- United States

- /

- Tobacco

- /

- NYSE:PM

Philip Morris International (NYSE:PM) Reports Rise in Q1 2025 Earnings and Revenue

Reviewed by Simply Wall St

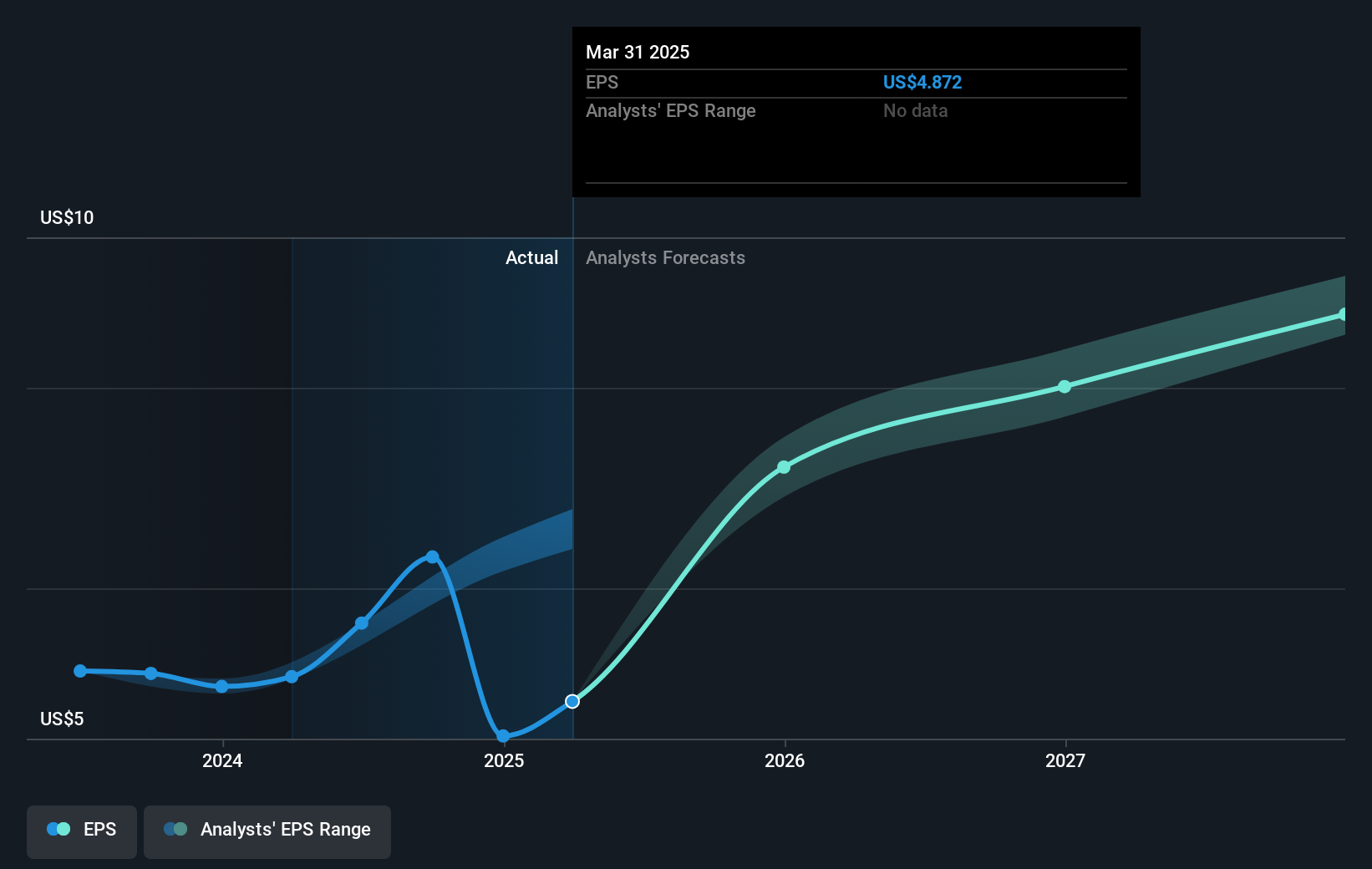

On April 23, 2025, Philip Morris International (NYSE:PM) announced its Q1 2025 earnings, reporting a notable rise in sales and net income, with diluted earnings per share up to $1.72 from $1.38 in Q1 2024. Over the last quarter, the company's shares appreciated by 34%, a substantial move as investors processed earnings and broader market trends where the Dow added 1%. Other developments included dividend affirmations and guidance confirmation. The price rally aligned with a broader market upswing, suggesting these factors added weight to the positive market momentum observed recently.

Be aware that Philip Morris International is showing 3 risks in our investment analysis.

The recent earnings announcement from Philip Morris International, with Q1 2025 diluted earnings per share rising to US$1.72, has positively influenced the company's narrative by underscoring the growth and resilience in its sales strategy. While short-term share price movements have shown a substantial increase due to this news, longer-term returns over a five-year period reveal a total return of 185.53%, emphasizing robust growth despite potential market constraints. Over the past year, Philip Morris International outperformed both the US Tobacco industry, which returned 9.1%, and the general US market, which returned 5.9%, indicating strong relative performance. This contrasts with the one-year trend, where the company's earnings decreased by 4.7%.

The enhanced earnings results have a potential influence on revenue and earnings forecasts, as seen in the analyst consensus. Projected revenues and earnings are critical, especially given possible hurdles in smoke-free product offerings. The current share price of US$168.11 represents a divergence from the consensus analyst price target of US$156.49, reflecting a modest overvaluation in the light of earnings forecasts. Although bullish analysts suggest higher price targets, this short-term price appreciation has moved the stock closer to the bearish cohort's lower expectations. This creates a scenario where investors may need to reassess the sustainability of current valuations, particularly considering ongoing challenges in product availability and regulatory uncertainties.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PM

Average dividend payer and slightly overvalued.

Similar Companies

Market Insights

Community Narratives