Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:FRO

Frontline (FRO) Is Up 5.6% After Q2 Revenue Tops Estimates but EPS Misses Forecasts—Has the Bull Case Changed?

Simply Wall St

Reviewed by Sasha Jovanovic

- Frontline Ltd recently achieved a new 52-week high following its Q2 2025 results, which saw revenue exceed expectations even as earnings per share fell short of forecasts.

- Analyst optimism, especially regarding sustained strong Very Large Crude Carrier rates and a favorable winter outlook, has contributed to heightened investor confidence in the company.

- We'll explore how Frontline's substantial Q2 revenue beat supports its long-term investment narrative amid industry supply constraints.

AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Frontline Investment Narrative Recap

For many investors, the core Frontline story centers on the durability of global seaborne oil demand and the company's exposure to favorable tanker rates, amid constrained vessel supply. Frontline's strong Q2 revenue surprise supports the short-term outlook for elevated Very Large Crude Carrier rates, but does not materially reduce the biggest risk, prolonged rate volatility if oil demand growth weakens due to shifting energy policies or macro headwinds.

Of the company's latest announcements, the Q2 2025 dividend declaration of US$0.36 per share directly reflects Frontline's ability to return capital to shareholders, even as earnings fell below analyst forecasts. This payout highlights the company's strategy of maintaining shareholder distributions alongside the ongoing catalyst of robust crude tanker demand and constrained fleet supply.

By contrast, investors should remain alert to the risk that a quick reversal in oil trade routes or easing of sanctions could...

Read the full narrative on Frontline (it's free!)

Frontline's outlook anticipates $1.3 billion in revenue and $828.1 million in earnings by 2028. This requires a 10.7% annual revenue decline and a $590.1 million increase in earnings from the current level of $238.0 million.

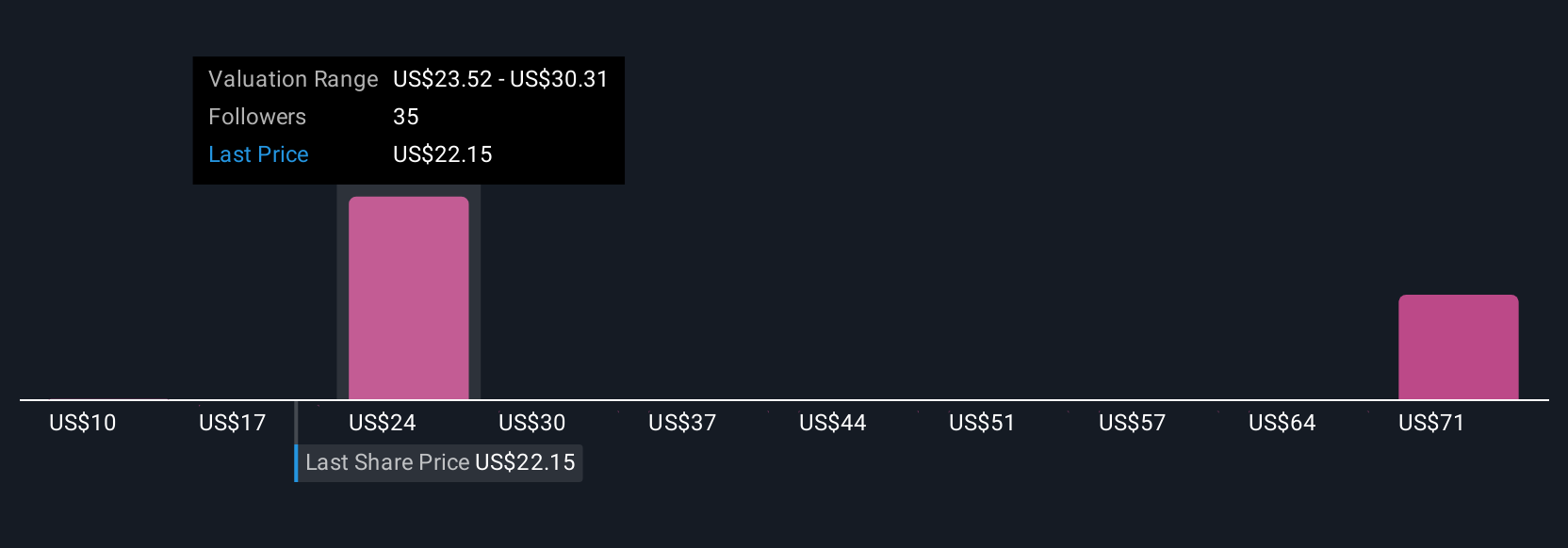

Uncover how Frontline's forecasts yield a $27.20 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members provided eight fair value estimates for Frontline, ranging widely from US$9.65 to US$94.67. With the current supply constraints supporting higher vessel utilization, viewpoints on Frontline's performance can differ greatly, explore these varied analyses for a broader understanding of potential outcomes.

Explore 8 other fair value estimates on Frontline - why the stock might be worth less than half the current price!

Build Your Own Frontline Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Frontline research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 27 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FRO

Frontline

A shipping company, engages in the ownership and operation of oil and product tankers worldwide.

Good value with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor