- United States

- /

- Energy Services

- /

- NYSE:TDW

Tidewater (NYSE:TDW) Stock Slides 19% Following Decline In Q4 2024 Net Income To US$37 Million

Reviewed by Simply Wall St

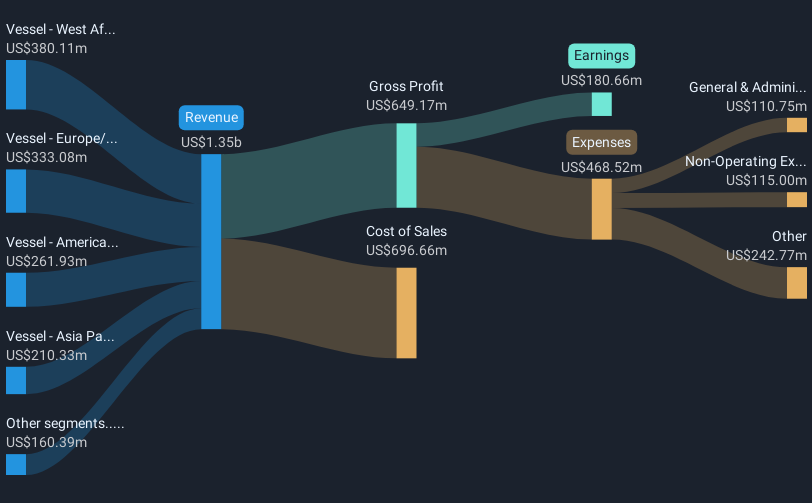

Tidewater (NYSE:TDW) faced a challenging week, with its stock price dropping 18.8%. This decline coincided with the company's recent earnings announcement, where it reported a decline in Q4 2024 net income to $36.91 million despite revenue growth. Tidewater's cautious earnings guidance for 2025, projecting revenues between $1.32 billion and $1.38 billion, may have fueled investor apprehension during the period. The strategic shift towards value-accretive acquisitions and increased share repurchases to address perceived undervaluation were addressed by the CEO, but market volatility and acquisition challenges might have impacted sentiment. Broader market conditions likely played a role as well, given the 2.5% drop in the overall market amid new U.S. tariffs and global trade uncertainties. Tidewater’s performance reflects the confluence of both company-specific factors and wider economic concerns, underscoring investor caution in the face of economic and policy developments affecting the broader market.

Click here to discover the nuances of Tidewater with our detailed analytical report.

The last five years have seen Tidewater's total shareholder return reach 336.16%. This remarkable performance was driven in part by consistent profitability growth, with earnings increasing by 65.7% annually. Tidewater's aggressive share repurchase program, as evidenced by the US$18.1 million authorization in May 2024, likely boosted shareholder value. The company's strategic focus on value-accretive acquisitions has also played a crucial role, ensuring sustained interest from investors.

Despite its long-term successes, Tidewater underperformed the US market and Energy Services industry over the past year. Nonetheless, the inclusion in the S&P 1000 and the PHLX Oil Service Sector Index in June 2024 might have contributed positively to its long-term market exposure. Finally, the appointment of Dick H. Fagerstal as the non-executive Chairman in June 2024 signaled a stable corporate governance structure, potentially enhancing investor confidence during the period.

- Get the full picture of Tidewater's valuation metrics and investment prospects—click to explore.

- Discover the key vulnerabilities in Tidewater's business with our detailed risk assessment.

- Shareholder in Tidewater? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tidewater might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TDW

Tidewater

Provides offshore support vessels and marine support services to the offshore energy industry through the operation of a fleet of offshore marine service vessels worldwide.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Community Narratives