Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:EQT

EQT (EQT) Is Up 7.0% After Securing Major AI Data Center Gas Supply Deal – Has The Bull Case Changed?

Simply Wall St

Reviewed by Simply Wall St

- EQT Corporation recently announced an agreement to become the exclusive natural gas supplier for the Homer City Energy Campus, a major 4.4-gigawatt data center and power project in Pennsylvania, underpinning what is considered one of the largest single-site natural gas purchases in North American history.

- This development positions EQT as a central enabler of infrastructure supporting advanced computing while increasing long-term demand for its natural gas production.

- We'll explore how providing fuel to a massive AI-focused energy campus could influence EQT’s previously established investment narrative.

EQT Investment Narrative Recap

To be an EQT shareholder, you must believe in the company's ability to capture regional demand growth and monetize major partnerships like the Homer City Energy Campus project, all while managing exposure to volatile gas prices and integrating acquisitions without overstressing cash flows. The Homer City deal directly supports EQT's most important short-term catalyst, in-basin gas demand from large-scale power and data projects, while also adding potential risks if these long-cycle developments face delays or underperform; however, the project's long timeline means immediate financial impact may be limited.

Among EQT’s recent announcements, the affirmation of a quarterly cash dividend at US$0.1575 per share signals confidence in near-term cash generation and shareholder returns, despite capital demands from growth initiatives such as Homer City that may affect liquidity and future dividends if market conditions shift unexpectedly.

But in contrast to this sense of progress, investors should be aware of what happens if cash flows come under pressure from ...

Read the full narrative on EQT (it's free!)

EQT's narrative projects $9.0 billion revenue and $3.4 billion earnings by 2028. This requires 13.4% yearly revenue growth and an increase of approximately $3.0 billion in earnings from the current $369.2 million.

Uncover how EQT's forecasts yield a $56.67 fair value, a 4% downside to its current price.

Exploring Other Perspectives

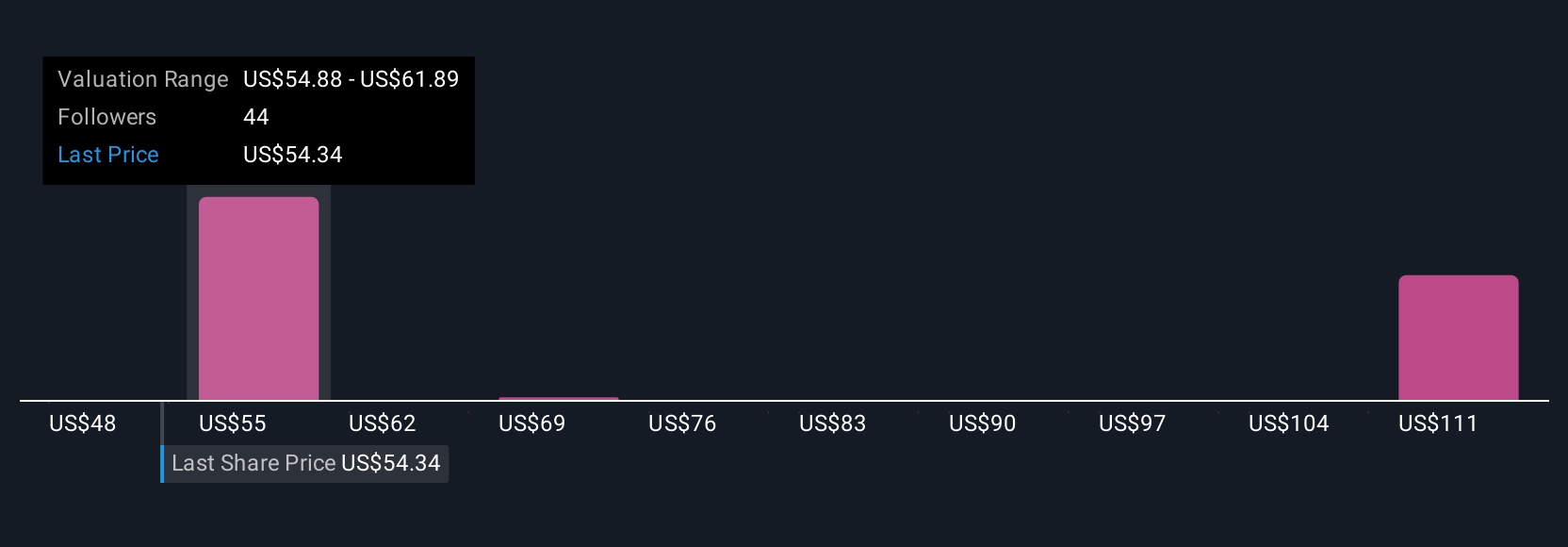

Five fair value estimates from the Simply Wall St Community span US$47.87 to US$119.34 per share, reflecting a broad spectrum of individual outlooks. While perspectives diverge widely, all eyes remain on EQT’s ability to grow in-basin demand through large-scale projects, a factor critical to supporting future performance amid sector uncertainties.

Build Your Own EQT Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your EQT research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free EQT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EQT's overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- These 17 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EQT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EQT

EQT

Engages in the production, gathering, and transmission of natural gas.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor