnea market adoption have also pushed sentiment higher.

- On our scoring system, ResMed earns a 4 out of 6 for undervaluation, suggesting there could be value here. The real story lies in how we compare and interpret all these valuation methods, with an even smarter perspective revealed at the end.

Find out why ResMed's 3.2% return over the last year is lagging behind its peers.

Approach 1: ResMed Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and discounting them back to today’s dollars. This process allows investors to weigh future growth against present costs. For ResMed, the DCF approach uses a 2 Stage Free Cash Flow to Equity model, focusing on current cash generation and anticipated expansion in the future.

Currently, ResMed generates $1.75 billion in Free Cash Flow. Analysts forecast steady expansion, with Free Cash Flow expected to reach $1.83 billion by 2028. While detailed analyst estimates go out five years, Simply Wall St extends these projections to a ten-year horizon, predicting Free Cash Flow of approximately $2.25 billion by 2035. This approach incorporates both expert forecasts and logical extrapolation, providing a broader picture of sustained value creation.

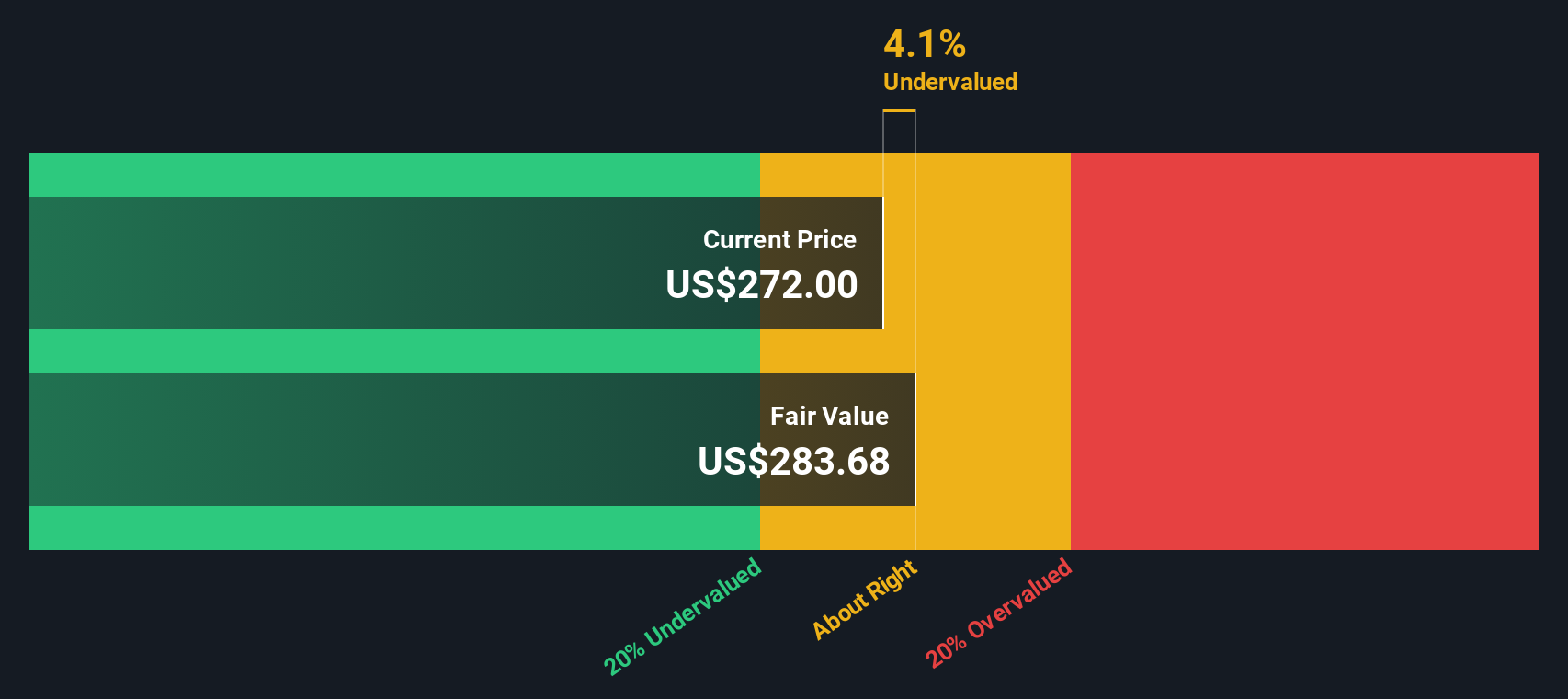

Based on this model, the intrinsic value for ResMed is estimated at $256.73 per share. This figure is just 0.7% above the current trading price, suggesting that shares are priced almost exactly in line with conservative cash flow expectations.

