Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:UWMC

UWM Holdings (UWMC): Assessing Valuation After Third Quarter Earnings, Dividend Consistency, and Updated Guidance

Simply Wall St

Reviewed by Simply Wall St

UWM Holdings (UWMC) just reported its third quarter results, drawing attention with a smaller net loss than last year, a consistent quarterly dividend, and fresh guidance on production and gain margins for the months ahead.

See our latest analysis for UWM Holdings.

While UWM Holdings is managing smaller losses and steady dividends, the market’s mood has stayed cautious. The share price recently slipped to $4.96 and has dropped 12% year-to-date. However, the three-year total shareholder return is still up 50%, highlighting the stock’s sharp swings and long-term recovery potential.

If tracking resilient momentum or turnaround stories is your thing, now is the perfect time to broaden your scope and discover fast growing stocks with high insider ownership

With shares trading well below analyst targets and recent profitability improvements, investors are left wondering if UWM Holdings is an undervalued turnaround play or if the market has already adjusted for future prospects.

Most Popular Narrative: 29.1% Undervalued

With UWM Holdings closing at $4.96 and the most-watched narrative estimating fair value at $7.00, the gap signals outsized future potential if assumptions hold up. Let’s look at one of the drivers shaping this optimistic valuation.

Continued investment and successful deployment of advanced AI tools (like BOLT, ChatUWM, LEO, and Mia) are materially increasing broker productivity, efficiency, and borrower retention. This provides UWM with lower unit costs and the ability to handle significantly higher loan volumes without a proportional increase in costs, which should drive long-term revenue growth and operating margin expansion.

Curious how a blend of ambitious revenue growth, margin expansion, and future profit multiples drives this sharp fair value target? The most popular narrative hints at a growth trajectory rarely seen in this sector and relies on bold future projections. Click through and uncover which specific assumptions must come true to justify such a premium.

Result: Fair Value of $7.00 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent high interest rates or a shift in broker preferences could challenge UWM Holdings’ projected growth, which may affect future volumes and profitability.

Find out about the key risks to this UWM Holdings narrative.

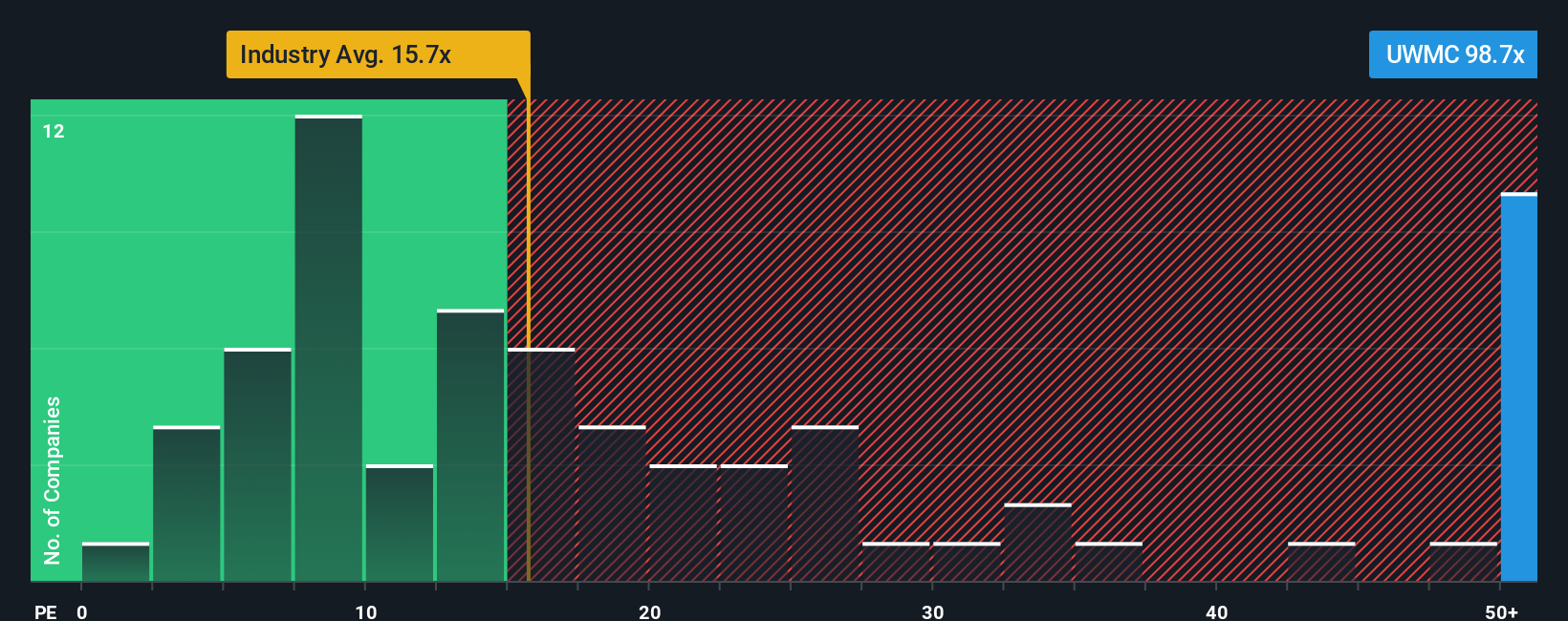

Another View: Valuation Using Earnings Multiples

Looking through the lens of earnings multiples, UWM Holdings appears expensive. Its price-to-earnings ratio is 74.8x, which is far above the US Diversified Financial industry average of 13x and its peer group at 9.5x. The fair ratio, which could signal where the market might shift, sits at 39.7x. These elevated levels might suggest heightened valuation risk if profit growth disappoints. Are investors paying too much for a turnaround story, or is the market anticipating years of outperformance?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own UWM Holdings Narrative

If you want to see a different angle or prefer diving into the numbers yourself, you can craft your own UWM Holdings outlook in just a few minutes. Do it your way

A great starting point for your UWM Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let the next big opportunity pass you by. Tap into proven strategies and outperform your peers by following expert-curated stock ideas that target unique angles within today’s market.

- Tap into the momentum of small companies shaking up the market when you check out these 3577 penny stocks with strong financials.

- Ride the wave of innovative medical breakthroughs by following leaders in smart healthcare with these 31 healthcare AI stocks.

- Boost portfolio stability and earn steady income with these 18 dividend stocks with yields > 3% for yields that go beyond what the average stock provides.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UWMC

UWM Holdings

Engages in the origination, sale, and servicing residential mortgage lending in the United States.

Exceptional growth potential with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

105 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

142 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative