- United States

- /

- Healthcare Services

- /

- NYSE:EHAB

Exploring Delek US Holdings And Two More Undervalued Small Caps With Insider Actions In The United States

Reviewed by Simply Wall St

The United States stock market has experienced a dip of 2.4% over the last week, although it has risen by 18% over the past year with earnings expected to grow by 15% annually. In this context, identifying undervalued small-cap stocks with insider buying can be particularly compelling, as these actions often signal potential unrecognized value in a fluctuating market.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Hanover Bancorp | 8.5x | 1.9x | 48.69% | ★★★★★☆ |

| Ramaco Resources | 12.4x | 1.0x | 19.98% | ★★★★★☆ |

| AtriCure | NA | 2.8x | 46.76% | ★★★★★☆ |

| Franklin Financial Services | 9.9x | 2.0x | 31.08% | ★★★★☆☆ |

| PCB Bancorp | 10.9x | 2.9x | 32.31% | ★★★★☆☆ |

| Columbus McKinnon | 23.9x | 1.1x | 43.30% | ★★★★☆☆ |

| Titan Machinery | 4.3x | 0.1x | 18.52% | ★★★★☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| Alta Equipment Group | NA | 0.2x | -237.84% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -132.83% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Delek US Holdings (NYSE:DK)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Delek US Holdings is an energy company primarily engaged in petroleum refining, with additional operations in retail fuel and logistics, boasting a market capitalization of approximately $1.22 billion.

Operations: Refining constitutes the predominant revenue stream for the entity, generating $15.72 billion, complemented by contributions from Retail and Logistics amounting to $871.2 million and $1.029 billion respectively. The Gross Profit Margin over recent periods shows a fluctuating trend with current figures at approximately 5.79%, reflecting variability in operational efficiency and market conditions.

PE: -19.1x

Despite a challenging quarter where Delek US Holdings reported a net loss and a drop in sales, their strategic inclusion in multiple Russell indexes underscores market recognition of potential growth. With insider confidence reflected through substantial share repurchases totaling $485.21 million, the firm demonstrates commitment to enhancing shareholder value. Additionally, an increase in dividends suggests optimism about future cash flows, positioning this entity intriguingly for those eyeing undervalued opportunities within dynamic sectors.

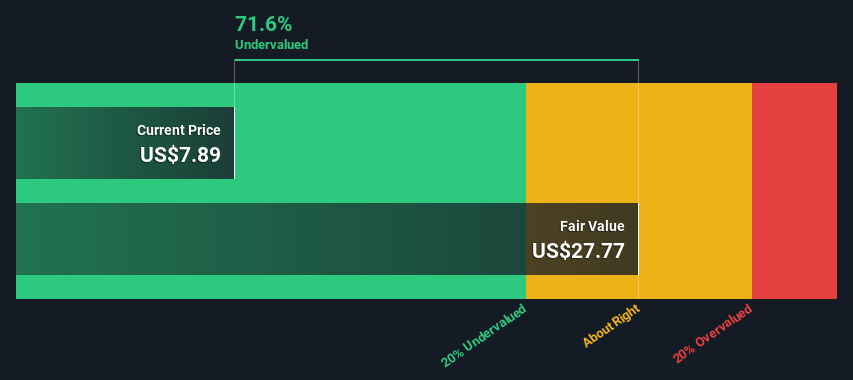

Enhabit (NYSE:EHAB)

Simply Wall St Value Rating: ★★★★★☆

Overview: Enhabit operates in the healthcare sector, providing hospice and home health services with a market capitalization of approximately $1.04 billion.

Operations: The company generated a gross profit of $506.40 million with a gross profit margin of 48.52% in the most recent quarter, reflecting its cost management in relation to revenue of $1043.60 million. Over the past years, gross profit margins have shown a slight decline from 51.70% in 2019 to current levels, indicating changes in cost dynamics or pricing strategies within the operational framework.

PE: -6.2x

Recently, Enhabit has been a focal point of investor activism, with significant boardroom challenges and strategic reviews influencing its trajectory. Amidst this backdrop, the company's earnings are projected to surge by 105% annually. Insider confidence is reflected through recent purchases, underscoring a belief in the firm’s potential despite external pressures and operational critiques from entities like AREX Capital Management. Added to key growth indices like the Russell 2000, Enhabit exemplifies a promising yet undervalued entity within its sector, poised for recalibration and growth.

- Take a closer look at Enhabit's potential here in our valuation report.

Evaluate Enhabit's historical performance by accessing our past performance report.

