Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:OMCL

Omnicell (NASDAQ:OMCL) Seems To Use Debt Rather Sparingly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Omnicell, Inc. (NASDAQ:OMCL) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Omnicell Carry?

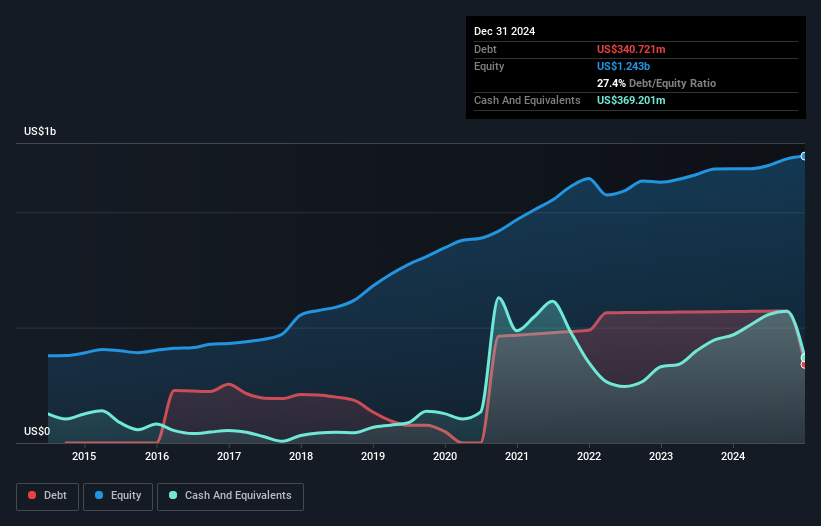

You can click the graphic below for the historical numbers, but it shows that Omnicell had US$340.7m of debt in December 2024, down from US$569.7m, one year before. However, its balance sheet shows it holds US$369.2m in cash, so it actually has US$28.5m net cash.

How Strong Is Omnicell's Balance Sheet?

We can see from the most recent balance sheet that Omnicell had liabilities of US$595.7m falling due within a year, and liabilities of US$282.0m due beyond that. On the other hand, it had cash of US$369.2m and US$268.9m worth of receivables due within a year. So its liabilities total US$239.6m more than the combination of its cash and short-term receivables.

Of course, Omnicell has a market capitalization of US$1.53b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, Omnicell boasts net cash, so it's fair to say it does not have a heavy debt load!

View our latest analysis for Omnicell

It was also good to see that despite losing money on the EBIT line last year, Omnicell turned things around in the last 12 months, delivering and EBIT of US$5.5m. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Omnicell can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Omnicell has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Omnicell actually produced more free cash flow than EBIT over the last year. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing Up

Although Omnicell's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$28.5m. The cherry on top was that in converted 2,458% of that EBIT to free cash flow, bringing in US$135m. So is Omnicell's debt a risk? It doesn't seem so to us. Another factor that would give us confidence in Omnicell would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:OMCL

Omnicell

Provides medication management solutions and adherence tools for healthcare systems and pharmacies the United States and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor