- United States

- /

- Healthcare Services

- /

- NasdaqGS:GH

With Guardant Health, Inc. (NASDAQ:GH) It Looks Like You'll Get What You Pay For

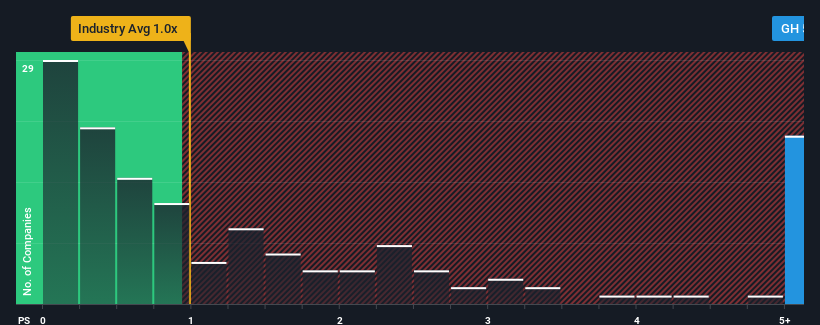

Guardant Health, Inc.'s (NASDAQ:GH) price-to-sales (or "P/S") ratio of 5.3x may look like a poor investment opportunity when you consider close to half the companies in the Healthcare industry in the United States have P/S ratios below 1x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Guardant Health

What Does Guardant Health's Recent Performance Look Like?

Recent times have been advantageous for Guardant Health as its revenues have been rising faster than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on Guardant Health will help you uncover what's on the horizon.Do Revenue Forecasts Match The High P/S Ratio?

Guardant Health's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Retrospectively, the last year delivered an exceptional 24% gain to the company's top line. Pleasingly, revenue has also lifted 97% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 20% per year as estimated by the analysts watching the company. With the industry only predicted to deliver 7.2% each year, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Guardant Health's P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Guardant Health maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Healthcare industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Before you take the next step, you should know about the 2 warning signs for Guardant Health that we have uncovered.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:GH

Guardant Health

A precision oncology company, provides blood and tissue tests, data sets, and analytics in the United States and internationally.

Low and slightly overvalued.