Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:PIPR

Piper Sandler (PIPR): Assessing Valuation After Leadership Expansion and Private Markets Push

Simply Wall St

Reviewed by Simply Wall St

Piper Sandler Companies is making deliberate moves to strengthen its leadership and broaden its reach. The firm appointed Michael Piper as the new head of fixed income and expanded into private markets trading with three experienced managing directors.

See our latest analysis for Piper Sandler Companies.

Recent leadership moves and the firm's push into private market trading come as Piper Sandler’s year-to-date share price return sits at 12.22%. Still, its 1-year total shareholder return is essentially flat, even after a robust three-year gain of over 140%. Momentum appears steady, with investors weighing short-term stability against the long-term growth Piper Sandler has delivered.

Curious about what else is changing in the market? Now could be a smart time to broaden your investing lens and discover fast growing stocks with high insider ownership

With shares ticking higher so far this year but still trading below analyst price targets, the big question is whether Piper Sandler’s current valuation understates its upside, or if the market is already accounting for further growth.

Price-to-Earnings of 25.1x: Is it justified?

Piper Sandler shares currently trade at a price-to-earnings ratio of 25.1, placing them above both the broader US Capital Markets industry average of 23.8x and their peer group’s average of 7.5x. This higher multiple reflects what investors are paying for each dollar of the company’s earnings compared to its rivals.

The price-to-earnings ratio gauges how much investors are willing to pay today for expected future profitability. For Piper Sandler, a higher ratio might signal that the market anticipates continued earnings momentum, possibly supported by its seasoned management, recent strategic moves, and robust profit growth.

However, measured against industry and peer benchmarks, Piper Sandler’s valuation appears elevated. The market may be pricing in further success from its leadership strategy and previous earnings outperformance, rather than current earnings alone. With no fair-ratio guide available, investors need to dig deeper into the underlying assumptions supporting such a premium.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 25.1x (OVERVALUED)

However, weaker-than-expected revenue growth or a shift in the interest rate environment could quickly challenge Piper Sandler’s valuation premium and growth outlook.

Find out about the key risks to this Piper Sandler Companies narrative.

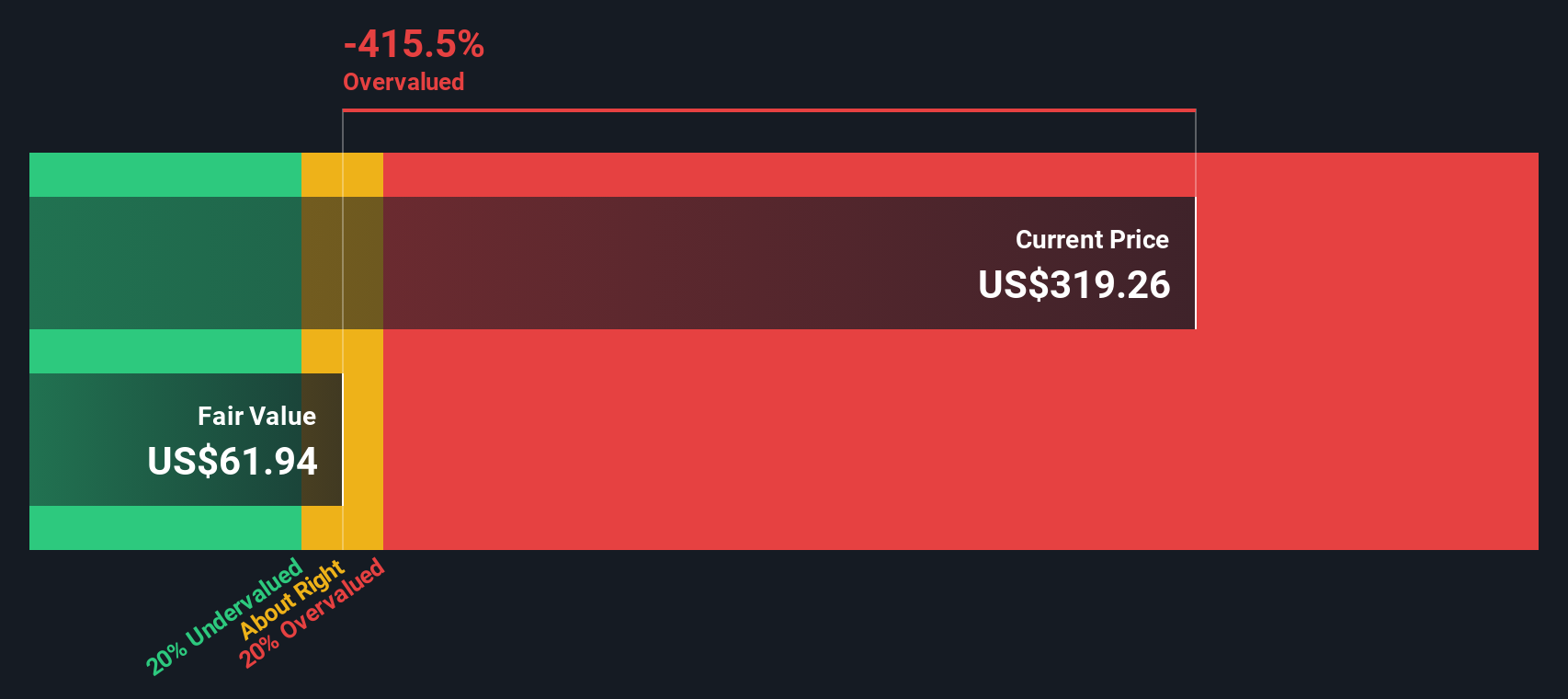

Another View: Discounted Cash Flow Sends a Dissenting Signal

While the market seems comfortable assigning Piper Sandler a higher price-to-earnings ratio, our DCF model presents a very different analysis. According to our calculations, the current share price is well above the estimated fair value of $61.05, suggesting notable overvaluation from a cash flow perspective. Is the optimism reflected in current prices a risk that investors should consider?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Piper Sandler Companies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 913 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Piper Sandler Companies Narrative

If you have a different perspective or want to dig into the numbers firsthand, you can assemble your own viewpoint on Piper Sandler Companies in just a few minutes. Do it your way

A great starting point for your Piper Sandler Companies research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Now is a great time to identify businesses that are shaping the future of various markets. Don’t let important opportunities pass you by.

- Capitalize on the increasing demand for healthcare innovation by starting with these 30 healthcare AI stocks which is supporting breakthroughs in AI-driven treatments and diagnostics.

- Enhance your income potential by exploring these 15 dividend stocks with yields > 3% which consistently offers attractive yields for those focused on long-term wealth building.

- Explore next-generation computing trends and discover which companies are leading advancements with these 28 quantum computing stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PIPR

Piper Sandler Companies

Operates as an investment bank and institutional securities firm that serves corporations, private equity groups, public entities, non-profit entities, and institutional investors in the United States and internationally.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

106 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

936 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

144 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative