- United States

- /

- Capital Markets

- /

- OTCPK:SCMT

Why You Might Be Interested In Sculptor Capital Management, Inc. (NYSE:SCU) For Its Upcoming Dividend

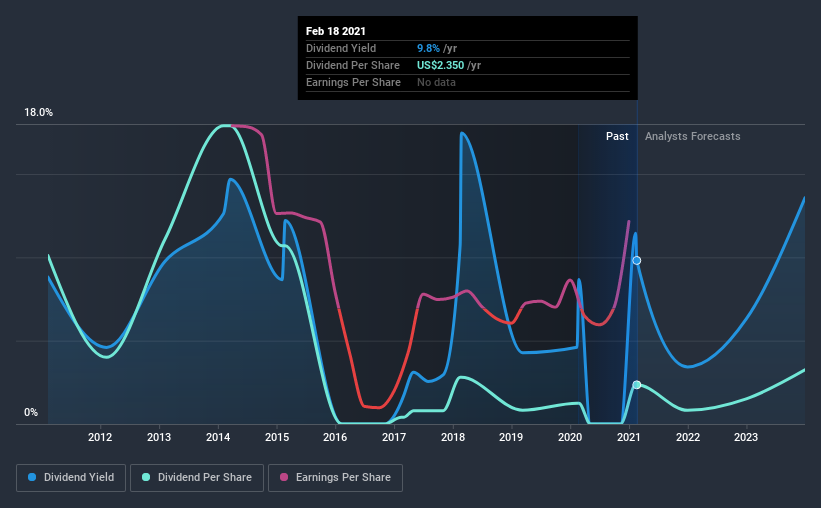

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Sculptor Capital Management, Inc. (NYSE:SCU) is about to go ex-dividend in just four days. Investors can purchase shares before the 24th of February in order to be eligible for this dividend, which will be paid on the 4th of March.

Sculptor Capital Management's next dividend payment will be US$2.35 per share, on the back of last year when the company paid a total of US$2.35 to shareholders. Looking at the last 12 months of distributions, Sculptor Capital Management has a trailing yield of approximately 9.8% on its current stock price of $23.95. If you buy this business for its dividend, you should have an idea of whether Sculptor Capital Management's dividend is reliable and sustainable. So we need to check whether the dividend payments are covered, and if earnings are growing.

See our latest analysis for Sculptor Capital Management

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Sculptor Capital Management is paying out just 7.0% of its profit after tax, which is comfortably low and leaves plenty of breathing room in the case of adverse events.

Generally speaking, the lower a company's payout ratios, the more resilient its dividend usually is.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. It's encouraging to see Sculptor Capital Management has grown its earnings rapidly, up 39% a year for the past five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Sculptor Capital Management has seen its dividend decline 14% per annum on average over the past 10 years, which is not great to see. It's unusual to see earnings per share increasing at the same time as dividends per share have been in decline. We'd hope it's because the company is reinvesting heavily in its business, but it could also suggest business is lumpy.

To Sum It Up

Has Sculptor Capital Management got what it takes to maintain its dividend payments? Companies like Sculptor Capital Management that are growing rapidly and paying out a low fraction of earnings, are usually reinvesting heavily in their business. Perhaps even more importantly - this can sometimes signal management is focused on the long term future of the business. Sculptor Capital Management ticks a lot of boxes for us from a dividend perspective, and we think these characteristics should mark the company as deserving of further attention.

So while Sculptor Capital Management looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. For example, we've found 4 warning signs for Sculptor Capital Management that we recommend you consider before investing in the business.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Sculptor Capital Management, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Sculptor Capital Management, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OTCPK:SCMT

Sculptor Capital Management

Sculptor Capital Management, Inc. is a publicly owned hedge fund sponsor.

Slightly overvalued with weak fundamentals.

Similar Companies

Market Insights

Community Narratives