Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:NVCR

NovoCure Limited (NASDAQ:NVCR) Looks Just Right With A 84% Price Jump

The NovoCure Limited (NASDAQ:NVCR) share price has done very well over the last month, posting an excellent gain of 84%. The annual gain comes to 130% following the latest surge, making investors sit up and take notice.

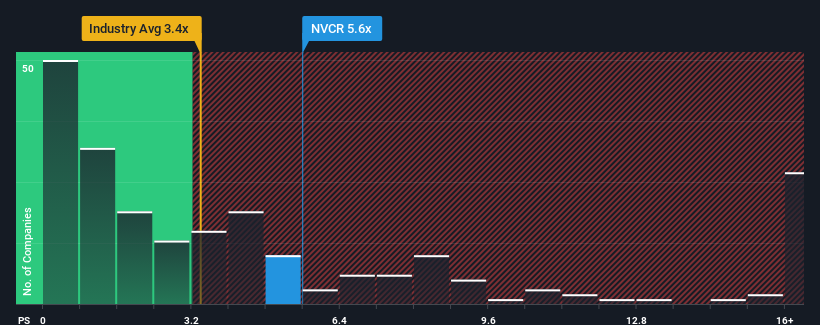

After such a large jump in price, NovoCure's price-to-sales (or "P/S") ratio of 5.6x might make it look like a strong sell right now compared to other companies in the Medical Equipment industry in the United States, where around half of the companies have P/S ratios below 3.4x and even P/S below 1.3x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for NovoCure

What Does NovoCure's P/S Mean For Shareholders?

With revenue growth that's superior to most other companies of late, NovoCure has been doing relatively well. The P/S is probably high because investors think this strong revenue performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on NovoCure.How Is NovoCure's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like NovoCure's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 15%. The latest three year period has also seen a 5.9% overall rise in revenue, aided somewhat by its short-term performance. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Turning to the outlook, the next three years should generate growth of 11% each year as estimated by the eight analysts watching the company. That's shaping up to be materially higher than the 9.2% per year growth forecast for the broader industry.

In light of this, it's understandable that NovoCure's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

NovoCure's P/S has grown nicely over the last month thanks to a handy boost in the share price. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our look into NovoCure shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

It is also worth noting that we have found 2 warning signs for NovoCure (1 doesn't sit too well with us!) that you need to take into consideration.

If you're unsure about the strength of NovoCure's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if NovoCure might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:NVCR

NovoCure

An oncology company, engages in the development, manufacture, and commercialization of tumor treating fields (TTFields) devices for the treatment of solid tumor cancers in the United States, Germany, France, Japan, Greater China, and internationally.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor