Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:KKR

A Fresh Look at KKR’s (KKR) Valuation Following Major UK Real Estate Investment

Simply Wall St

Reviewed by Simply Wall St

KKR (KKR) just backed a major UK logistics and industrial portfolio by providing a £350 million refinancing through its managed funds and accounts. This move gives Cain room to advance leasing efforts and highlights KKR’s long-term confidence in real estate fundamentals.

See our latest analysis for KKR.

Despite KKR’s strategic moves in real estate and the broader market, the stock price has come under pressure this year, with an 18.1% share price decline year to date. Over the past year, total shareholder return is down 23%, but the strong three- and five-year total returns of 152% and 220%, respectively, show that long-term performance and momentum remain impressive compared to shorter-term volatility.

If KKR’s recent shift in strategy has you curious about other opportunities, now might be the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

Given the sharp drop in KKR’s share price this year, while long-term returns remain robust and the stock still trades nearly 30% below average analyst targets, investors may wonder if there is more upside ahead or if future growth is already priced in.

Most Popular Narrative: 22% Undervalued

At $122.19, KKR’s share price sits well below the narrative-driven fair value of $157. This suggests there could be notable potential upside if key expectations are realized. Investors are watching for catalysts that could justify this valuation, especially as KKR navigates a demanding market environment.

Strong and accelerating fundraising momentum across asset classes, especially with institutional investors and the fast-growing private wealth/retail segment, are expanding fee-paying AUM and supporting double-digit management fee growth. Further upside may come from new distribution initiatives. This is likely to positively impact future revenue and management fees.

Want to know what’s driving the lofty target behind this discount? This narrative assumes a dramatic earnings turnaround and profit margins rarely seen in the industry. The boldest projections lie in how fast KKR can ramp revenues and fees while scaling high-growth platforms. Curious what these numbers could mean for your own investment thesis? Unlock the analysis that justifies this eye-catching valuation.

Result: Fair Value of $157 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent credit concerns and tougher competition in alternative asset management could challenge KKR’s momentum and introduce more volatility to future returns.

Find out about the key risks to this KKR narrative.

Another View: Multiples Paint a Pricier Picture

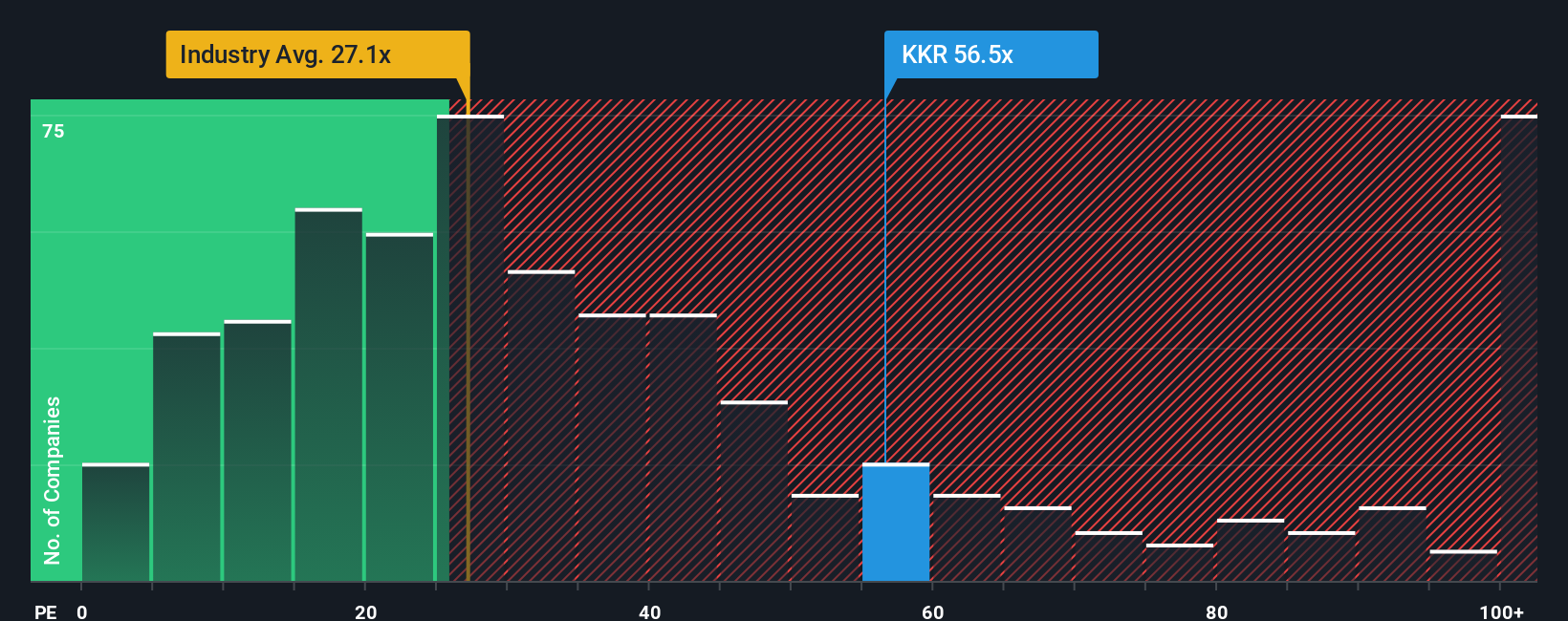

While the narrative-driven valuation provides an optimistic outlook, the current price-to-earnings ratio stands at 47.9x. This is nearly double the US Capital Markets industry average of 23.8x and well above the peer average of 35.3x. The fair ratio, based on regression analysis, is 26.6x. This suggests KKR’s shares are trading at a significant premium. For investors, this puts valuation risk in sharper focus, especially if growth targets are not reached. Is the premium justified, or should caution take center stage?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own KKR Narrative

If you have a different perspective or want to dig into the numbers yourself, you can build your own analysis and narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding KKR.

Looking for More Smart Investment Opportunities?

Every investor needs an edge. Tap into new trends and resilient sectors using handpicked shortlists from the Simply Wall Street Screener to strengthen your portfolio and spot tomorrow’s winners today.

- Earn higher yields by reviewing these 14 dividend stocks with yields > 3% and find companies offering the most attractive income streams above 3%.

- Accelerate your growth plans by tapping into these 25 AI penny stocks which are positioned to transform industries with advanced artificial intelligence breakthroughs.

- Step into the future of banking and decentralized finance with these 81 cryptocurrency and blockchain stocks already shaking up the digital economy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KKR might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KKR

KKR

A private equity and real estate investment firm specializing in direct and fund of fund investments.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.3% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

HA

Haha94 on Perdana Petroleum Berhad ·

Perdana Petroleum Berhad is a Zombie Business with a 27.34% Profit Margin and inflation adjusted revenue Business

Fair Value:RM 0.2128.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AB

Abc on Global X Etfs Icav - Global X Silver Miners Ucits ETF ·

Many trends acting at the same time

Fair Value:€10068.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

941 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative