Sable Offshore (NYSE:SOC) has faced a rough few months, with its stock sliding nearly 16% over the past 3 months and around 23% lower compared to last year. Despite this, investors are eyeing the stock's long-term growth story with curiosity, particularly in light of its strong annual revenue and net income growth.

Shares of Sable Offshore have seen their momentum fade, with a notable decline in the past quarter and a 1-year total shareholder return of -23%. While recent news flow has quieted, the story here remains one of volatility as investors reassess both risk and upside following last year's strong operational growth.

With analyst targets sitting well above the current share price, but recent financials reflecting both rapid growth and continued volatility, investors are left to decide: is Sable Offshore undervalued right now, or is the market already pricing in tomorrow's success?

Advertisement

Price-to-Book of 4.4x: Is it justified?

Sable Offshore is trading at a price-to-book (P/B) ratio of 4.4x, which stands sharply above both its peer average and the broader US oil and gas industry. At a last close of $19.56, the market values the company's assets significantly higher than the industry norm.

The price-to-book ratio measures how much investors are paying for each dollar of net assets. For oil and gas companies, which can have substantial asset bases but volatile earnings, this metric often reflects market views on future profitability and capital efficiency. A high P/B usually suggests high growth expectations or strong asset quality. However, it may also mean the market is pricing in significant potential that is not yet realized in earnings.

Compared to the industry average P/B of 1.4x and a peer average of just 0.9x, Sable Offshore's 4.4x multiple looks expensive by any measure. The spread to sector norms is wide and raises tough questions about whether the current business fundamentals and near-term growth trajectory justify this aggressive market premium.

However, until consistent profitability is achieved and sector volatility eases, Sable Offshore's elevated valuation remains highly vulnerable to changes in market sentiment.

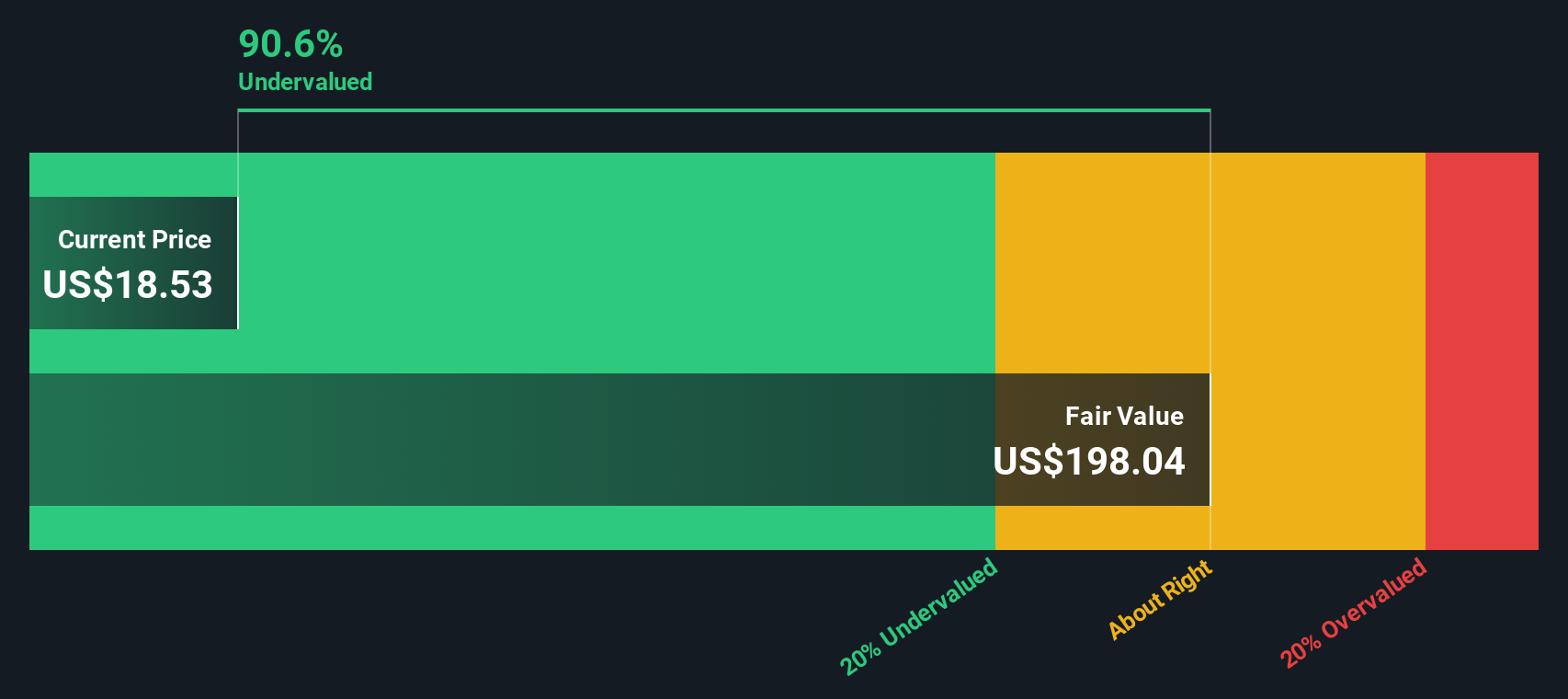

Another View: Is Sable Offshore Actually Undervalued?

While the price-to-book ratio presents Sable Offshore as expensive compared to its peers, our DCF model offers a markedly different perspective. According to this approach, Sable Offshore is trading well below its estimated fair value, which suggests the possibility of deep undervaluation. Could the market be missing the bigger picture?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sable Offshore for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sable Offshore Narrative

If you have a different perspective on Sable Offshore's outlook or want to dive deeper into the numbers yourself, you can shape your own view in minutes. Do it your way.

A great starting point for your Sable Offshore research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Opportunities are everywhere, but the smartest investors act before the crowd moves. If you want to potentially get ahead of the market, check out these handpicked ideas you shouldn’t miss:

Spot high-yield opportunities and power up your income strategy when you review these 19 dividend stocks with yields > 3% with strong payouts and reliable performance.

Tap into emerging trends by evaluating these 23 AI penny stocks that are driving innovation across industries and could redefine tomorrow’s tech landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks