Advertisement

- United States

- /

- Tobacco

- /

- NYSE:PM

Philip Morris International's (PM) Debt Redemption: A Clue to Its Evolving Capital Allocation Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 17, 2025, Philip Morris International announced it will redeem all of its outstanding 4.875% notes due February 13, 2026, with an aggregate principal amount of US$1.7 billion, scheduled for redemption on December 4, 2025.

- This development highlights PMI's active approach to managing its debt obligations and optimizing its capital structure through early redemption of outstanding notes.

- We'll explore how the company's move to redeem debt early may influence its investment outlook and risk profile for investors.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

Philip Morris International Investment Narrative Recap

To be a shareholder in Philip Morris International (PMI), you need to believe in the company's ability to successfully transition from traditional cigarettes to smoke-free products like IQOS and ZYN, capturing the shift in consumer preferences and benefiting from evolving regulatory trends. The recent early redemption of US$1.7 billion in notes highlights prudent debt management but is not likely to materially impact the key short-term catalyst of smoke-free product growth or alter the biggest risk, which remains regulatory headwinds and declining cigarette volumes.

Among recent announcements, PMI's increases to its quarterly dividend, most recently to US$1.47 per share, stand out for investors focused on income. While capital structure improvements such as debt redemption can support future dividend sustainability, the primary catalyst of market adoption for smoke-free alternatives still overshadows the current importance of these financial moves.

In contrast, investors should be aware that, while financial discipline is a positive, new regulations or taxes on both traditional and smoke-free products could ...

Read the full narrative on Philip Morris International (it's free!)

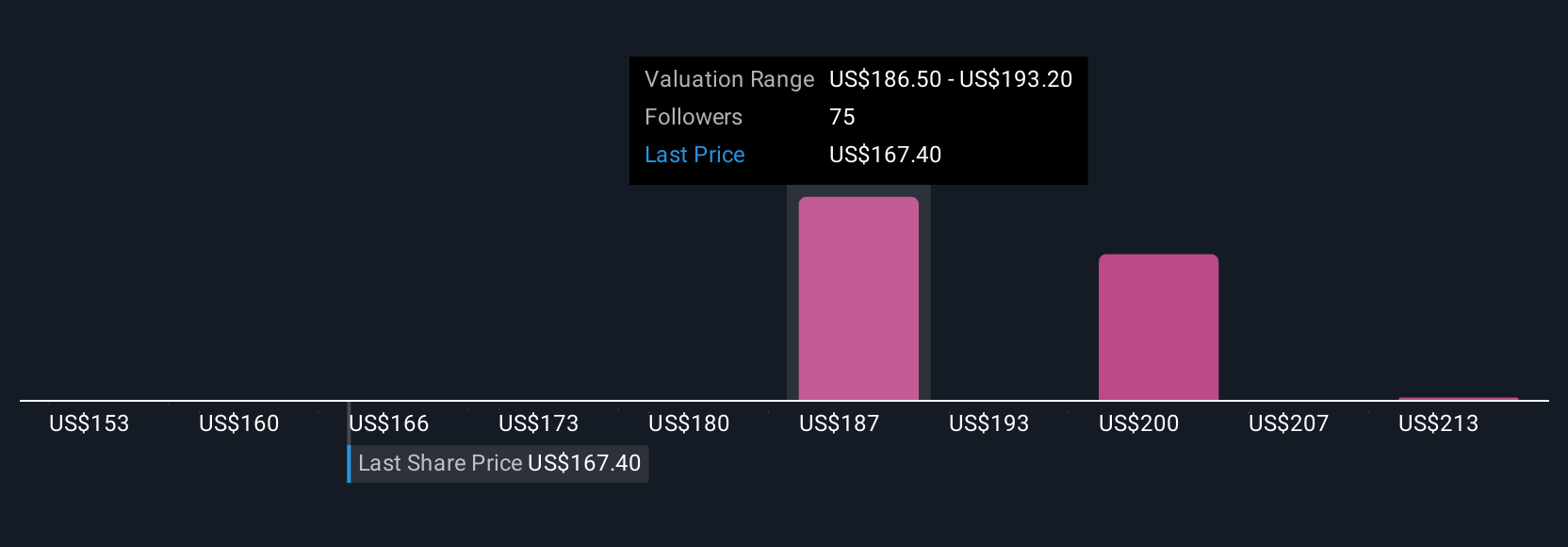

Philip Morris International's narrative projects $49.4 billion revenue and $14.5 billion earnings by 2028. This requires 8.2% yearly revenue growth and a $6.3 billion earnings increase from $8.2 billion today.

Uncover how Philip Morris International's forecasts yield a $183.25 fair value, a 17% upside to its current price.

Exploring Other Perspectives

If you focus on the most pessimistic analyst forecasts, there is much more skepticism, with expectations for US$47.1 billion in revenue and US$14.4 billion in earnings by 2028. These analysts see escalating regulation and costs as a real threat and remind you that opinions about PMI’s future can differ widely. You can review a range of perspectives to see how upcoming events like the debt redemption could adjust these outlooks.

Explore 11 other fair value estimates on Philip Morris International - why the stock might be worth as much as 41% more than the current price!

Build Your Own Philip Morris International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Philip Morris International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our top stock finds are flying under the radar-for now. Get in early:

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PM

Second-rate dividend payer and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative