- United States

- /

- Medical Equipment

- /

- NasdaqGM:APEN

If You Had Bought Apollo Endosurgery's (NASDAQ:APEN) Shares Three Years Ago You Would Be Down 36%

It is doubtless a positive to see that the Apollo Endosurgery, Inc. (NASDAQ:APEN) share price has gained some 155% in the last three months. But that doesn't change the fact that the returns over the last three years have been less than pleasing. Truth be told the share price declined 36% in three years and that return, Dear Reader, falls short of what you could have got from passive investing with an index fund.

View our latest analysis for Apollo Endosurgery

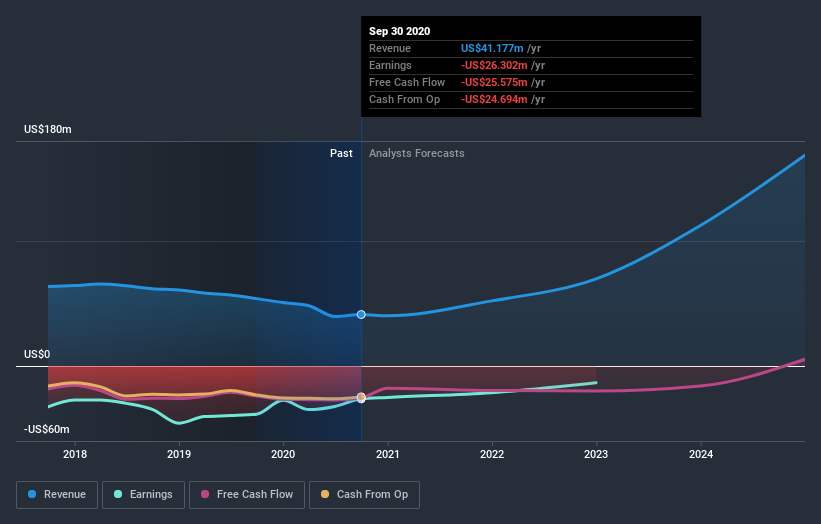

Apollo Endosurgery isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In the last three years Apollo Endosurgery saw its revenue shrink by 15% per year. That means its revenue trend is very weak compared to other loss making companies. On the face of it we'd posit the share price fall of 11% compound, over three years is well justified by the fundamental deterioration. It would probably be worth asking whether the company can fund itself to profitability. Of course, it is possible for businesses to bounce back from a revenue drop - but we'd want to see that before getting interested.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

Take a more thorough look at Apollo Endosurgery's financial health with this free report on its balance sheet.

A Different Perspective

Pleasingly, Apollo Endosurgery's total shareholder return last year was 26%. This recent result is much better than the 11% drop suffered by shareholders each year (on average) over the last three. We're generally cautious about putting too much weigh on shorter term data, but the recent improvement is definitely a positive. It's always interesting to track share price performance over the longer term. But to understand Apollo Endosurgery better, we need to consider many other factors. Case in point: We've spotted 4 warning signs for Apollo Endosurgery you should be aware of.

But note: Apollo Endosurgery may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

If you’re looking to trade Apollo Endosurgery, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGM:APEN

Apollo Endosurgery

Apollo Endosurgery, Inc., a medical technology company, focuses on the design, development, and commercialization of medical devices for gastrointestinal therapeutic endoscopy.

Excellent balance sheet with limited growth.

Similar Companies

Market Insights

Community Narratives