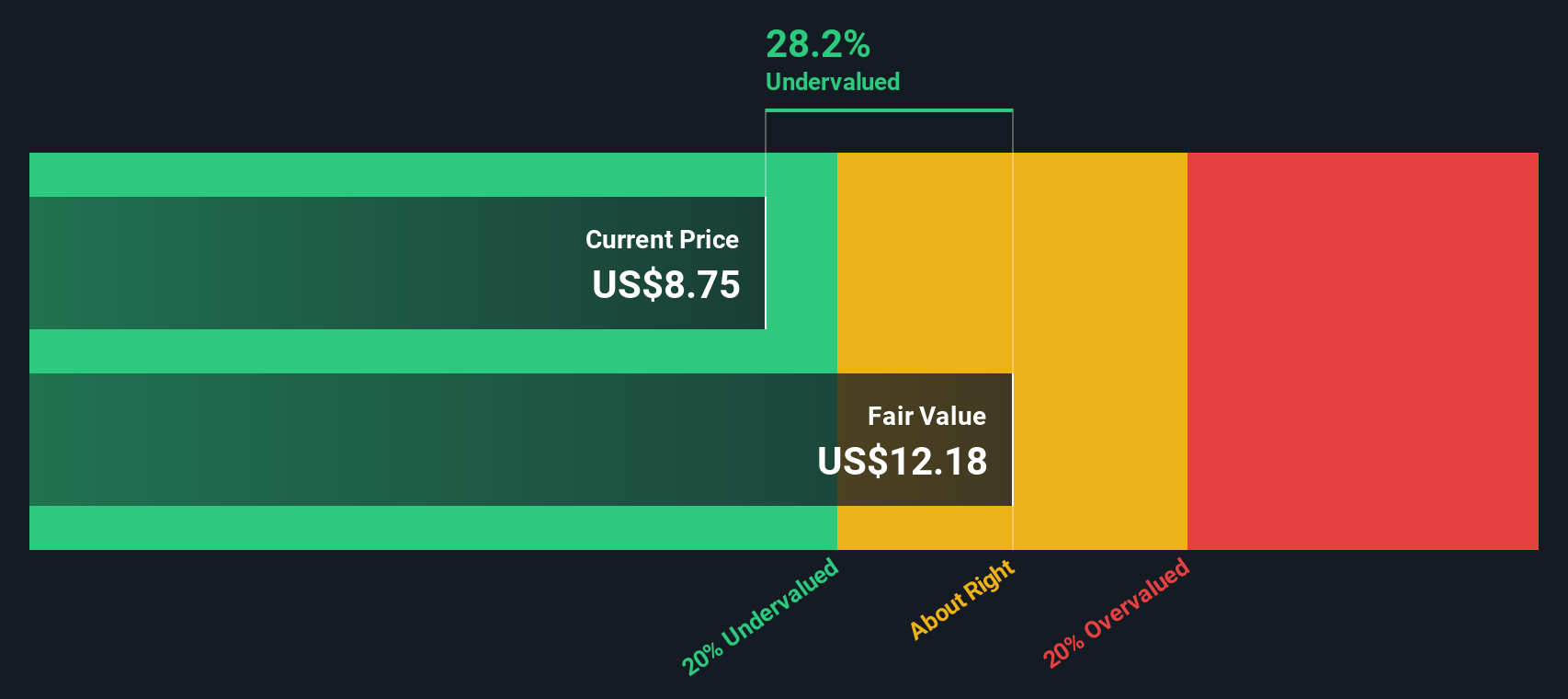

Enviri (NYSE:NVRI)

Simply Wall St Value Rating: ★★★★★☆

Overview: Enviri is a diversified company with operations in environmental solutions, including the Clean Earth and Harsco Environmental segments, boasting a market capitalization of approximately $2.11 billion.

Operations: Clean Earth and Harsco Environmental are the primary revenue segments for the company, generating $931.89 million and $1.17 billion respectively. The gross profit margin has seen a fluctuation over recent periods, with the latest recorded at 21.29%.

PE: -16.0x

Enviri, a burgeoning entity in the market, recently projected its 2027 revenues to touch US$2.7 billion, signaling robust growth prospects. Despite a net loss in Q1 2024, revised upward guidance for the year suggests improving operational efficiency. Insider confidence is evident as they recently purchased shares, underscoring belief in the company’s trajectory. With no high-risk funding dependencies and a strategic ESOP-related offering initiated, Enviri stands out for its financial prudence and insider-endorsed potential.

- Navigate through the intricacies of Enviri with our comprehensive valuation report here.

Assess Enviri's past performance with our detailed historical performance reports.

Summing It All Up

- Delve into our full catalog of 66 Undervalued US Small Caps With Insider Buying here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Enhabit might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EHAB

Very undervalued with moderate growth potential.