- United States

- /

- Food

- /

- NasdaqGS:KHC

Kraft Heinz (NASDAQ:KHC) Looks Undervalued, But Remains Under Legal Burdens

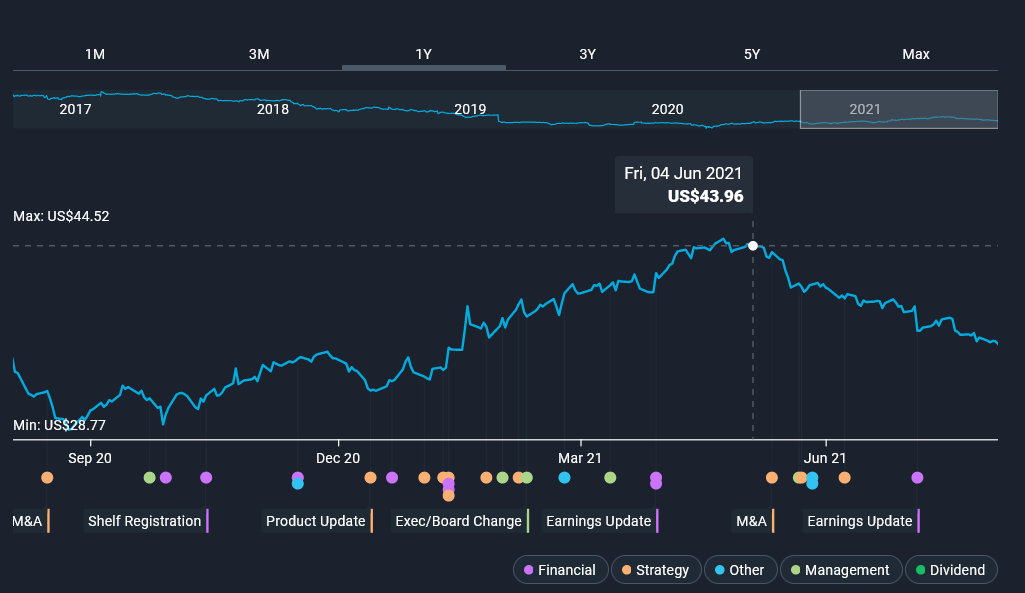

The Kraft Heinz Company (NasdaqGS: KHC) stock was doing great in 2021 until it wasn't. After shooting up over 30%, it topped in June and gave back almost all the gains for the year.

While the latest SEC slap on the wrist might be an isolated case, it certainly adds to the downtrend. We will examine the current intrinsic value based on the discounted cash-flow model in the wake of these events.

If you look at the share price, you might notice that KHC's price topped for the year almost exactly when the company announced that it completed the sale of its nuts business to Hormel Foods Corporation. The all-cash transaction was worth US$3.35b. However, this is likely a coincidence as this business accounted for less than 4% of total revenue.

Although US$15b goodwill impairment is a fact many would love to forget, the aftershocks are still present as a federal judge in Illinois denied bids to dismiss the proposed class-action lawsuit that dates back to the 2015 merger of Kraft Foods Group Inc and J.J. Heinz Co. A coalition of investors arguest that the reckless cost-cutting spree that followed the merger resulted in the eventual impairment.

As this was not enough, SEC just released a statement, charging Kraft Heinz Co. For an alleged expense management scheme.

SEC also charged former COO Eduardo Pelleissone and the former CPO Klaus Hofmann for alleged misconduct related to the scheme. Kraft agreed to cooperate and pay a civil penalty of US$62m. This comes after the company restated financial results in 2019 and saw a correction of US$208m in improperly recognized cost savings.

Check out our latest analysis for Kraft Heinz

The DCF model

Companies can be valued in many ways, so we would point out that a DCF is not perfect for every situation.If you want to learn more about discounted cash flow, the rationale behind this calculation can be read in detail in the Simply Wall St analysis model.

We use what is known as a 2-stage model, which means we have two different periods of growth rates for the company's cash flows. Generally, the first stage is higher growth, and the second stage is a lower growth phase.

To begin with, we have to get estimates of the next ten years of cash flows. Where possible, we use analyst estimates, but when these aren't available, we extrapolate the previous free cash flow (FCF) from the last estimate or reported value. We assume companies with shrinking free cash flow will slow their rate of shrinkage and that companies with growing free cash flow will see their growth rate slow over this period. We do this to reflect that growth tends to slow more in the early years than in later years.

Generally, we assume that a dollar today is more valuable than a dollar in the future, so we need to discount the sum of these future cash flows to arrive at a present value estimate:

10-year free cash flow (FCF) estimate

| 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | |

| Levered FCF ($, Millions) | US$3.42b | US$3.41b | US$3.43b | US$3.46b | US$3.51b | US$3.56b | US$3.62b | US$3.68b | US$3.75b | US$3.82b |

| Growth Rate Estimate Source | Analyst x6 | Analyst x5 | Est @ 0.51% | Est @ 0.95% | Est @ 1.26% | Est @ 1.48% | Est @ 1.63% | Est @ 1.74% | Est @ 1.82% | Est @ 1.87% |

| Present Value ($, Millions) Discounted @ 6.2% | US$3.2k | US$3.0k | US$2.9k | US$2.7k | US$2.6k | US$2.5k | US$2.4k | US$2.3k | US$2.2k | US$2.1k |

("Est" = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = US$26b

We now need to calculate the Terminal Value, which accounts for all the future cash flows after this ten-year period. The Gordon Growth formula is used to calculate Terminal Value at a future annual growth rate equal to the 5-year average of the 10-year government bond yield of 2.0%. We discount the terminal cash flows to today's value at the cost of equity of 6.2%.

Terminal Value (TV)= FCF2031 × (1 + g) ÷ (r - g) = US$3.8b× (1 + 2.0%) ÷ (6.2%-2.0%) = US$92b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= US$92b÷ ( 1 + 6.2%)10= US$50b

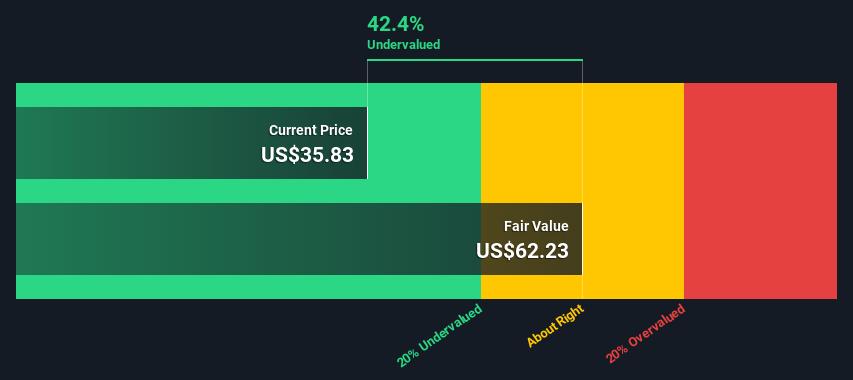

The total value is the sum of cash flows for the next ten years plus the discounted terminal value, which results in the Total Equity Value, which in this case is US$76b. The last step is to then divide the equity value by the number of shares outstanding. Relative to the current share price of US$35.8, the company appears quite good value at a 42% discount to where the stock price trades currently.

The assumptions

Now the most important inputs to a discounted cash flow are the discount rate, and of course, the actual cash flows. If you don't agree with these results, go to the calculation yourself and play with the assumptions. The DCF does not consider the possible cyclicality of an industry or a company's future capital requirements, so it does not give a full picture of its potential performance. Given that we are looking at Kraft Heinz as potential shareholders, the cost of equity is used as the discount rate rather than the cost of capital (or the weighted average cost of capital, WACC), which accounts for debt.

We've used 6.2% in this calculation, which is based on a levered beta of 0.896. Beta is a measure of a stock's volatility compared to the market as a whole. We get our beta from the industry average beta of globally comparable companies, with an imposed limit between 0.8 and 2.0, a reasonable range for a stable business.

Looking Ahead:

Whilst important, the DCF calculation ideally won't be the sole piece of analysis you scrutinize for a company. The DCF model is not a perfect stock valuation tool. Rather it should be seen as a guide to "what assumptions need to be true for this stock to be under/overvalued?" If a company grows at a different rate, or if its cost of equity or risk-free rate changes sharply, the output can look very different.

Can we work out why the company is trading at a discount to intrinsic value? Is it only legal troubles?

For Kraft Heinz, we've put together three further elements you should further research:

- Risks: We feel you should assess the 3 warning signs for Kraft Heinz (1 is significant!) we've flagged before investing in the company.

- Management: Have insiders been ramping up their shares to take advantage of the market's sentiment for KHC's future outlook? Check out our management and board analysis with insights on CEO compensation and governance factors.

- Other High-Quality Alternatives: Do you like a good all-rounder? Explore our interactive list of high quality stocks to get an idea of what else is out there you may be missing!

PS. Simply Wall St updates its DCF calculation for every American stock every day, so if you want to find the intrinsic value of any other stock, search here.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kraft Heinz might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NasdaqGS:KHC

Kraft Heinz

Manufactures and markets food and beverage products in North America and internationally.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)