- United States

- /

- Oil and Gas

- /

- NYSE:COP

ConocoPhillips (COP): Assessing Valuation After a Recent Pullback and Modest Short-Term Rebound

Reviewed by Simply Wall St

ConocoPhillips (COP) has been treading water lately, with the stock down slightly over the past week but up over the past month. This has left investors wondering whether the recent pullback is a chance to add exposure.

See our latest analysis for ConocoPhillips.

Zooming out, ConocoPhillips has seen its share price drift lower year to date while the recent 30 day share price return has turned positive, hinting that selling pressure may be easing even as the multi year total shareholder return remains strong.

If this kind of steady energy name is on your radar, it could also be worth exploring other aerospace and defense stocks that might offer different growth and risk profiles.

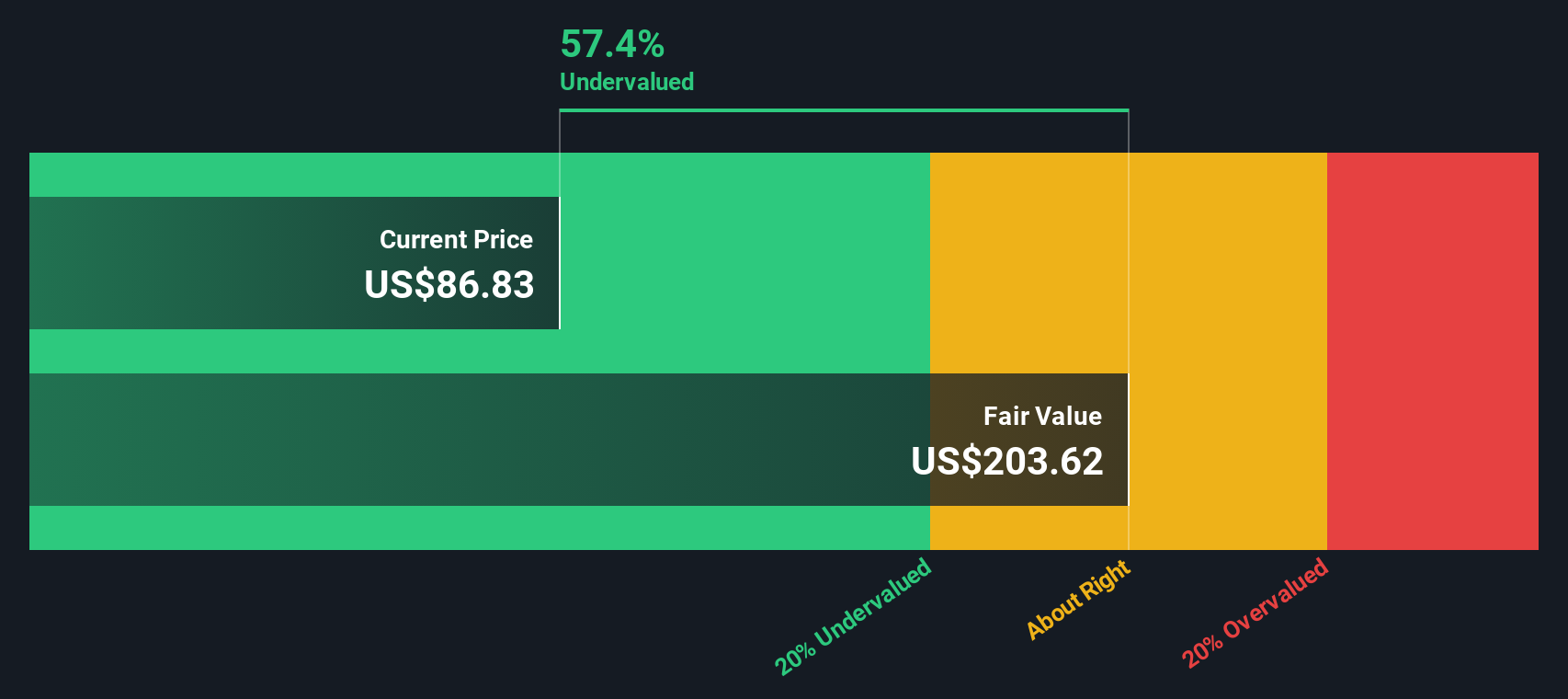

With shares trading below Wall Street targets and some models suggesting a steeper intrinsic discount, COP’s muted recent returns raise the key question: is this value hiding in plain sight, or is future growth already fully priced in?

Most Popular Narrative Narrative: 18.2% Undervalued

Compared with the last close at $91.94, the most widely followed narrative points to a higher fair value, framing COP as meaningfully mispriced today.

The company's expanding LNG portfolio and progress on large-scale liquefaction projects (notably in Qatar, Port Arthur, and Willow) are set to capture significant market share from robust global gas demand, especially as natural gas solidifies its role as a "transition fuel"; these projects are expected to drive a substantial free cash flow inflection and topline revenue expansion through 2029.

Want to see what powers that upbeat valuation view? The narrative leans on a subtle revenue reset, fatter margins, and a future earnings multiple that might surprise you.

Result: Fair Value of $112.39 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that optimism could be challenged if large capital projects face delays or if weaker commodity prices squeeze the free cash flow ramp analysts expect.

Find out about the key risks to this ConocoPhillips narrative.

Another Lens on Value

Our SWS DCF model presents a far more aggressive picture, suggesting COP is trading at a steep discount to its long term cash flow potential, even deeper than the narrative fair value implies. If both are correct, the market may be overly cautious about future energy prices and project execution.

Look into how the SWS DCF model arrives at its fair value.

Build Your Own ConocoPhillips Narrative

If you see the story differently or want to stress test the assumptions using your own research, you can build a fresh view in just a few minutes, Do it your way

A great starting point for your ConocoPhillips research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Do not stop at a single opportunity when your next smart move could be waiting in plain sight. Use the Simply Wall Street Screener before the market gets there first.

- Target potential multi baggers early by scanning these 3625 penny stocks with strong financials that pair tiny share prices with solid underlying financials and momentum.

- Position yourself for the next wave of innovation by tracking these 24 AI penny stocks harnessing artificial intelligence to reshape entire industries and profit pools.

- Explore income potential with these 13 dividend stocks with yields > 3% that combine yields above 3 percent with balance sheets built to support long term payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:COP

ConocoPhillips

Explores for, produces, transports, and markets crude oil, bitumen, natural gas, liquefied natural gas (LNG), and natural gas liquids.

Excellent balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion