Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:WU

Did CFO’s Stock Purchase and Digital Moves Just Shift Western Union’s (WU) Investment Narrative?

Simply Wall St

Reviewed by Simply Wall St

- Earlier this week, Western Union's CFO Matthew Cagwin purchased 17,500 shares of company stock following the latest earnings call, which highlighted growth in digital and consumer services as well as ongoing acquisitions in Europe amid revenue and transaction volume declines.

- This substantial insider buying comes as Western Union explores stablecoin integration and pursues its Evolve 2025 strategy to drive future growth through digital transformation and improved compliance.

- We'll examine how the CFO's investment and focus on digital innovation may influence Western Union's investment narrative going forward.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Western Union Investment Narrative Recap

To invest in Western Union, you have to believe the company can successfully accelerate its digital transformation and regain transaction growth, especially as competition and regulatory pressures mount. The recent insider buying by the CFO may boost short-term investor confidence, but it does not fundamentally change the most important catalyst, digital adoption, or lessen the risk of ongoing revenue declines from competitive and regulatory headwinds.

One announcement closely connected to this narrative is Western Union’s move to explore stablecoin integration. This step aligns with the company’s Evolve 2025 strategy and represents a clear effort to remain competitive, as the industry’s shift toward digital and blockchain-based solutions could prove pivotal for future transaction growth.

In contrast, investors should not overlook the ongoing risk that new regulations or declining transaction volumes may weigh further on...

Read the full narrative on Western Union (it's free!)

Western Union's outlook points to $4.3 billion in revenue and $543.0 million in earnings by 2028. This implies a modest 1.3% annual revenue growth but a significant earnings decrease of $353.1 million from current earnings of $896.1 million.

Uncover how Western Union's forecasts yield a $9.32 fair value, a 7% upside to its current price.

Exploring Other Perspectives

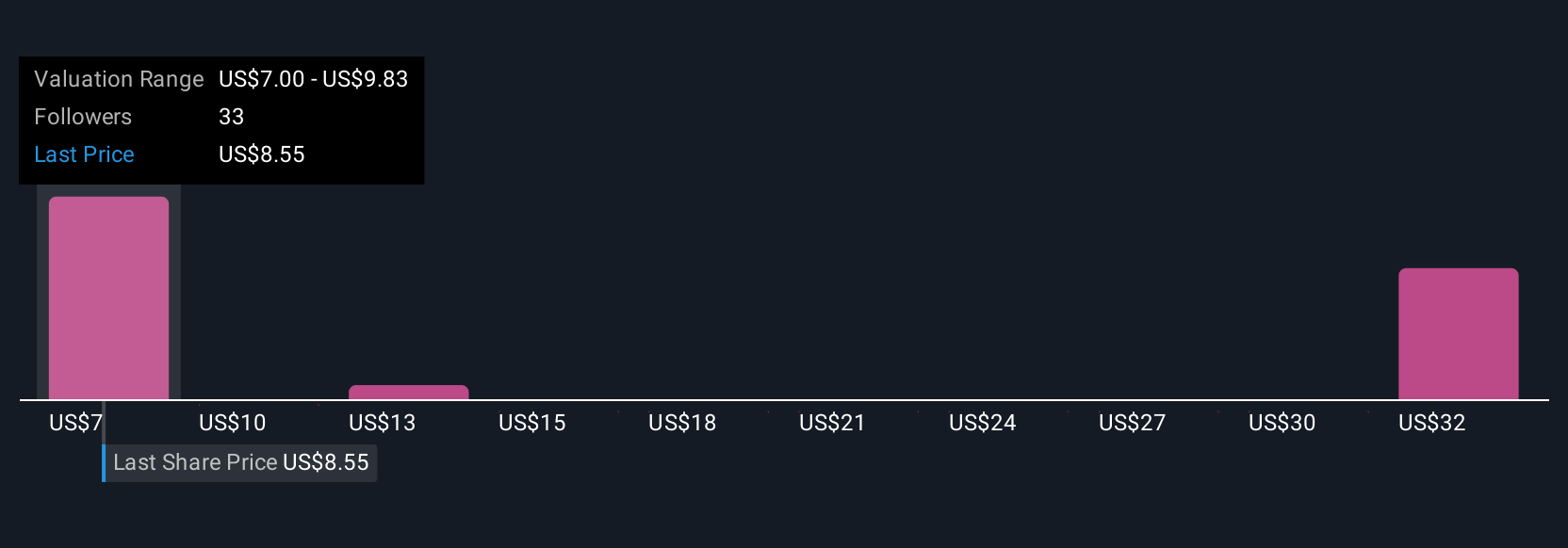

Nine Simply Wall St Community fair value estimates for Western Union range widely from US$7 to over US$35 per share. With revenue growth increasingly dependent on digital adoption in a crowded market, your own outlook on future performance may differ sharply from others, consider reviewing several viewpoints before making any decisions.

Explore 9 other fair value estimates on Western Union - why the stock might be worth over 4x more than the current price!

Build Your Own Western Union Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Western Union research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Western Union research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Western Union's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Western Union might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WU

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|54.3% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.2% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|25.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|51.4% overvalued

RO

Community Contributor