Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:BKD

Is Brookdale Senior Living (NYSE:BKD) Using Debt In A Risky Way?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Brookdale Senior Living Inc. (NYSE:BKD) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Brookdale Senior Living

What Is Brookdale Senior Living's Net Debt?

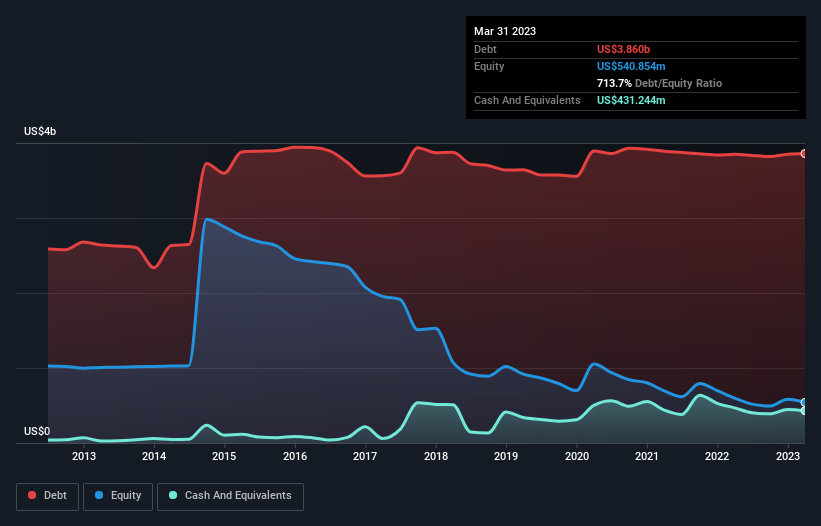

As you can see below, Brookdale Senior Living had US$3.86b of debt, at March 2023, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$431.2m, its net debt is less, at about US$3.43b.

How Healthy Is Brookdale Senior Living's Balance Sheet?

According to the last reported balance sheet, Brookdale Senior Living had liabilities of US$707.3m due within 12 months, and liabilities of US$4.64b due beyond 12 months. Offsetting these obligations, it had cash of US$431.2m as well as receivables valued at US$52.6m due within 12 months. So it has liabilities totalling US$4.86b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$643.6m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Brookdale Senior Living would likely require a major re-capitalisation if it had to pay its creditors today. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Brookdale Senior Living can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Brookdale Senior Living wasn't profitable at an EBIT level, but managed to grow its revenue by 4.0%, to US$2.8b. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, Brookdale Senior Living had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable US$85m at the EBIT level. Reflecting on this and the significant total liabilities, it's hard to know what to say about the stock because of our intense dis-affinity for it. Sure, the company might have a nice story about how they are going on to a brighter future. But the reality is that it is low on liquid assets relative to liabilities, and it burned through US$162m in the last year. So is this a high risk stock? We think so, and we'd avoid it. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 4 warning signs we've spotted with Brookdale Senior Living (including 1 which makes us a bit uncomfortable) .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Brookdale Senior Living might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:BKD

Brookdale Senior Living

Owns, manages, and operates senior living communities in the United States.

Undervalued low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor