Lamb Weston Holdings (LW) has seen its stock price move quietly over the past month, dipping around 10%. With annual revenue and net income both growing, investors may be considering where value could emerge next.

While Lamb Weston’s 1-day and 7-day share price returns show a bit of positive momentum, the bigger picture is more muted, with a 1-year total shareholder return of -20.3%. After a challenging stretch, sentiment suggests investors are still weighing recent risks against the company’s underlying growth drivers.

With shares trading below analyst targets and recent performance lagging, investors face an important question. Is Lamb Weston now trading at a discount that opens the door to gains, or does the current price reflect all expected growth?

Advertisement

Most Popular Narrative: 9.7% Undervalued

Compared to the last close at $59.61, the most popular narrative sets Lamb Weston's fair value at $66. This suggests the stock trades at a notable discount, inviting close attention to the story driving that valuation.

Lamb Weston's $250 million cost savings program, which includes operational streamlining, zero-based budgeting, and supply chain efficiency, aims to lower the cost base significantly by fiscal 2028. This could directly enhance net margins and overall profitability. Industry rationalization, as shown by the postponement or cancellation of competing international capacity projects, is likely to foster a more favorable supply-demand balance. This could restore more constructive pricing and improve gross profit and EBITDA margins after current pressures subside.

Want the inside story on the numbers behind this narrative's fair value? The key is major operational initiatives and future profit multiples shaped by significant assumptions. Discover which specific trends and forecasts are informing analyst confidence. Only in the full narrative.

However, ongoing price and mix headwinds, as well as slow recovery in both volume and margins, could create further challenges to the current valuation outlook.

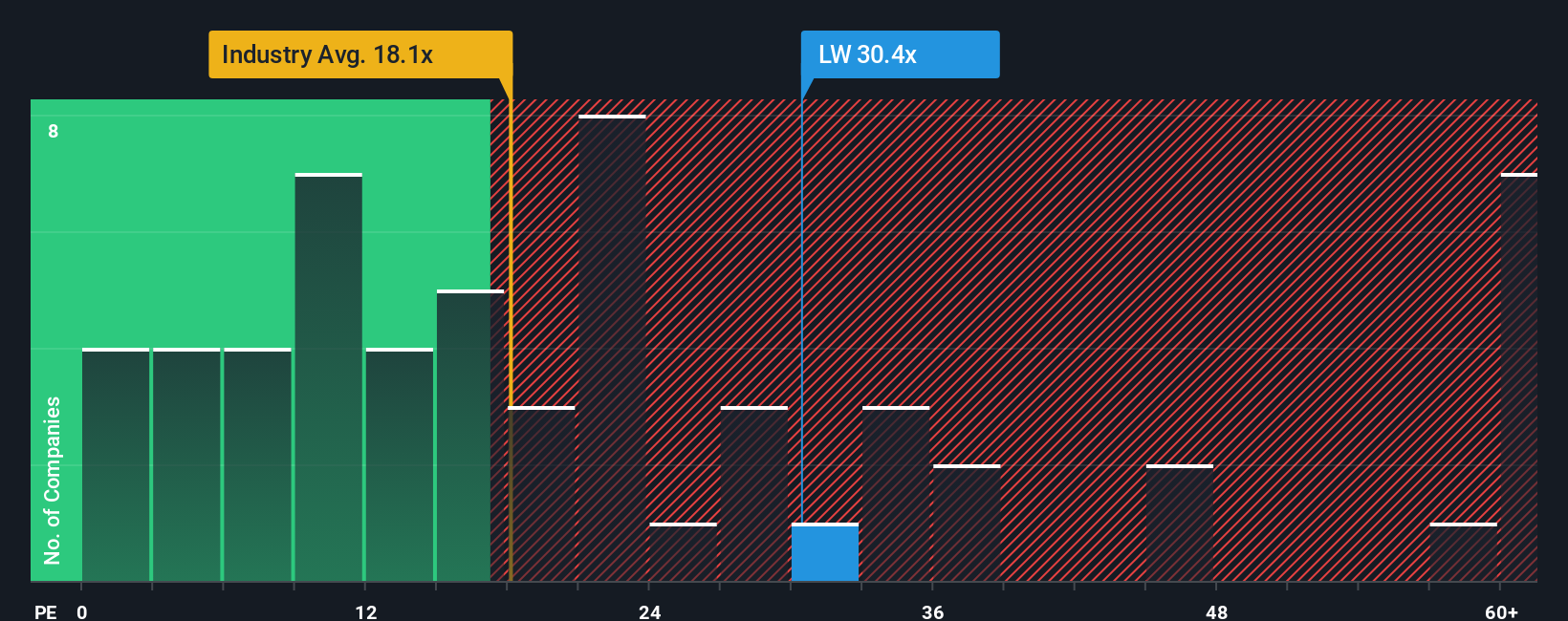

Switching perspectives, Lamb Weston’s price-to-earnings ratio stands at 28.2x. That is well above its industry peers at 12.1x and higher than a fair ratio of 23.1x. When a stock trades at a premium like this, it can raise questions about overvaluation risks or the possibility that the business may eventually align with its higher pricing.

If you see things differently or want to dig deeper into the numbers, you can craft your own perspective in just a few minutes. Do it your way.

A great starting point for your Lamb Weston Holdings research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Sharpen your strategy and supercharge your portfolio by checking out unique stocks curated for real potential. Don’t risk missing out on what could be your next big winner.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies