Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that BIOLASE, Inc. (NASDAQ:BIOL) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for BIOLASE

How Much Debt Does BIOLASE Carry?

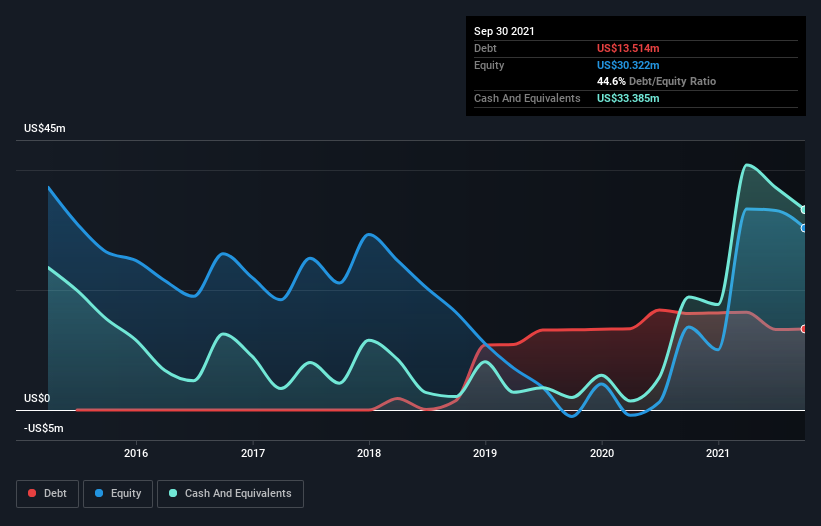

As you can see below, BIOLASE had US$13.5m of debt at September 2021, down from US$16.1m a year prior. However, its balance sheet shows it holds US$33.4m in cash, so it actually has US$19.9m net cash.

How Strong Is BIOLASE's Balance Sheet?

The latest balance sheet data shows that BIOLASE had liabilities of US$13.5m due within a year, and liabilities of US$14.7m falling due after that. Offsetting these obligations, it had cash of US$33.4m as well as receivables valued at US$3.64m due within 12 months. So it can boast US$8.83m more liquid assets than total liabilities.

This surplus suggests that BIOLASE is using debt in a way that is appears to be both safe and conservative. Due to its strong net asset position, it is not likely to face issues with its lenders. Simply put, the fact that BIOLASE has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine BIOLASE's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, BIOLASE reported revenue of US$35m, which is a gain of 44%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is BIOLASE?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months BIOLASE lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$15m and booked a US$18m accounting loss. Given it only has net cash of US$19.9m, the company may need to raise more capital if it doesn't reach break-even soon. With very solid revenue growth in the last year, BIOLASE may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 4 warning signs for BIOLASE you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if BIOLASE might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:BIOL.Q

BIOLASE

Develops, manufactures, markets, and sells laser systems for dental practitioners and their patients in the United States and internationally.

Medium-low and slightly overvalued.

Similar Companies

Market Insights

Community Narratives