Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqCM:CODX

Things Look Grim For Co-Diagnostics, Inc. (NASDAQ:CODX) After Today's Downgrade

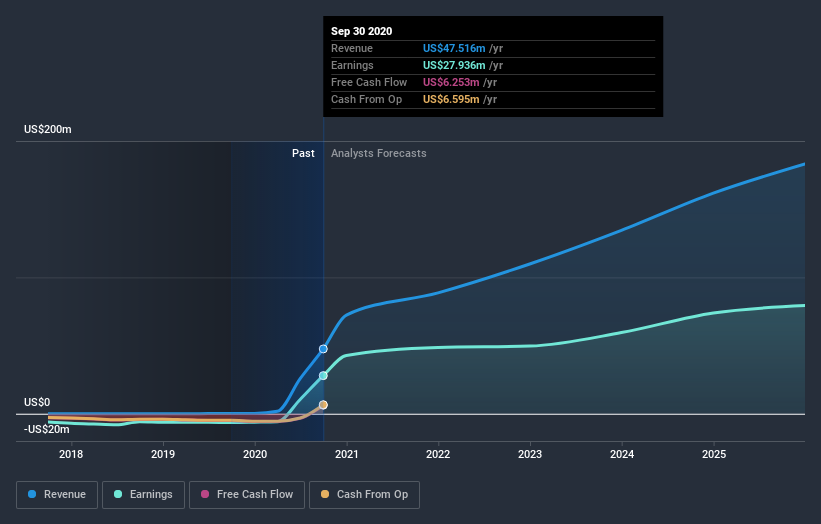

Market forces rained on the parade of Co-Diagnostics, Inc. (NASDAQ:CODX) shareholders today, when the analysts downgraded their forecasts for next year. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analysts have soured majorly on the business. Investors however, have been notably more optimistic about Co-Diagnostics recently, with the stock price up a notable 13% to US$13.94 in the past week. Whether the downgrade will have a negative impact on demand for shares is yet to be seen.

After the downgrade, the three analysts covering Co-Diagnostics are now predicting revenues of US$89m in 2021. If met, this would reflect a sizeable 87% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to surge 40% to US$1.65. Previously, the analysts had been modelling revenues of US$104m and earnings per share (EPS) of US$1.94 in 2021. It looks like analyst sentiment has declined substantially, with a measurable cut to revenue estimates and a real cut to earnings per share numbers as well.

View our latest analysis for Co-Diagnostics

It'll come as no surprise then, to learn that the analysts have cut their price target 13% to US$27.00. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Co-Diagnostics analyst has a price target of US$31.00 per share, while the most pessimistic values it at US$20.00. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Co-Diagnostics shareholders.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Co-Diagnostics' revenue growth will slow down substantially, with revenues to the end of 2021 expected to display 65% growth on an annualised basis. This is compared to a historical growth rate of 107% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 9.0% annually. So it's pretty clear that, while Co-Diagnostics' revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Unfortunately, analysts also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

After a downgrade like this, it's pretty clear that previous forecasts were too optimistic. What's more, we've spotted several possible issues with Co-Diagnostics' business, like concerns around earnings quality. For more information, you can click here to discover this and the 3 other flags we've identified.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade Co-Diagnostics, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:CODX

Co-Diagnostics

Operates as a molecular diagnostics company that develops, manufactures, and sells reagents used for diagnostic tests that function through the detection and/or analysis of nucleic acid molecules in the United States and internationally.

Flawless balance sheet with moderate risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.1% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.6% undervalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

27 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

IN

inimosini on Lucky Cement ·

Discounted Cash Flow Valuation of Lucky Cement Limited (LUCK)

Fair Value:PK₨511.86.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PR

Premium_Bobcat_cwey on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6530.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Space Exploration Technologies ·

WHY YOU SHOULD NOT BUY THE SPACEX IPO

Fair Value:US$50224.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative