Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:MCO

How Moody's (MCO) Strong Q3 Results May Shape Investor Expectations Amid Uncertain Markets

Simply Wall St

Reviewed by Sasha Jovanovic

- On October 22, 2025, Moody's Corporation reported third quarter earnings with sales reaching US$2.01 billion and net income rising to US$646 million, both higher than the same period last year, alongside improved earnings per share.

- This performance signals increased financial strength for Moody's and highlights its ability to deliver earnings growth even as questions remain around market stability and regulatory scrutiny.

- We will explore how Moody's strong quarterly results and higher profitability impact the company’s investment narrative and future outlook.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Moody's Investment Narrative Recap

To be a Moody’s shareholder, you need to believe in the company’s capacity to sustain recurring revenue and earnings growth as demand for risk assessment, especially in private credit and data analytics, expands. Moody’s latest quarter delivered solid top- and bottom-line gains, but this does not materially shift the primary catalyst, increasing private credit market penetration, or the biggest risk posed by heightened regulatory attention that could impact profit margins via new compliance demands.

Among recent announcements, Moody’s Board amended its By-Laws to clarify and update procedures for director nominations and stockholder proposals. While unrelated to earnings, this governance update is meaningful for investors focused on clear corporate processes and transparency, both of which can support confidence as Moody's scales in fast-moving financial sectors.

Yet, despite robust results, investors should remain alert to how regulatory scrutiny, in contrast to prior periods, may introduce unexpected costs or complexities that ...

Read the full narrative on Moody's (it's free!)

Moody's narrative projects $9.0 billion revenue and $3.0 billion earnings by 2028. This requires 7.3% yearly revenue growth and a $0.9 billion earnings increase from $2.1 billion.

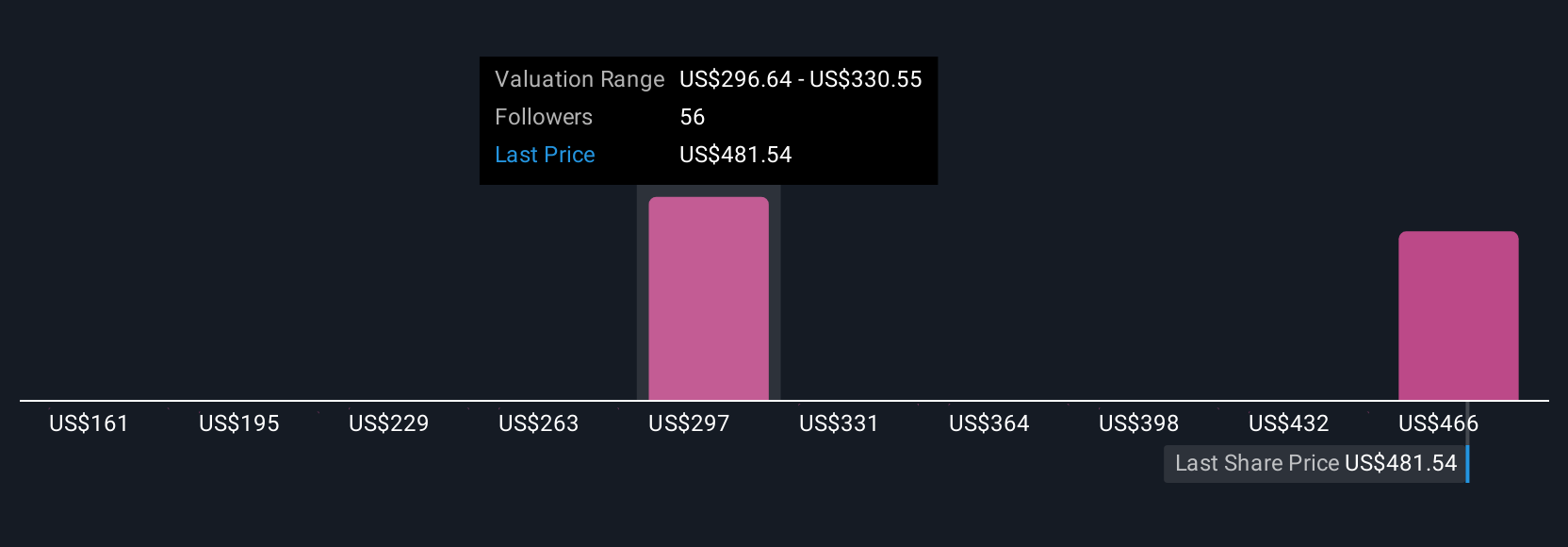

Uncover how Moody's forecasts yield a $545.50 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Nine separate fair value estimates from the Simply Wall St Community range from US$282.56 to US$545.50 per share. While your expectations may differ, it is important to keep in mind that new regulatory burdens remain the key risk that could impact Moody’s profitability and its outlook.

Explore 9 other fair value estimates on Moody's - why the stock might be worth as much as 12% more than the current price!

Build Your Own Moody's Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Moody's research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Moody's research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moody's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MCO

Proven track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor