Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:DKL

A Look at Delek Logistics Partners (DKL) Valuation as Quarterly Distribution Rises for Q3 2025

Simply Wall St

Reviewed by Simply Wall St

Delek Logistics Partners (NYSE:DKL) just announced an increased quarterly cash distribution for the third quarter of 2025, setting the payout at $1.12 per common limited partner unit, or $4.48 annually. This move highlights the partnership’s continued focus on cash flow strength and rewarding unitholders.

See our latest analysis for Delek Logistics Partners.

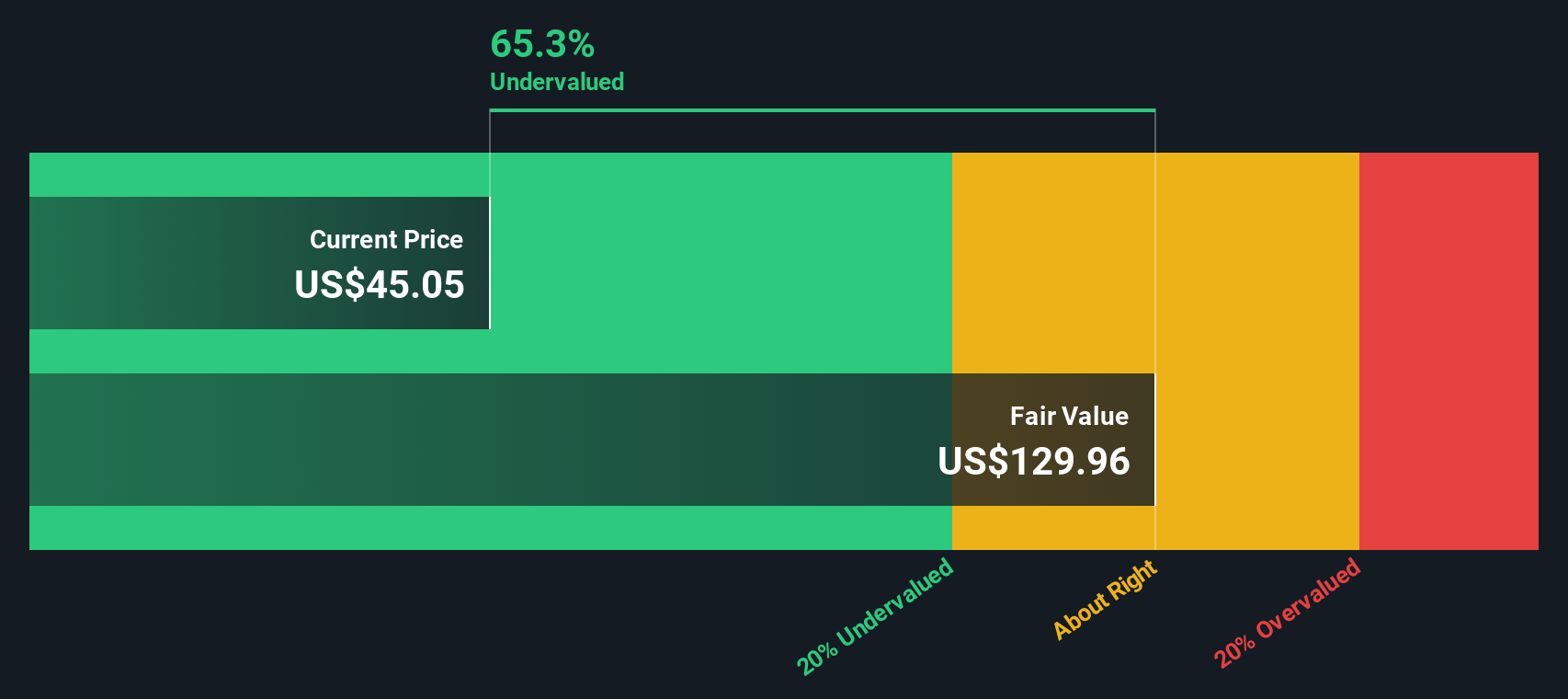

Following this distribution hike, Delek Logistics Partners has captured renewed investor attention. Its share price is now at $45.13 and it has achieved a 27.93% total shareholder return over the past year. Strong results have supported momentum, reflecting both consistent payouts and longer-term value creation.

If you want to broaden your search for income plays with strong fundamentals, this is a great time to discover fast growing stocks with high insider ownership

With the stock now delivering steady gains and another payout increase, the question is whether these strengths signal an undervalued opportunity or if the current price already reflects all the anticipated growth ahead.

Most Popular Narrative: 3.2% Overvalued

With Delek Logistics Partners trading just above the narrative's fair value, the small premium means growth assumptions are playing a crucial role in justifying the current share price. This narrative focuses on future operational expansions and their impact on earnings as a key catalyst.

The full commissioning and expected ramp to capacity of the new Libby 2 gas plant in the Delaware Basin, along with associated investments (amine unit and AGI wells), positions Delek Logistics to capitalize on rising energy demand and stable domestic energy infrastructure needs, which could boost gathering and processing volumes, EBITDA, and revenue growth.

The real story behind this small valuation premium? The narrative is balancing expected gains from new assets and a profit margin increase that surpasses the industry. Want to know which projections drive this target? Find out what’s behind the numbers by reading the complete narrative for the full picture.

Result: Fair Value of $43.75 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, recent acquisitions and heavy capital outlays could backfire if fossil fuel demand falls or if financial leverage becomes difficult to manage.

Find out about the key risks to this Delek Logistics Partners narrative.

Another View: What About Discounted Cash Flow?

Our SWS DCF model suggests a radically different perspective. It estimates Delek Logistics Partners’ fair value at $154.63 per unit, which is far above the current price. This hints at substantial upside if cash flows play out as projected. Is the market missing something, or are analysts too optimistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Delek Logistics Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 849 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Delek Logistics Partners Narrative

If you have a different perspective or want to dig into the details yourself, you can build your own view from the ground up in just minutes. Do it your way

A great starting point for your Delek Logistics Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let great opportunities slip by. The Simply Wall Street Screener makes it easy to spot standout stocks in growing markets and powerful trends quickly.

- Uncover rising stars with massive potential by starting your search with these 3606 penny stocks with strong financials, which show strong financials and growth momentum.

- Capture the future of medicine and technology by targeting companies at the forefront of innovation using these 33 healthcare AI stocks.

- Boost your passive income with attractive yields by selecting from these 20 dividend stocks with yields > 3%, which consistently reward shareholders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DKL

Delek Logistics Partners

Provides gathering, pipeline, transportation, and other services for crude oil, intermediates, refined products, natural gas, storage, wholesale marketing, terminalling water disposal and recycling customers in the United States.

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

55 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

49 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

55 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative