Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:WU

What Does WU’s Move to the SmallCap Index Reveal About Its Place in Digital Finance?

Simply Wall St

Reviewed by Sasha Jovanovic

- Western Union was recently removed from the S&P MidCap 400 and added to the S&P SmallCap 600, reflecting its shrinking market capitalization and ongoing financial challenges.

- This index change signals a shift in how the market views Western Union’s size and position amid digital competition and declining revenue growth.

- We’ll explore how Western Union’s move to the SmallCap index raises new questions about its long-term industry relevance and investment outlook.

The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Western Union Investment Narrative Recap

To be a shareholder in Western Union today, you need to believe the company’s shift to digital payments and new consumer services can outpace both regulatory headwinds and fast-moving digital competitors. The recent S&P index demotion highlights shrinking market value and operational pressures, but does not materially affect the core catalyst, digital transformation, or the key risk, which is persistent revenue softness due to U.S. immigration policy and digital disruptors attacking traditional channels.

Among Western Union’s recent announcements, the alliance with dLocal stands out as it expands digital payment options in Latin America, aligning with the company’s stated goal to capture more digital transaction volume. As the main catalyst remains the transition to digital services and alternatives, investors are watching to see if partnerships like this can meaningfully strengthen growth and offset ongoing declines elsewhere.

Yet, in contrast to these digital ambitions, the potential for tighter U.S. immigration controls poses ongoing risks that investors should be aware of, especially if...

Read the full narrative on Western Union (it's free!)

Western Union's narrative projects $4.3 billion in revenue and $543.0 million in earnings by 2028. This requires 1.3% yearly revenue growth and a decrease of $353.1 million in earnings from current earnings of $896.1 million.

Uncover how Western Union's forecasts yield a $9.32 fair value, a 16% upside to its current price.

Exploring Other Perspectives

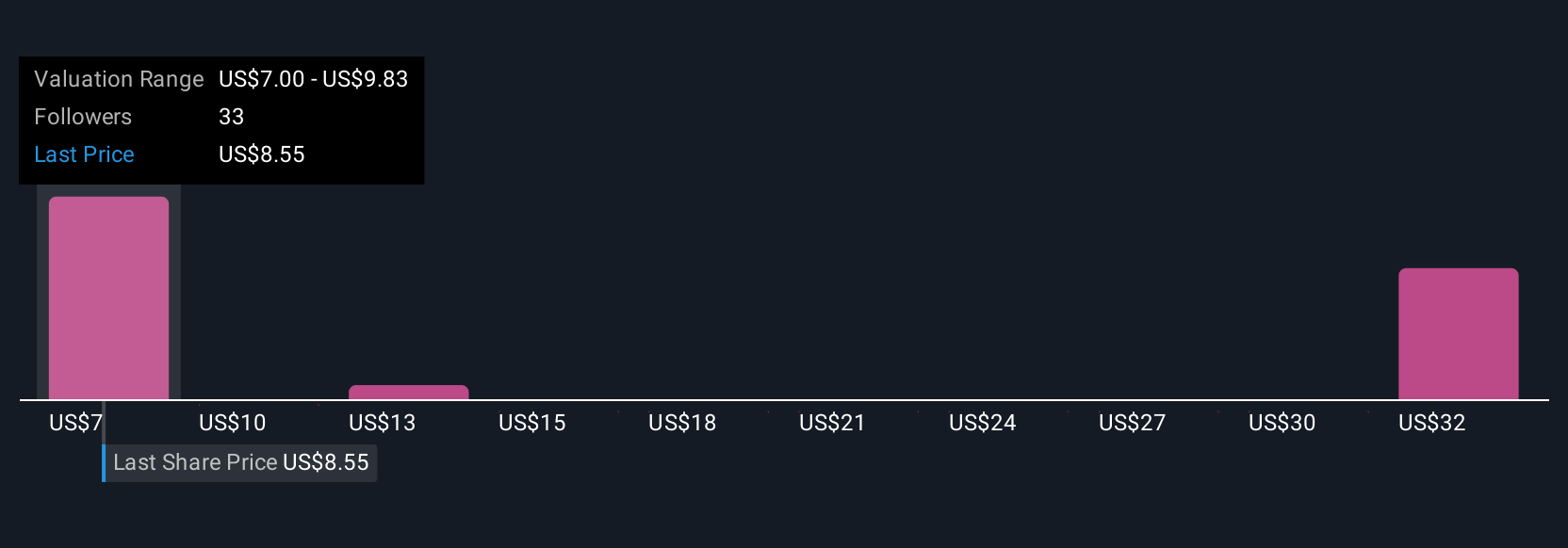

Ten private investors in the Simply Wall St Community estimate Western Union’s fair value broadly, from US$7 to US$36.71. Despite aggressive digital expansion, many see long-term threats from digital-first competitors as central to future performance, check out several viewpoints before making up your mind.

Explore 10 other fair value estimates on Western Union - why the stock might be worth 13% less than the current price!

Build Your Own Western Union Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Western Union research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Western Union research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Western Union's overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 33 companies in the world exploring or producing it. Find the list for free.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Western Union might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WU

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor