Baker Hughes (BKR) has caught attention recently as investors evaluate its current position and the company’s performance over the past few months. Share prices have climbed steadily, gaining 6% in the past month and 19% year to date.

Momentum has clearly been building for Baker Hughes lately, with a 1-month share price return of 6.3% and a solid year-to-date gain of over 19%. This recent climb follows a string of impressive long-term results, as the company's 5-year total shareholder return sits at an outstanding 186%.

If Baker Hughes’ run has you wondering where else strong momentum and growth might be playing out, now is a great time to broaden your search and discover fast growing stocks with high insider ownership

But with shares trading close to analyst targets and strong momentum behind them, investors need to ask whether Baker Hughes is undervalued at this stage or if the recent gains indicate that markets are already priced for future growth.

Advertisement

Most Popular Narrative: 5.7% Undervalued

Based on the prevailing narrative, Baker Hughes shares last closed at $49.53, while the fair value is pegged at $52.52. The gap suggests room for potential upside, with the narrative framing this advantage in the context of sector momentum and strategic positioning.

The company's strong momentum in securing large-scale service contracts, framework agreements, and technology-driven orders (such as for data centers, LNG, CCS, and recurring gas tech services) is driving an all-time high IET backlog. This is building strong visibility into future revenue and supporting sustained earnings durability.

Curious what’s really powering this premium? The secret ingredient is a combination of surging service backlogs and ambitious future profit assumptions. Want the whole formula behind this eye-catching valuation? Take a closer look to discover which forecasts and structural bets are fueling expectations for Baker Hughes’ next chapter.

However, risks such as persistent cost inflation and continued exposure to volatile oil and gas markets could challenge Baker Hughes' projected growth and margin expansion.

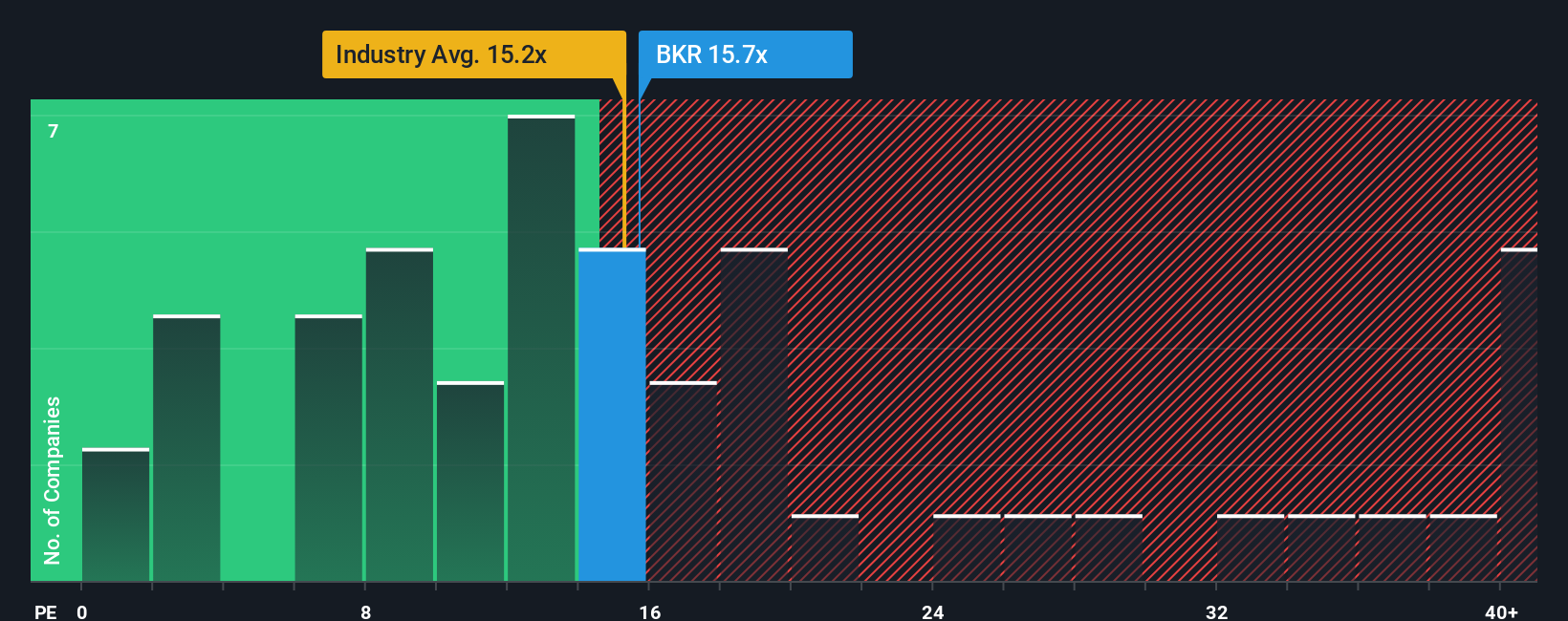

While some models see Baker Hughes as undervalued, looking at the price-to-earnings ratio paints a more nuanced picture. Baker Hughes trades at 16.9x earnings, slightly above its industry average of 16.8x and the peer average of 16.1x. However, it remains below the fair ratio of 17.7x. This suggests upside may still exist but is not guaranteed. Are investors being too cautious, or is the risk premium justified?

If you think the story goes deeper or want to bring your own data-driven perspective, it only takes a few minutes to create your own view. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Baker Hughes.

Looking for More Investment Ideas?

Smart investors never limit their watchlist. Give yourself an edge by using the Simply Wall Street Screener. These opportunities are moving fast, so secure your spot early.

Capitalize on surging demand in artificial intelligence by tracking these 25 AI penny stocks, which are poised to disrupt industries with their groundbreaking tech and real-world applications.

Grow your income potential by reviewing these 15 dividend stocks with yields > 3%, which features steady yields above 3% and highlights companies that stand out for consistency and financial strength.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Baker Hughes might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.