Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:ALGN

These 4 Measures Indicate That Align Technology (NASDAQ:ALGN) Is Using Debt Safely

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Align Technology, Inc. (NASDAQ:ALGN) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Align Technology

How Much Debt Does Align Technology Carry?

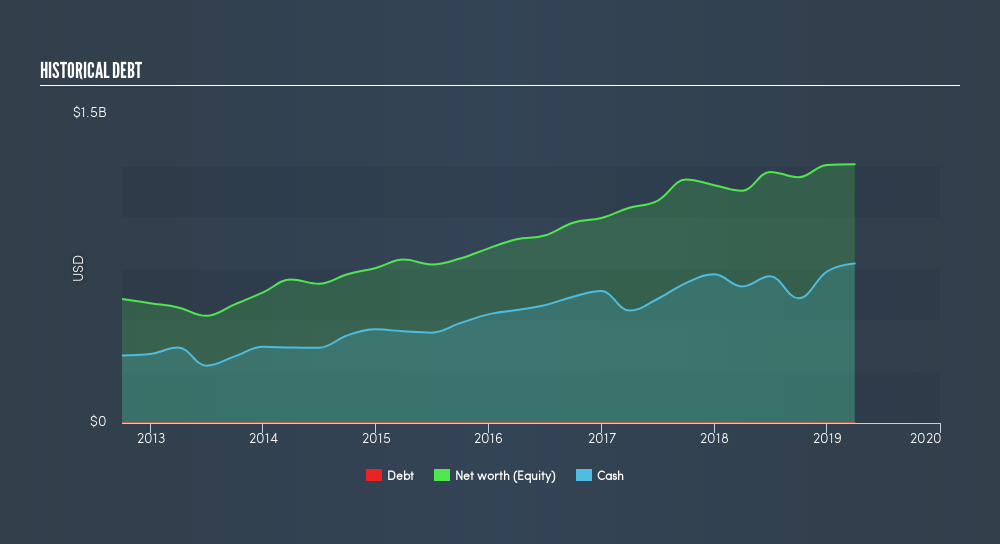

The image below, which you can click on for greater detail, shows that at March 2019 Align Technology had debt of US$56.1m, up from none in one year. But it also has US$774.5m in cash to offset that, meaning it has US$718.4m net cash.

How Strong Is Align Technology's Balance Sheet?

According to the last reported balance sheet, Align Technology had liabilities of US$804.9m due within 12 months, and liabilities of US$173.8m due beyond 12 months. On the other hand, it had cash of US$774.5m and US$479.3m worth of receivables due within a year. So it actually has US$275.1m more liquid assets than total liabilities.

This state of affairs indicates that Align Technology's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the US$21.7b company is short on cash, but still worth keeping an eye on the balance sheet. Align Technology boasts net cash, so it's fair to say it does not have a heavy debt load!

Another good sign is that Align Technology has been able to increase its EBIT by 25% in twelve months, making it easier to pay down debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Align Technology can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Align Technology may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, Align Technology recorded free cash flow worth 73% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Align Technology has net cash of US$718m, as well as more liquid assets than liabilities. And it impressed us with its EBIT growth of 25% over the last year. So we don't think Align Technology's use of debt is risky. Another factor that would give us confidence in Align Technology would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:ALGN

Align Technology

Designs, manufactures, and markets Invisalign clear aligners, Vivera retainers, and iTero intraoral scanners and services in the United States, Switzerland, and internationally.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor