Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:QDEL

The Bull Case For QuidelOrtho (QDEL) Could Change Following Fresh Insider Buying By Top Executives

Simply Wall St

Reviewed by Sasha Jovanovic

- In late November 2025, QuidelOrtho drew heightened attention after director Joseph D Jr. Wilkins bought 370 shares and CEO Brian J. Blaser purchased 23,500 shares, signaling leadership’s willingness to commit personal capital to the diagnostics company.

- These insider purchases have become a focal point for investors, who often treat such buying as a real-time indicator of management’s conviction in the company’s prospects.

- We’ll now examine how this insider buying wave could influence QuidelOrtho’s investment narrative built around global expansion, operational efficiency and margin recovery.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

QuidelOrtho Investment Narrative Recap

To own QuidelOrtho, you need to believe its global diagnostics footprint and operational clean-up can eventually outweigh current losses and COVID testing declines. The recent insider buying spike supports sentiment but does not materially change the immediate catalyst, which remains margin recovery, or the key risk, which is ongoing revenue pressure as legacy COVID and discontinued product lines roll off.

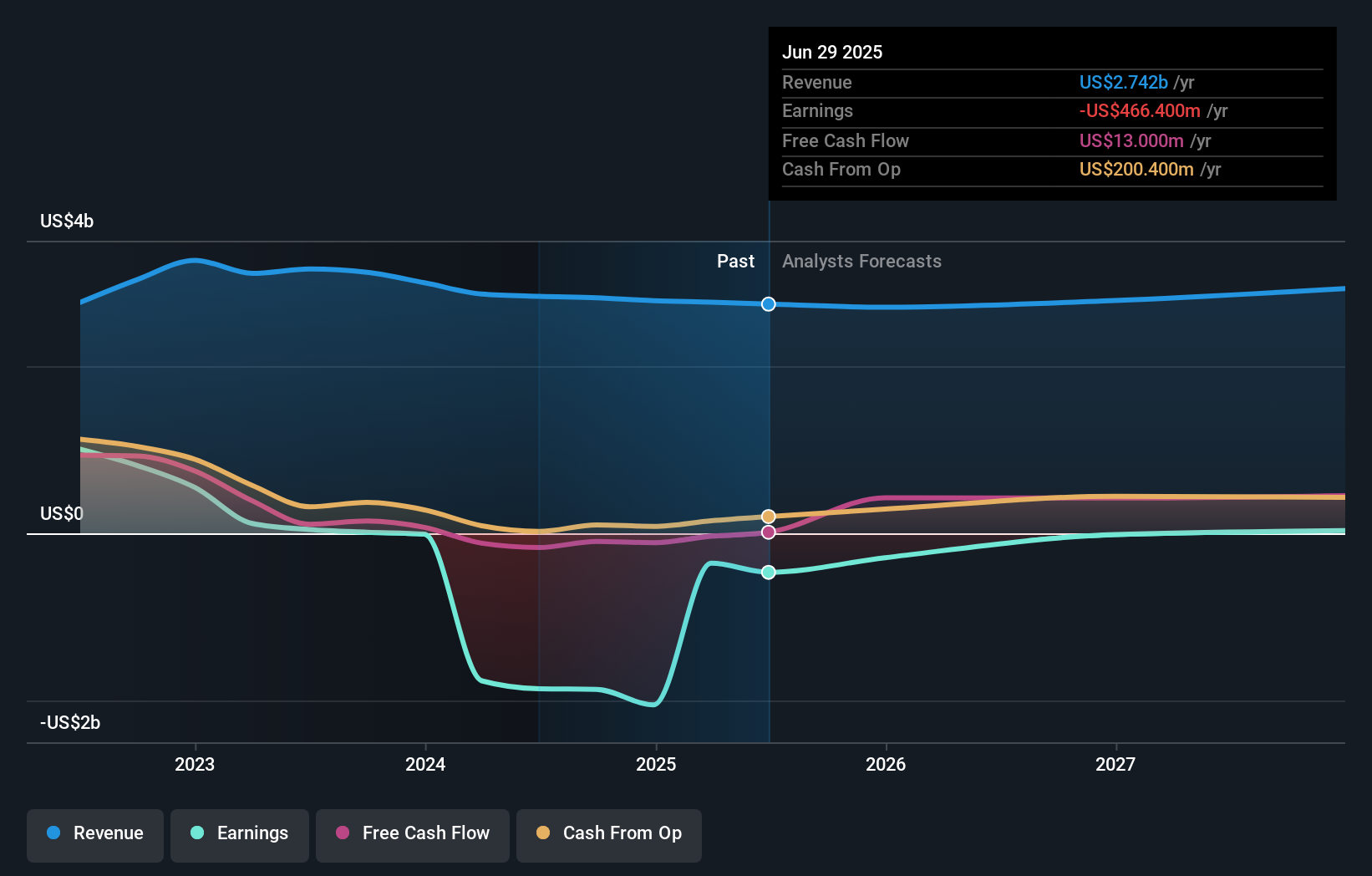

The most relevant recent announcement here is QuidelOrtho’s updated 2025 revenue guidance of US$2.68 billion to US$2.74 billion, which frames those insider purchases against a backdrop of shrinking sales and sizable net losses. For investors, that guidance keeps the focus on whether cost savings, new assays such as the FDA cleared VITROS hs Troponin I test, and international growth can offset portfolio pruning and sustain the investment narrative.

Yet while insider buying can be reassuring, investors should also be aware of the risk that ongoing product discontinuations and COVID normalization could still...

Read the full narrative on QuidelOrtho (it's free!)

QuidelOrtho's narrative projects $3.0 billion revenue and $17.2 million earnings by 2028. This requires 2.6% yearly revenue growth and an earnings increase of about $483.6 million from -$466.4 million today.

Uncover how QuidelOrtho's forecasts yield a $37.67 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates span roughly US$37.67 to US$83.22 per share, showing how far apart individual views can be. You may want to weigh that spread against the central risk that shrinking COVID revenues and discontinued product lines are pressuring both diversification and the path back to profitability.

Explore 3 other fair value estimates on QuidelOrtho - why the stock might be worth over 2x more than the current price!

Build Your Own QuidelOrtho Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your QuidelOrtho research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free QuidelOrtho research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate QuidelOrtho's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if QuidelOrtho might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:QDEL

Undervalued with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

53 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

53 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative