- United States

- /

- Healthcare Services

- /

- NYSE:MCK

McKesson (NYSE:MCK) Reports US$90 Billion Sales With 66% Q4 Net Income Rise

Reviewed by Simply Wall St

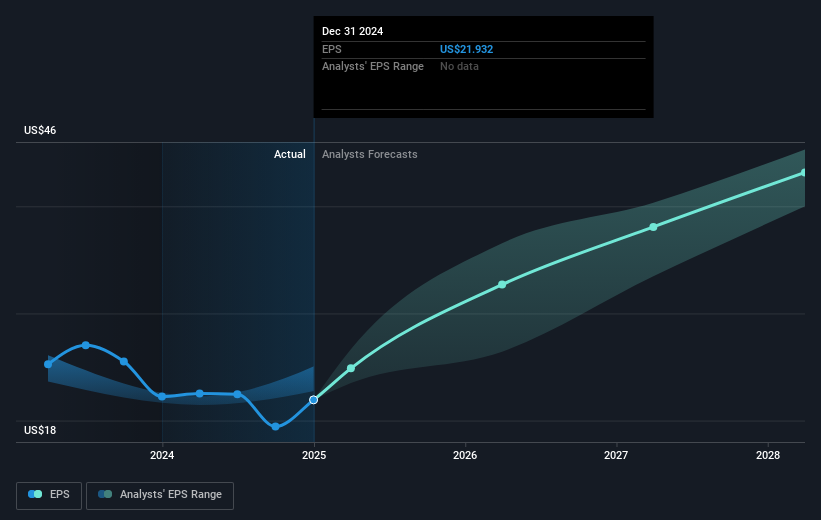

McKesson (NYSE:MCK) recently reported a significant increase in earnings for the fourth quarter and full year, reflecting robust growth in sales and net income. This performance, alongside the launch of its Precision Care Companion initiative in April, highlights the company's strategic focus on improving healthcare outcomes. Simultaneously, McKesson's declared dividend and the strong financial results likely bolstered investor confidence, aligning with a broader market trend of 1.3% growth over the past week. Despite some market fluctuations due to global trade uncertainties, McKesson's share price appreciated by 16% in the last quarter.

McKesson has 2 weaknesses (and 1 which is significant) we think you should know about.

The recent news about McKesson's earnings growth and the Precision Care Companion initiative may positively influence the company's revenue and earnings forecasts, as both initiatives align with its focus on healthcare improvement. The PRISM Vision Acquisition could further expand McKesson's specialty services, particularly in retinal and ophthalmology care, potentially boosting future earnings. Analysts' expectations of revenue growth in the specialty pharmaceutical distribution and biopharma services may see support from these strategic moves.

Over the past five years, McKesson's total shareholder return, which includes share price appreciation and dividends, reached a very large value of 451.97%, showcasing robust long-term growth. In the shorter term, McKesson's shares outperformed the US Healthcare industry over the past year, surpassing the industry that experienced an 11.2% decline. Such performance indicates resilience even amidst fluctuating market conditions.

With McKesson's current share price at US$711.07, slightly ahead of the consensus price target of US$709.65, the market appears to have already priced in much of this optimistic outlook. Investors should consider the potential for revenue growth driven by recent acquisitions and initiatives, while also being mindful of risks posed by regulatory challenges and changes in product volumes. The narrow gap between the current share price and the price target could suggest analysts view the stock as fairly valued given the anticipated earnings growth trajectory.

Understand McKesson's track record by examining our performance history report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MCK

McKesson

Provides healthcare services in the United States and internationally.

Solid track record and good value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion