If you are watching Diamondback Energy (FANG) after the company’s latest announcement, you are not alone. The company just raised its third quarter 2025 production outlook, increasing both its oil output and total net production targets. At a time when energy markets are hardly predictable, an upward revision like this suggests Diamondback’s wells are hitting performance marks that even management did not anticipate just a quarter ago.

This latest move follows a mixed year for Diamondback. While the stock has posted a 9% gain over the last three months, recovering from a challenging year with a 23% drop, momentum may be shifting as the market digests the new guidance and considers signs of stabilizing operations. Over the past five years, Diamondback’s return remains notable, but the recent shift in sentiment around energy stocks is encouraging investors to stay alert.

With this positive revision in production, a key question remains: Is the market overlooking an opportunity in Diamondback, or has the optimism around growth already been reflected in the current stock price?

Advertisement

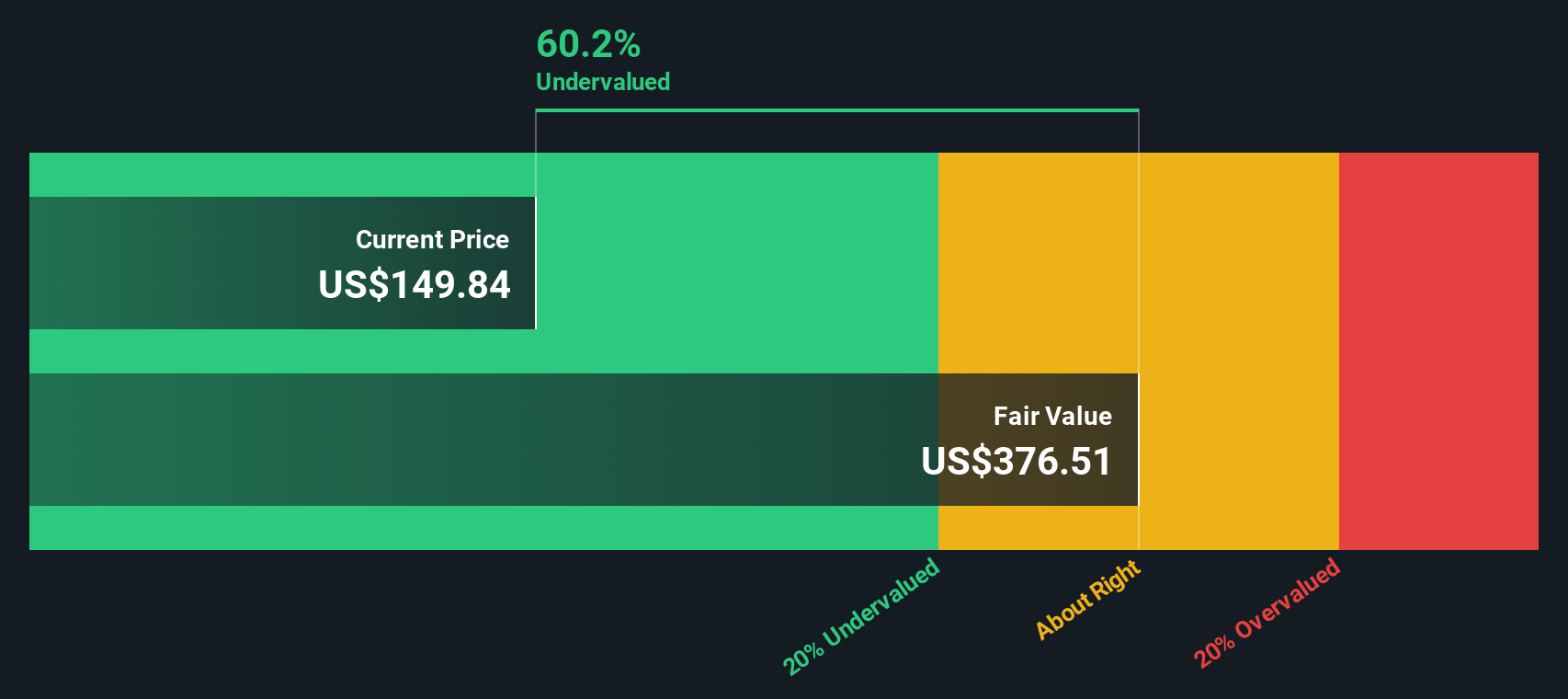

Most Popular Narrative: 19.4% Undervalued

According to community narrative, Diamondback Energy is currently trading below what analysts believe to be its fair value. There is a strong case for future potential based on earnings growth and efficiency-driven expansion. The consensus view is that the company is undervalued, with robust operational improvements and industry-leading cost management cited as major catalysts for price appreciation.

Ongoing consolidation in the Permian Basin positions Diamondback as the "consolidator of choice" because of its industry-best integration, low cost structure, and demonstrated ability to deliver synergies from recent large acquisitions (for example, Double Eagle and Endeavor). This supports expectations for future growth in scale, cost savings, and higher EBITDA margins.

The factors fueling this discount include strategic acquisitions, significant operational upgrades, and a clear plan for higher margins. If you are interested in projections for profits or in which milestone numbers may impact this valuation, the full report explores the forecasts and key targets that support this analyst consensus.

However, rising operating costs in the Permian and declines in premium drilling inventory could pressure Diamondback’s margins and create challenges for its long-term growth outlook.

Our SWS DCF model tells a similar story, suggesting Diamondback is also undervalued when you look at its future cash flows, rather than just market multiples. Does this alignment boost your confidence or deepen your curiosity?

If you would rather reach your own conclusions or take a different perspective, the tools are here for you to investigate and shape your own in just a few minutes. Do it your way

A great starting point for your Diamondback Energy research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Do not let your next big opportunity slip by. The Simply Wall Street Screener is designed to help you identify stocks with the potential to outperform your expectations. Give yourself an advantage and review these handpicked themes tailored for forward-thinking investors:

Uncover hidden value by targeting companies that are likely undervalued based on future cash flows with undervalued stocks based on cash flows locked in.

Generate recurring income with a focus on top performers yielding over 3%. Check out dividend stocks with yields > 3% and see how the strongest dividend payers compare.

Jump ahead of the curve in artificial intelligence disruption with AI penny stocks at the forefront of innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

An independent oil and natural gas company, acquires, develops, explores, and exploits unconventional, onshore oil and natural gas reserves in the Permian Basin in West Texas.