Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:DTM

DT Midstream (DTM): Assessing Valuation After Guardian Pipeline Capacity Expansion Announcement

Simply Wall St

Reviewed by Kshitija Bhandaru

DT Midstream (DTM) just revealed it has closed a binding open season for expansion capacity on its Guardian Pipeline. This move boosts total awarded capacity by 40% over current levels and highlights continued demand for pipeline infrastructure.

See our latest analysis for DT Midstream.

Shares of DT Midstream haven’t made any dramatic moves lately, but investors have enjoyed a steady climb, with a one-year total shareholder return of 40.6% and compounding momentum over the past three years. Recent milestones such as the Guardian Pipeline expansion and a new executive leadership appointment suggest that management is focused on positioning the company for long-term growth and reliability.

If infrastructure projects like this have you looking for the next breakout, broaden your search and discover fast growing stocks with high insider ownership

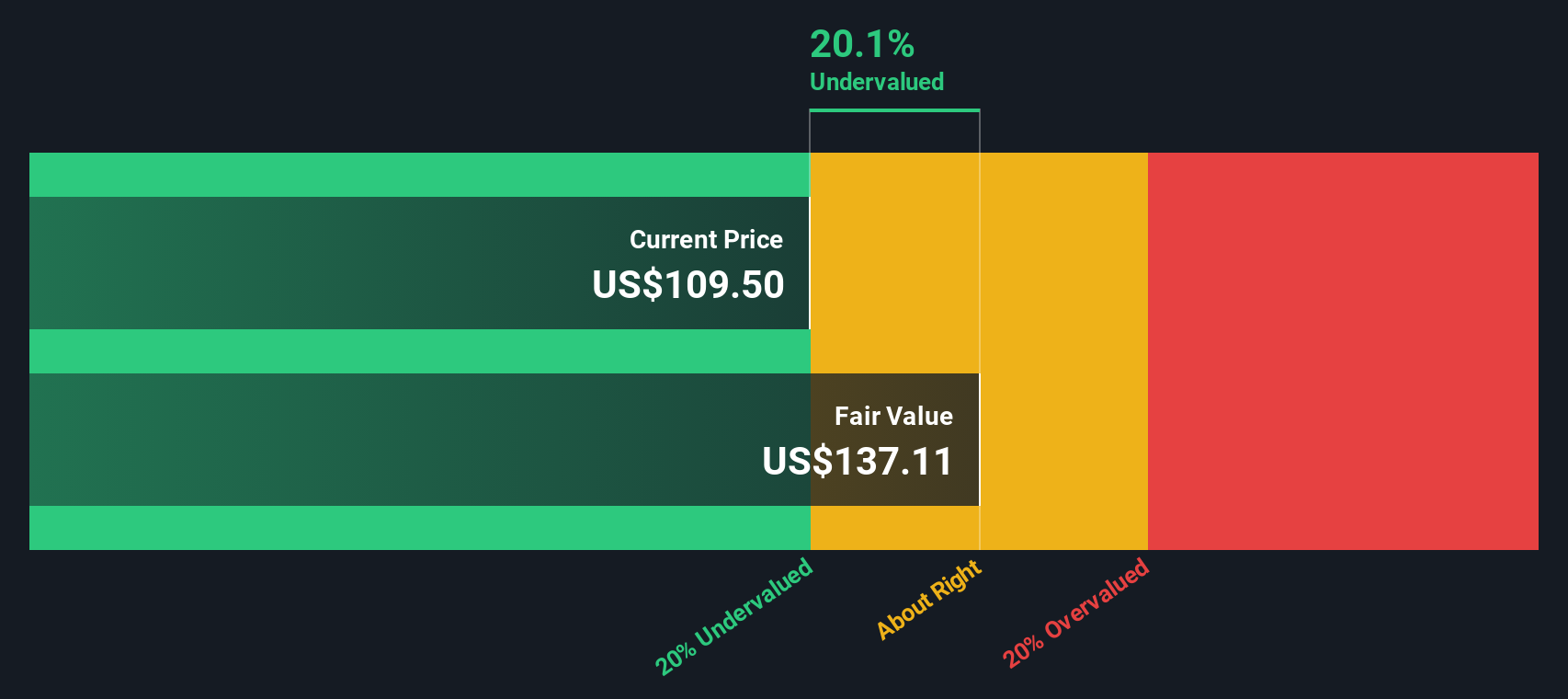

But with shares up over 40% in the past year and trading close to analyst price targets, investors may wonder whether DT Midstream is still undervalued or if the market has already factored in this future growth opportunity.

Most Popular Narrative: 2.7% Overvalued

With DT Midstream’s fair value pegged at $111.46, the last close at $114.49 leaves shares slightly above what the most widely followed narrative considers justified. This small premium raises questions about the strength behind the company's financial outlook and what assumptions are fueling the current enthusiasm.

Strategic focus on long-term, fee-based contracts with investment-grade counterparties (such as the 20-year Guardian expansion anchor) reduces earnings volatility and enhances net profit margins, supporting visible, durable cash flow and dividend increases.

Want to know the backbone of this premium price? Profit margins are set to climb, but it all hinges on a financial formula unique to this sector. Curious what revenue and earnings projections the narrative is betting on? See what sets this valuation apart from the crowd.

Result: Fair Value of $111.46 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, a slowdown in natural gas demand or unexpected regulatory shifts could quickly challenge DT Midstream’s anticipated growth and earnings outlook.

Find out about the key risks to this DT Midstream narrative.

Another View: What Does Our DCF Model Say?

While the analyst consensus pegs DT Midstream as slightly overvalued, the SWS DCF model offers a different perspective. According to this approach, shares are currently trading about 16.6% below their estimated fair value of $137.35. This suggests there could be meaningful potential upside for patient investors.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out DT Midstream for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own DT Midstream Narrative

If you see things differently or want to dive into the numbers for yourself, creating your own narrative is quick and easy. Do it your way

A great starting point for your DT Midstream research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors always keep new opportunities on their radar. Take action now and uncover unique trends or growth stories that could set your portfolio apart.

- Supercharge your returns by spotting these 896 undervalued stocks based on cash flows that the market has yet to price in. Find tomorrow’s winners before everyone else.

- Capture high-yield income potential from these 19 dividend stocks with yields > 3% paying over 3% and make your cash work harder for you.

- Position yourself at the forefront of tech innovation with these 24 AI penny stocks growing fast on the back of artificial intelligence breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DTM

DT Midstream

Provides integrated natural gas services in the United States.

Mediocre balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor