- United States

- /

- Medical Equipment

- /

- NasdaqGS:QDEL

Robust Earnings May Not Tell The Whole Story For QuidelOrtho (NASDAQ:QDEL)

QuidelOrtho Corporation's (NASDAQ:QDEL) robust recent earnings didn't do much to move the stock. We think this is due to investors looking beyond the statutory profits and being concerned with what they see.

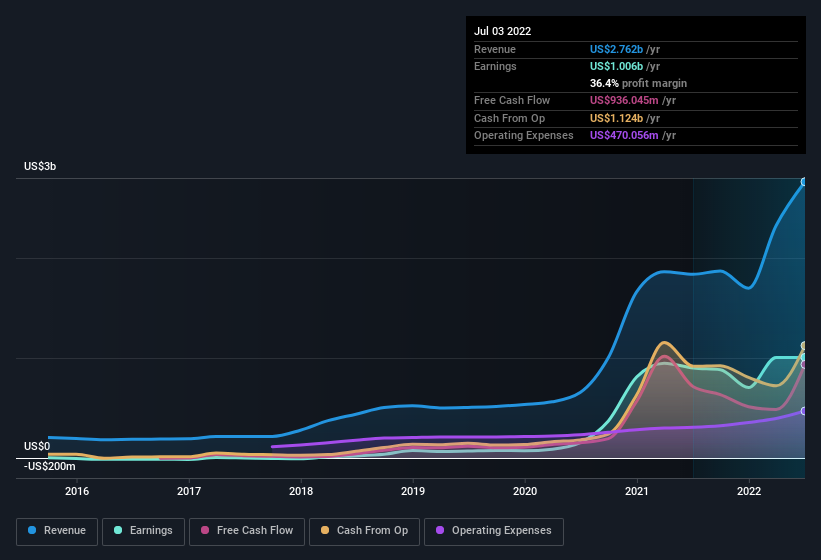

See our latest analysis for QuidelOrtho

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. In fact, QuidelOrtho increased the number of shares on issue by 61% over the last twelve months by issuing new shares. That means its earnings are split among a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out QuidelOrtho's historical EPS growth by clicking on this link.

How Is Dilution Impacting QuidelOrtho's Earnings Per Share (EPS)?

QuidelOrtho has improved its profit over the last three years, with an annualized gain of 1,345% in that time. But EPS was only up 1,181% per year, in the exact same period. And in the last year the company managed to bump profit up by 12%. But in comparison, EPS only increased by 4.6% over the same period. So you can see that the dilution has had a fairly significant impact on shareholders.

In the long term, earnings per share growth should beget share price growth. So QuidelOrtho shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On QuidelOrtho's Profit Performance

QuidelOrtho shareholders should keep in mind how many new shares it is issuing, because, dilution clearly has the power to severely impact shareholder returns. As a result, we think it may well be the case that QuidelOrtho's underlying earnings power is lower than its statutory profit. But the good news is that its EPS growth over the last three years has been very impressive. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. To that end, you should learn about the 3 warning signs we've spotted with QuidelOrtho (including 2 which are a bit unpleasant).

This note has only looked at a single factor that sheds light on the nature of QuidelOrtho's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if QuidelOrtho might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:QDEL

Undervalued with worrying balance sheet.