Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:KKR

Is KKR’s $6 Billion Sallie Mae Deal Reshaping Its Long-Term Private Credit Strategy (KKR)?

Simply Wall St

Reviewed by Sasha Jovanovic

- Sallie Mae announced a multi-year private credit partnership with KKR, under which KKR will purchase over US$6 billion in private student loans over three years, while Sallie Mae continues servicing the loans and collecting fees.

- This collaboration signals KKR's expanding push into private credit markets and digital infrastructure as it also joins Corastone, a blockchain-based fintech aiming to improve private market transactions.

- We’ll explore how KKR’s partnership with Sallie Mae to acquire student loans could influence its long-term earnings growth narrative.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

KKR Investment Narrative Recap

To own shares of KKR, you need to believe in the long-term growth of private credit, asset-based finance, and the secular shift toward alternative investments. The newly announced Sallie Mae partnership expands KKR’s reach in private student loans, but in the near term, it does not significantly alter the key catalysts, such as fundraising momentum or fee growth, or address the main risk of asset quality and liquidity in an expanding private credit book.

One recent company announcement of interest, the affirmed quarterly dividend of US$0.185 per share, underlines KKR’s continued focus on shareholder returns. Consistent dividends remain important to investors, especially as KKR’s business model faces ongoing challenges from competition and fee pressure across private markets.

In contrast, investors should be alert to the increased exposure KKR has to asset quality and liquidity risks if secular growth trends in private credit...

Read the full narrative on KKR (it's free!)

KKR's narrative projects $13.7 billion revenue and $5.4 billion earnings by 2028. This requires a 13.9% annual revenue decline and a $3.4 billion earnings increase from $2.0 billion currently.

Uncover how KKR's forecasts yield a $157.17 fair value, a 31% upside to its current price.

Exploring Other Perspectives

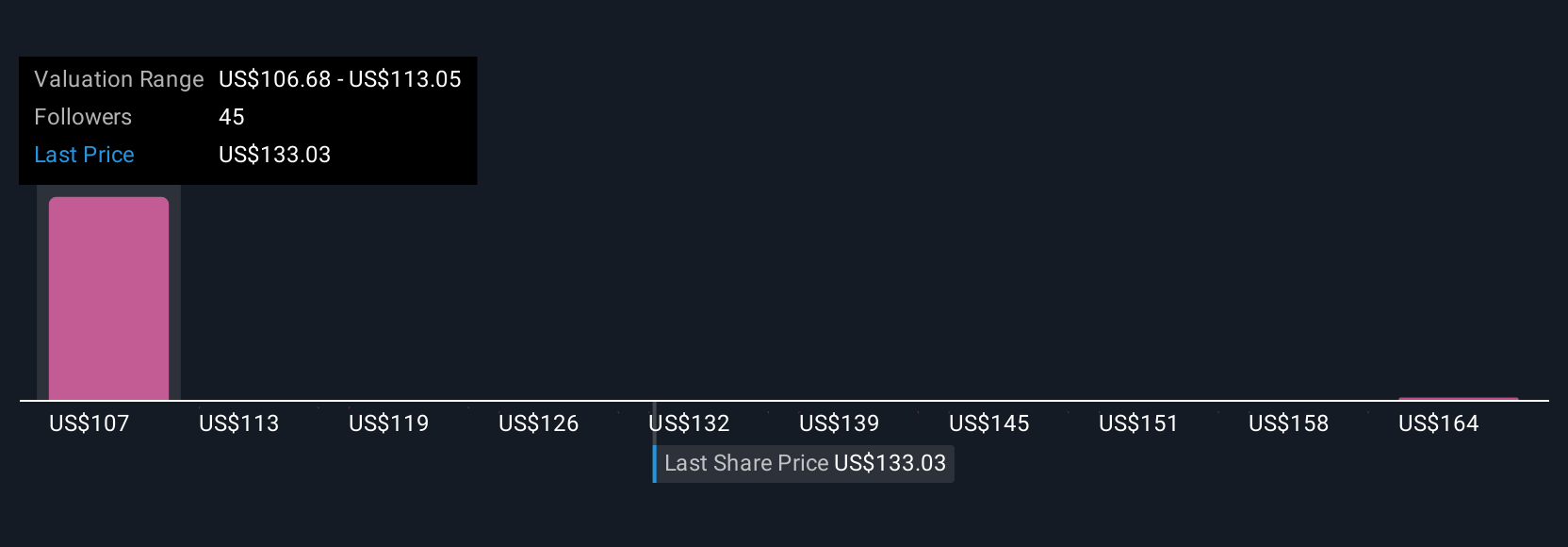

Simply Wall St Community members have set fair values for KKR ranging from US$57.95 to US$170.36, based on 5 independent perspectives. As fundraising momentum remains key to growing fee-paying assets, explore how differing views on growth potential could affect your outlook.

Explore 5 other fair value estimates on KKR - why the stock might be worth less than half the current price!

Build Your Own KKR Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your KKR research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free KKR research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate KKR's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KKR might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KKR

KKR

A private equity and real estate investment firm specializing in direct and fund of fund investments.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor