- United States

- /

- Healthtech

- /

- OTCPK:MDRX

These 4 Measures Indicate That Allscripts Healthcare Solutions (NASDAQ:MDRX) Is Using Debt Extensively

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Allscripts Healthcare Solutions, Inc. (NASDAQ:MDRX) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Allscripts Healthcare Solutions

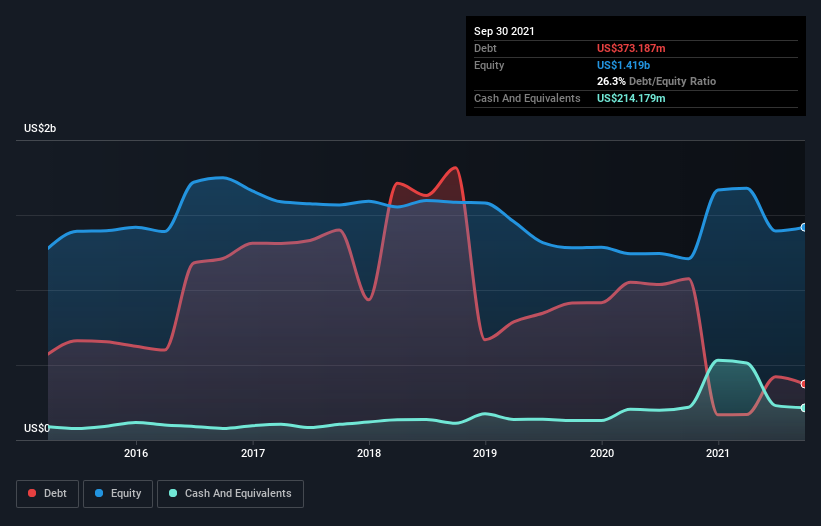

What Is Allscripts Healthcare Solutions's Net Debt?

You can click the graphic below for the historical numbers, but it shows that Allscripts Healthcare Solutions had US$373.2m of debt in September 2021, down from US$1.07b, one year before. However, it also had US$214.2m in cash, and so its net debt is US$159.0m.

How Strong Is Allscripts Healthcare Solutions' Balance Sheet?

We can see from the most recent balance sheet that Allscripts Healthcare Solutions had liabilities of US$566.9m falling due within a year, and liabilities of US$498.8m due beyond that. On the other hand, it had cash of US$214.2m and US$464.2m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$387.4m.

Since publicly traded Allscripts Healthcare Solutions shares are worth a total of US$2.27b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Allscripts Healthcare Solutions's net debt is sitting at a very reasonable 1.6 times its EBITDA, while its EBIT covered its interest expense just 5.6 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. Notably, Allscripts Healthcare Solutions made a loss at the EBIT level, last year, but improved that to positive EBIT of US$54m in the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Allscripts Healthcare Solutions's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. During the last year, Allscripts Healthcare Solutions burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Allscripts Healthcare Solutions's conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. But on the bright side, its ability to handle its debt, based on its EBITDA, isn't too shabby at all. It's also worth noting that Allscripts Healthcare Solutions is in the Healthcare Services industry, which is often considered to be quite defensive. Looking at all the angles mentioned above, it does seem to us that Allscripts Healthcare Solutions is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Allscripts Healthcare Solutions is showing 2 warning signs in our investment analysis , you should know about...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you're looking to trade Veradigm, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:MDRX

Veradigm

A healthcare technology company, provides information technology solutions to healthcare providers, payers, and biopharma markets in the United States and internationally.

Very low with weak fundamentals.

Similar Companies

Market Insights

Community Narratives