Result: ABOUT RIGHT

ResMed is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: ResMed Price vs Earnings

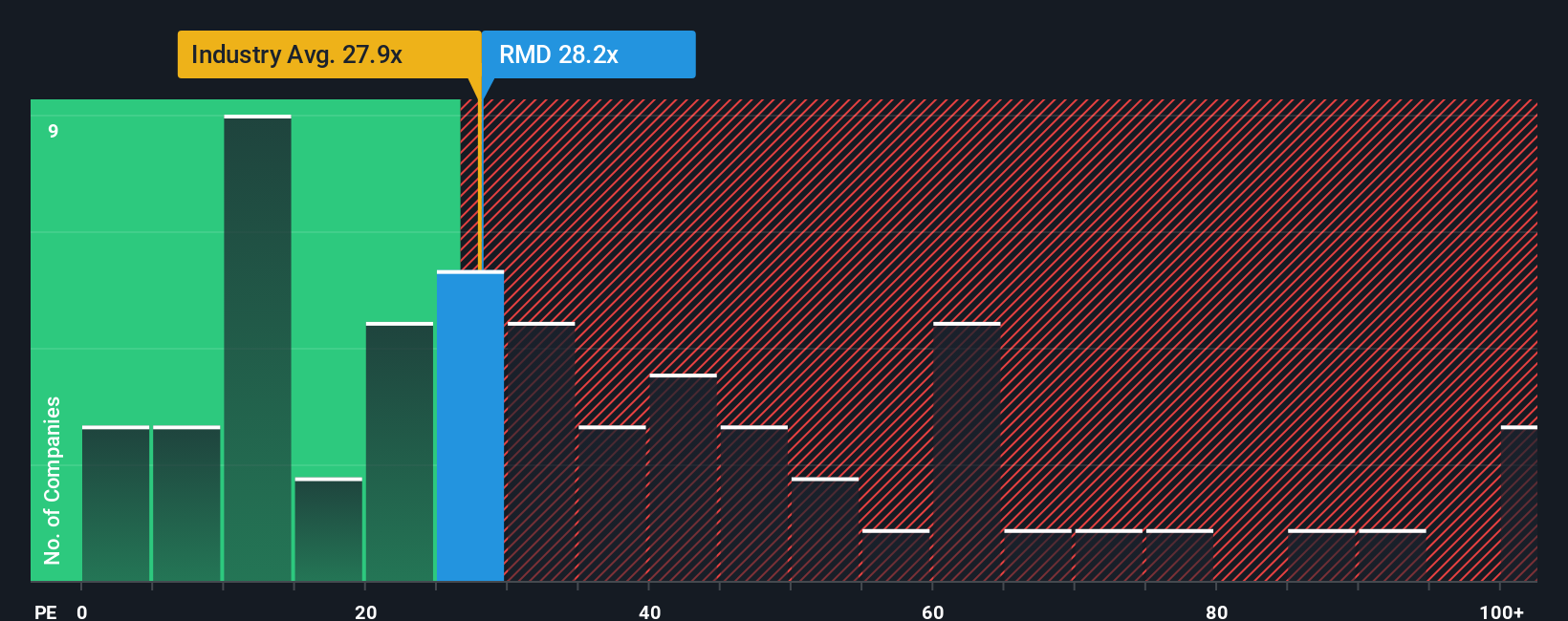

The Price-to-Earnings (PE) ratio is widely used to value profitable companies like ResMed because it quickly relates a company’s share price to its earnings per share. For investors, the PE ratio is a snapshot of how much the market is willing to pay for every dollar of current earnings. It is especially useful for companies with a stable track record of profitability.

A higher PE ratio can reflect expectations of stronger future growth or lower perceived risk. Conversely, a lower PE ratio might signal muted growth expectations or higher risk. Determining what PE ratio is “normal” depends not just on the company, but also on the industry and broader market sentiment.

ResMed's current PE ratio is 25.9x. This is notably below both the industry average of 28.9x and the peer group average of 31.5x, suggesting that ResMed is trading at a discount to its closest competitors and the broader medical equipment sector.

To offer more context, Simply Wall St calculates a “Fair Ratio” for ResMed, which is 26.7x. This proprietary metric incorporates factors such as earnings growth, risk profile, profit margin, industry standards, and market capitalization, making it more comprehensive than a simple industry or peer comparison.

Because the Fair Ratio considers the full picture including growth prospects, profitability, industry dynamics, and company size, it provides a more accurate benchmark for what ResMed’s valuation should be. This ensures the analysis reflects the total company profile and is not skewed by just one or two variables.

With ResMed’s current PE of 25.9x almost matching the Fair Ratio of 26.7x, the stock appears fairly valued on earnings.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1432 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your ResMed Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story or perspective about a company, combining what you believe about its future revenues, profit margins, and risks, with a fair value estimate grounded in real financial forecasts. It links everything together by connecting the company’s story, its numbers, and your sense of what it is really worth.

Narratives make complex valuation easy and accessible for everyone. On Simply Wall St’s Community page, used by millions of investors, you can explore different Narratives, instantly see how your beliefs influence fair value, and track how they compare to the current share price. This can help you decide whether to buy, hold, or sell.

What’s powerful about Narratives is that they automatically update whenever key news breaks or earnings reports are released, so your fair value stays relevant. For example, some investors are bullish on ResMed, expecting strategic acquisitions and margin growth could push fair value over $325 per share. Others, who are more cautious about regulatory and competitive risks, see fair value closer to $215. Narratives let you invest according to your own outlook, not just the consensus.

Do you think there's more to the story for ResMed? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:RMD

ResMed

Develops, manufactures, distributes, and markets medical devices and cloud-based software applications to diagnose, treat, and manage respiratory disorders in the United States and internationally.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

106 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

936 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

143 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative