Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:SFL

SFL Corporation Ltd. Beat Analyst Estimates: See What The Consensus Is Forecasting For Next Year

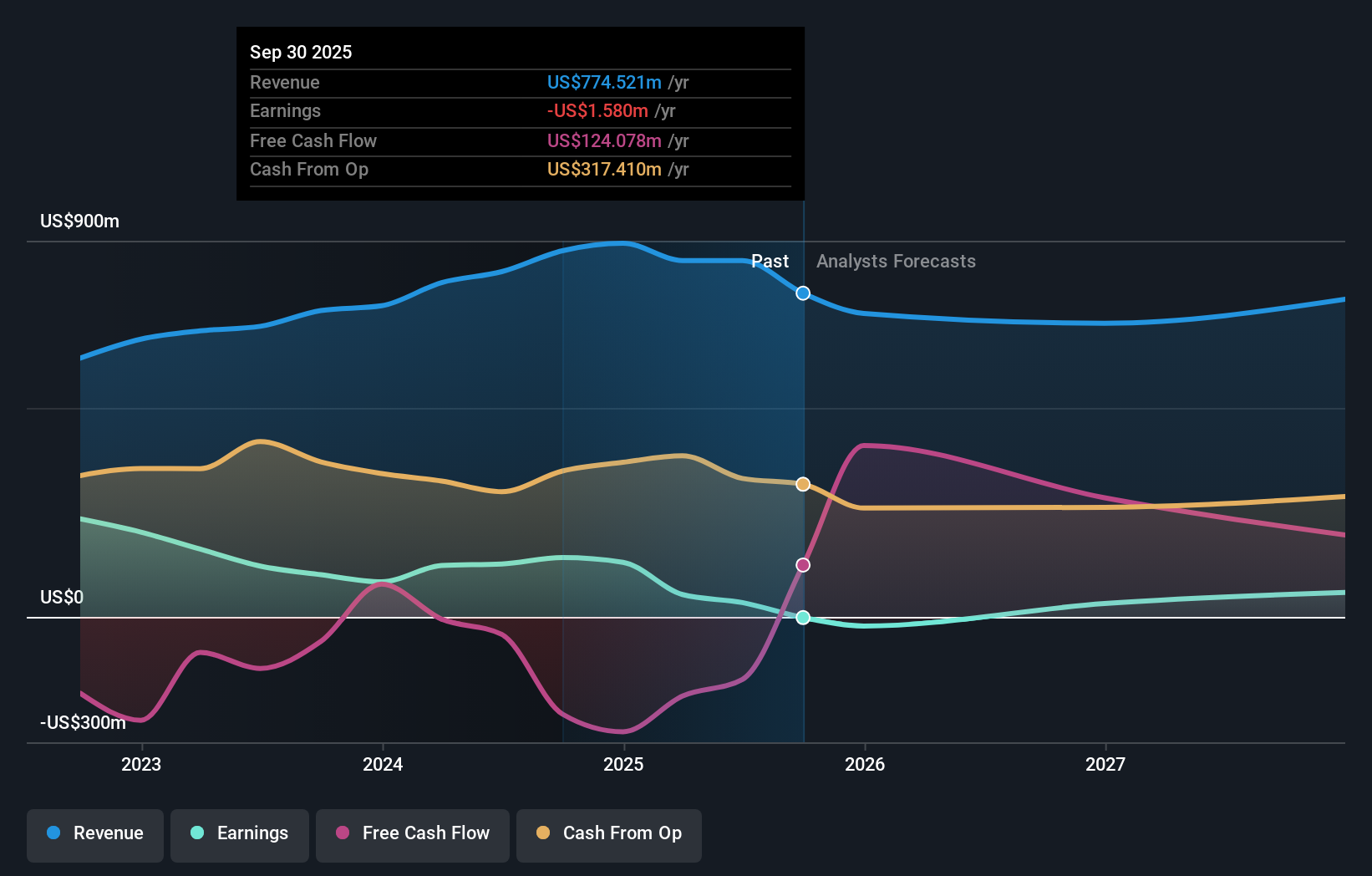

It's been a good week for SFL Corporation Ltd. (NYSE:SFL) shareholders, because the company has just released its latest quarterly results, and the shares gained 7.8% to US$8.19. SFL beat expectations by 2.7% with revenues of US$178m. It also surprised on the earnings front, with an unexpected statutory profit of US$0.07 per share a nice improvement on the losses that the analysts forecast. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Taking into account the latest results, the current consensus, from the three analysts covering SFL, is for revenues of US$702.7m in 2026. This implies an uncomfortable 9.3% reduction in SFL's revenue over the past 12 months. Earnings are expected to improve, with SFL forecast to report a statutory profit of US$0.24 per share. Before this earnings report, the analysts had been forecasting revenues of US$763.9m and earnings per share (EPS) of US$0.22 in 2026. Although the analysts have lowered their revenue forecasts, they've also made a substantial gain in their earnings per share estimates, which implies there's been something of an uptick in sentiment following the latest results.

View our latest analysis for SFL

The consensus has made no major changes to the price target of US$9.68, suggesting the forecast improvement in earnings is expected to offset the decline in revenues next year. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on SFL, with the most bullish analyst valuing it at US$11.40 and the most bearish at US$8.00 per share. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that revenue is expected to reverse, with a forecast 7.5% annualised decline to the end of 2026. That is a notable change from historical growth of 14% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 3.1% annually for the foreseeable future. It's pretty clear that SFL's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around SFL's earnings potential next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply they will perform worse than the wider industry. Even so, earnings are more important to the intrinsic value of the business. The consensus price target held steady at US$9.68, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for SFL going out to 2027, and you can see them free on our platform here.

Even so, be aware that SFL is showing 2 warning signs in our investment analysis , you should know about...

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SFL

SFL

A maritime and offshore asset owning and chartering company, engages in the ownership, operation, and chartering out of vessels and offshore related assets on medium and long-term charters.

Good value with moderate growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor