Advertisement

- United States

- /

- Healthcare Services

- /

- OTCPK:OTRK.Q

Ontrak, Inc. (NASDAQ:OTRK) Just Reported And Analysts Have Been Cutting Their Estimates

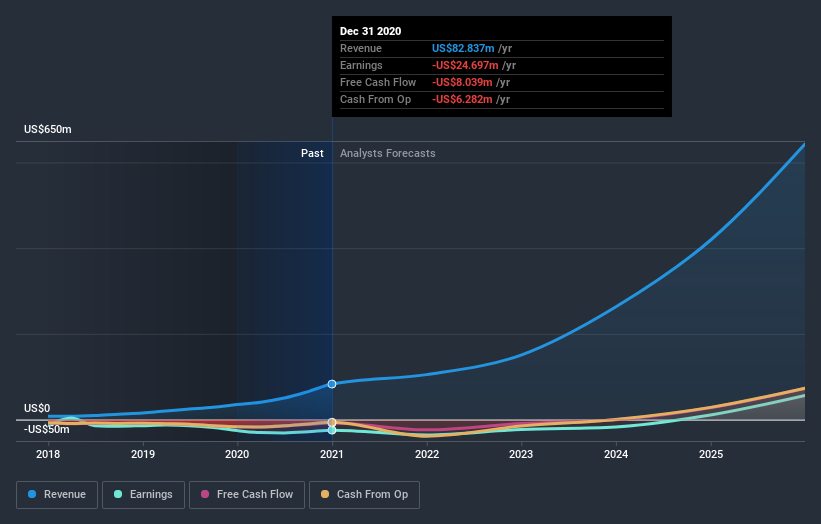

Shareholders in Ontrak, Inc. (NASDAQ:OTRK) had a terrible week, as shares crashed 61% to US$26.03 in the week since its latest full-year results. The results overall were pretty much dead in line with analyst forecasts; revenues were US$83m and statutory losses were US$1.44 per share. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for Ontrak

Taking into account the latest results, the most recent consensus for Ontrak from seven analysts is for revenues of US$104.9m in 2021 which, if met, would be a substantial 27% increase on its sales over the past 12 months. Losses are forecast to balloon 26% to US$1.82 per share. Before this earnings announcement, the analysts had been modelling revenues of US$165.1m and losses of US$0.60 per share in 2021. There's been a definite change in sentiment in this update, with the analysts administering a notable cut to next year's revenue estimates, while at the same time increasing their loss per share forecasts.

The consensus price target fell 48% to US$47.86, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Ontrak at US$80.00 per share, while the most bearish prices it at US$30.00. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how analysts think this business will perform. With this in mind, we wouldn't rely too heavily the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's pretty clear that there is an expectation that Ontrak's revenue growth will slow down substantially, with revenues to the end of 2021 expected to display 27% growth on an annualised basis. This is compared to a historical growth rate of 58% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 7.1% annually. So it's pretty clear that, while Ontrak's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at Ontrak. They also downgraded their revenue estimates, although industry data suggests that Ontrak's revenues are expected to grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Ontrak's future valuation.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for Ontrak going out to 2025, and you can see them free on our platform here.

You still need to take note of risks, for example - Ontrak has 3 warning signs we think you should be aware of.

If you’re looking to trade Ontrak, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OTCPK:OTRK.Q

Ontrak

Operates as a value-based behavioral healthcare company in the United States.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor