Advertisement

- United States

- /

- Medical Equipment

- /

- NYSE:MDT

A Look at Medtronic’s (MDT) Valuation After Strong Earnings and Raised Guidance

Simply Wall St

Reviewed by Simply Wall St

Medtronic (NYSE:MDT) just posted financial results that outpaced last year in both revenue and earnings, giving investors something to talk about. The company also raised its earnings guidance for 2026 and outlined optimistic projections for 2027.

See our latest analysis for Medtronic.

Medtronic’s upbeat earnings and raised guidance haven’t gone unnoticed, with the stock climbing steadily. The 30-day share price return sits at 14.8% and year-to-date gains are now over 31%. Recent enthusiasm has also lifted its one-year total shareholder return to 25.7%, signaling that momentum is building as investors respond to Medtronic’s robust results, expansion plans, and strategic moves into high-growth medical technology segments.

If Medtronic’s growth story has you looking for what’s next in healthcare, it’s a great moment to discover See the full list for free.

The big question now is whether Medtronic’s strong run leaves more opportunity on the table for new investors, or if future growth expectations are already fully reflected in the current share price.

Most Popular Narrative: 4.1% Undervalued

With Medtronic’s last close at $105.33 and the most-followed narrative estimating a fair value at $109.82, analysts appear to see modest upside from here. This reflects growing confidence in the company’s new product launches, recovery in key segments, and the durability of its innovation-led strategy.

The company’s expanding product pipeline and robust R&D investment set the stage for more durable and sustainable performance. New product momentum was noted as especially promising.

What do analysts see that could push Medtronic higher? Analysts point to a handful of aggressive assumptions about future growth and profitability, based on expectations that could surprise both bulls and bears. Click in to see exactly what they’re betting on for the next three years.

Result: Fair Value of $109.82 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent margin pressure or slower than expected adoption of new products could challenge the optimistic outlook and alter Medtronic's growth trajectory.

Find out about the key risks to this Medtronic narrative.

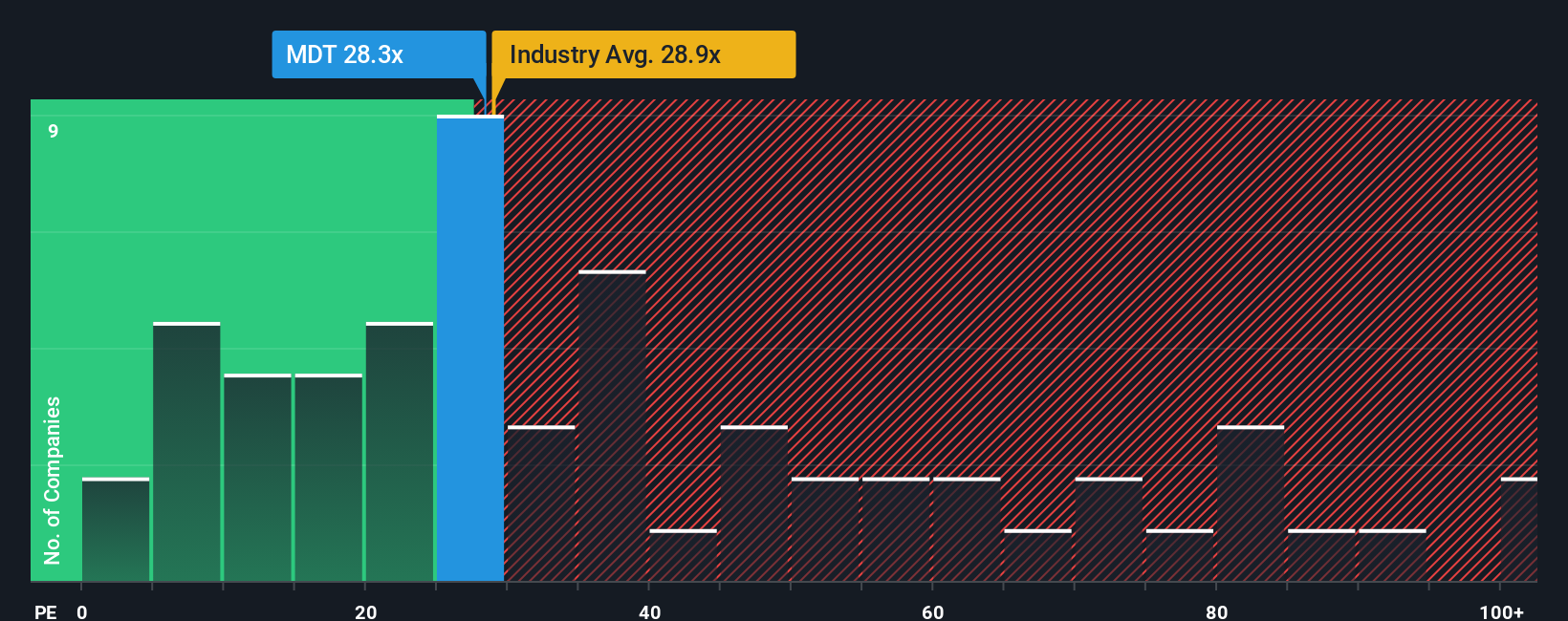

Another View: What Do Multiples Tell Us?

To challenge the fair value perspective, let’s look at how Medtronic is priced compared to industry standards. Its price-to-earnings ratio is 28.3x, which is not only below the peer average of 48.1x but also slightly below the Medical Equipment industry average of 28.9x. Our fair ratio analysis points to a level of 32x, suggesting the market could still re-rate Medtronic higher if optimism grows. Yet, with ratios this close, the risk of sudden revaluation is very real. Could a shift in sentiment trigger sharper moves up or down?

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Medtronic for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 921 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Medtronic Narrative

If you see things differently or want to dig deeper into the numbers, you can easily shape your own perspective in just a few minutes. Do it your way

A great starting point for your Medtronic research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Stay ahead of the curve by targeting opportunities that match your strategy. Don’t get left behind. These handpicked screens could spark your next winning investment.

- Maximize your income potential and spot reliable yield opportunities when you check out these 15 dividend stocks with yields > 3% with robust payouts above 3%.

- Capitalize on game-changing breakthroughs and emerging leaders by browsing these 25 AI penny stocks shaping tomorrow’s tech landscape today.

- Catch undervalued opportunities that others might overlook by scanning these 921 undervalued stocks based on cash flows chosen for their strong cash flow fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MDT

Medtronic

Develops, manufactures, and sells device-based medical therapies to healthcare systems, physicians, clinicians, and patients in the United States, Ireland, and internationally.

Established dividend payer with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative