Advertisement

- United States

- /

- Food

- /

- NasdaqGS:BYND

Beyond Meat (BYND): Reassessing Valuation After Sharp Share Price Slide and Recent Bounce

Simply Wall St

Reviewed by Simply Wall St

Why Beyond Meat’s Stock Slide Has Investors Rechecking the Story

Beyond Meat (BYND) keeps grinding lower, with shares recently hovering just above 1 dollar after a steep drop over the past year. This has forced investors to reassess both the brand and its balance sheet.

See our latest analysis for Beyond Meat.

The latest bump in Beyond Meat’s 7 day share price return of 24.26 percent comes against a much harsher backdrop, with the year to date share price return down 68.31 percent and the 1 year total shareholder return sliding more than 70 percent, signaling that any short term momentum still sits inside a long, grinding downtrend while investors reassess growth hopes and balance sheet risk.

If this kind of volatility has you thinking about where else growth stories might emerge, it could be a good time to explore fast growing stocks with high insider ownership for other potential opportunities.

With revenues inching lower but losses narrowing and the share price already crushed, investors face a tough question: is Beyond Meat now trading below its true potential, or is the market correctly discounting any future growth?

Most Popular Narrative Narrative: 24.2% Undervalued

With Beyond Meat last closing at 1.22 dollars against a narrative fair value of 1.61 dollars, the story leans toward recovery potential rather than liquidation risk.

Continued emphasis on manufacturing cost reduction and operational right sizing, aided by the newly appointed Interim Chief Transformation Officer, supports a path to structurally lower costs of goods sold and enhanced fixed cost absorption, directly improving gross and net margins.

Curious how flat revenues, rising margins, and a richer future earnings multiple can still point to upside from here? The full narrative unpacks those assumptions.

Result: Fair Value of $1.61 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent weak demand for plant based meat, along with pressure from debt and dilution, could quickly undermine any recovery hopes embedded in this valuation.

Find out about the key risks to this Beyond Meat narrative.

Another Lens on Valuation

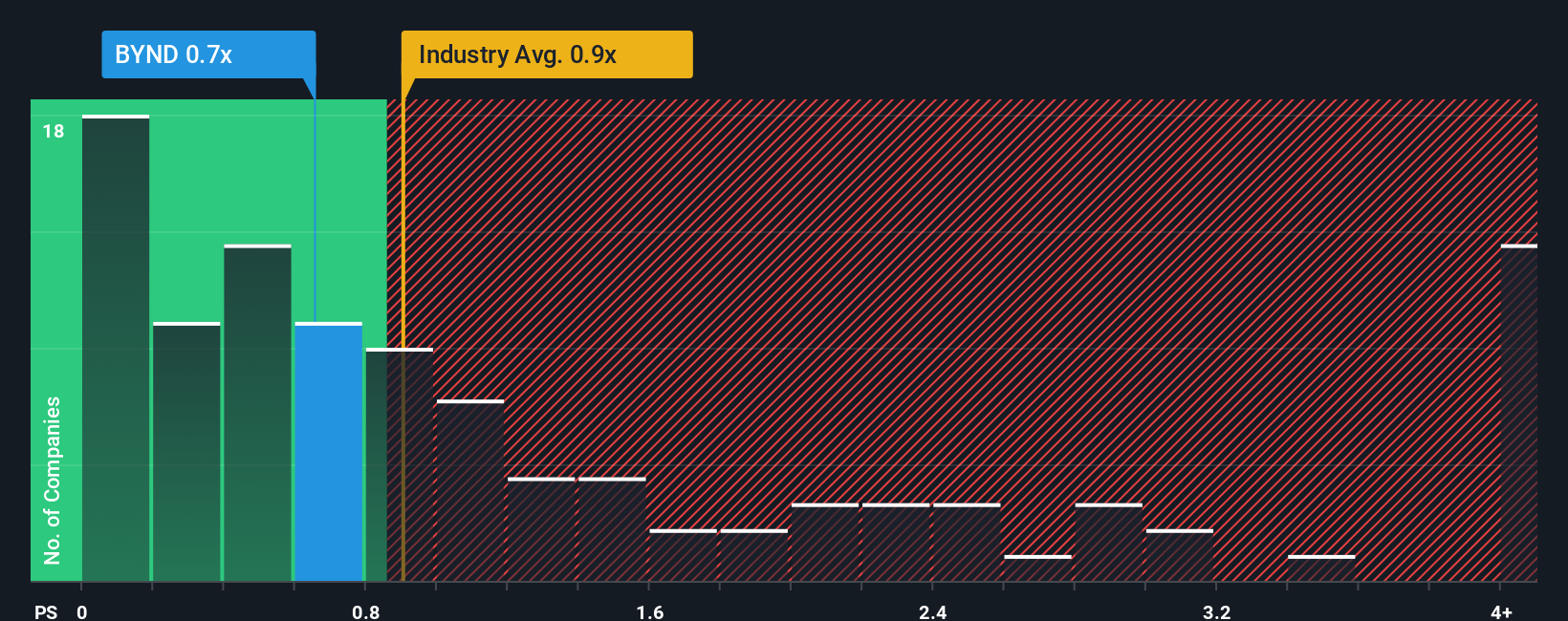

While the narrative fair value suggests upside, a simple price to sales check tells a different story. Beyond Meat trades at 1.9 times sales, versus about 0.7 times as a fair ratio and 0.7 times for both the industry and peers. This implies the market still prices in more optimism than its fundamentals justify. For investors, that gap could mean limited margin of safety if the turnaround stalls.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Beyond Meat Narrative

If you want to stress test these assumptions yourself and follow your own thesis, you can build a personalized view in minutes: Do it your way.

A great starting point for your Beyond Meat research is our analysis highlighting 4 important warning signs that could impact your investment decision.

Ready for more investment ideas?

Before you move on, explore your next potential opportunity by using the Simply Wall St Screener to uncover fresh, data driven ideas beyond a single stock.

- Target compelling potential with these 906 undervalued stocks based on cash flows that may be trading below their intrinsic worth based on future cash flows and fundamentals.

- Explore innovation trends through these 26 AI penny stocks tapping into companies involved in the development of intelligent software and automation.

- Strengthen your income strategy by scanning these 15 dividend stocks with yields > 3% offering yields that can help support returns in a range of market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Beyond Meat might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:BYND

Beyond Meat

A plant-based meat company, engages in the development, manufacture, marketing, and sale of plant-based meat products under the Beyond brand name in the United States and internationally.

Slight risk with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative