Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:KMI

How Investors Are Reacting To Kinder Morgan (KMI) Spotlighting Its $9.3 Billion Natural Gas Pipeline Backlog

Simply Wall St

Reviewed by Sasha Jovanovic

- In late November 2025, Mizuho highlighted Kinder Morgan's substantial US$9.3 billion project backlog, with US$8.4 billion tied to natural gas, following the company’s third-quarter earnings report that saw a modest EPS miss but better-than-expected revenue.

- An important insight is Mizuho’s increased medium- and long-term growth expectations for Kinder Morgan, citing upgraded forecasts for 2025–2029 and considerable confidence in the future contributions from its natural gas project pipeline.

- We'll now assess how Kinder Morgan's reinforced project backlog and growth outlook could influence its overall investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Kinder Morgan Investment Narrative Recap

To be a Kinder Morgan shareholder, you typically need to believe in sustained North American natural gas demand and the company’s ability to turn its large project backlog into steady contractual cash flows. The recent US$9.3 billion backlog highlighted by Mizuho supports the current growth outlook but does not significantly alter the main short-term catalyst: execution on expansion projects, or the greatest risk, Kinder Morgan’s high leverage, which continues to constrain financial flexibility. Among Kinder Morgan’s latest announcements, the recurring quarterly dividend increase stands out, with the Q3 2025 payout rising 2% over last year. This steady dividend policy is especially relevant as it reflects management’s confidence in future cash flows, which are closely tied to project completion and utilization, key catalysts given current expansion plans. Yet, it’s important for investors to remember that, despite upgraded growth expectations, Kinder Morgan’s financial flexibility remains limited by its...

Read the full narrative on Kinder Morgan (it's free!)

Kinder Morgan's narrative projects $20.2 billion revenue and $3.7 billion earnings by 2028. This requires 8.2% yearly revenue growth and a $1.0 billion increase in earnings from $2.7 billion today.

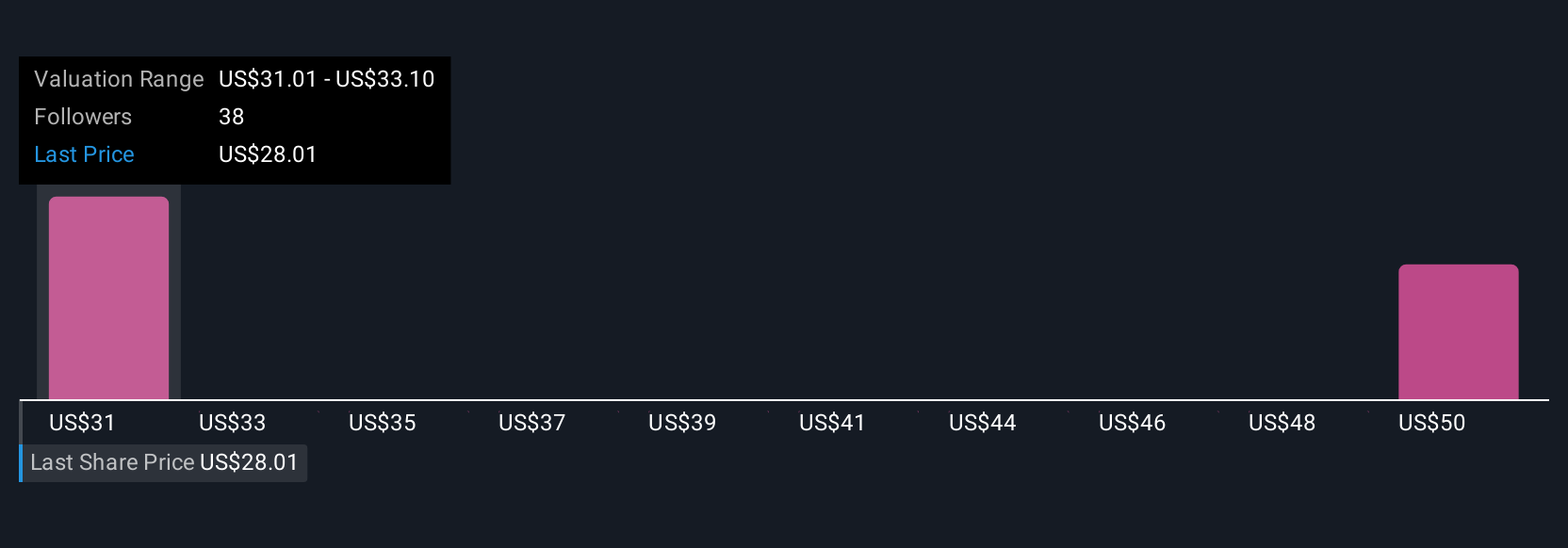

Uncover how Kinder Morgan's forecasts yield a $31.06 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members’ fair value estimates for Kinder Morgan range from US$31.06 up to US$49.19, based on 3 forecasts. Many see the robust project backlog as a driver, but views differ widely on future returns, explore the diversity of opinion for a fuller picture.

Explore 3 other fair value estimates on Kinder Morgan - why the stock might be worth as much as 80% more than the current price!

Build Your Own Kinder Morgan Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kinder Morgan research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Kinder Morgan research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kinder Morgan's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kinder Morgan might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KMI

Kinder Morgan

Operates as an energy infrastructure company primarily in North America.

Acceptable track record and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative