Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:JXN

Is Jackson Financial Still a Bargain After a 4.3% Weekly Price Jump?

Simply Wall St

Reviewed by Bailey Pemberton

- If you’ve ever wondered whether Jackson Financial stock is truly a bargain or just looks cheap, you are in the right place for some clear, actionable insights.

- Over the past week, the stock has jumped 4.3%, adding to an 11.5% gain since the start of this year. Its one-year return is a more modest 1.1% following a significant multi-year rally.

- Behind these price moves, headlines have focused on Jackson Financial’s consistent strategy in the shifting interest rate environment and its recent push into new annuity products. This has sparked fresh debate among investors about sustainable growth versus shifting industry risks.

- When it comes to valuation, Jackson Financial scores a 5 out of 6 in our systematic checks. See the full breakdown here. However, numbers only tell part of the story, so let’s explore how different valuation methods compare and why there may be a better way to assess the company’s future at the end of this article.

Approach 1: Jackson Financial Excess Returns Analysis

The Excess Returns valuation method looks at how much profit a company generates above its cost of equity. This approach focuses on return on invested capital and long-term growth in shareholder value. For Jackson Financial, it highlights the company’s efficiency in turning its equity into earnings and sustainable value over time.

Key measures from the model show a Book Value of $141.89 per share and a Stable EPS of $16.71 per share, based on the median Return on Equity from the past five years. The Cost of Equity is $13.26 per share, so Jackson Financial’s Excess Return is $3.45 per share. The company’s average Return on Equity stands at 9.49%. Looking ahead, the Stable Book Value is projected at $176.05 per share according to future estimates from two analysts.

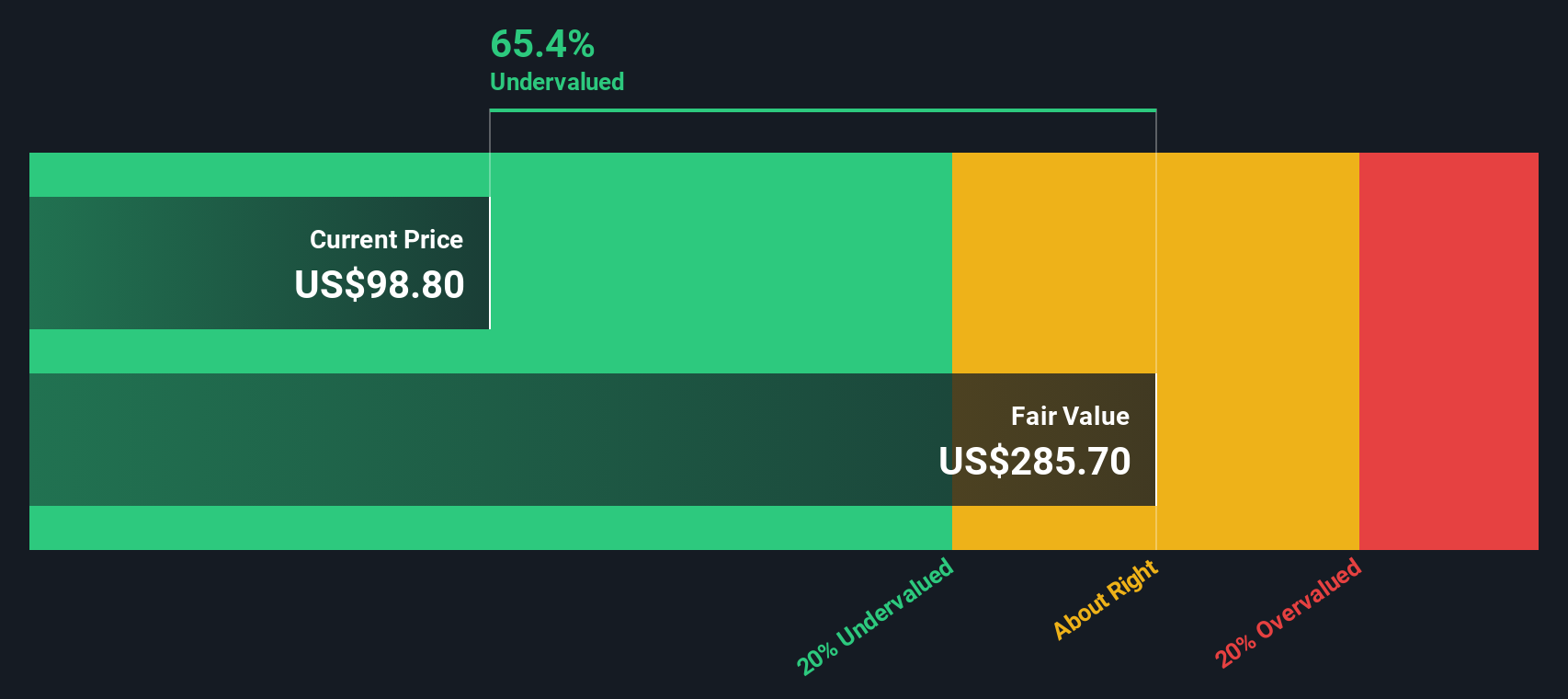

Based on these inputs, the Excess Returns model estimates an intrinsic value that implies Jackson Financial stock is 61.9% undervalued against its current market price. The substantial gap between intrinsic value and share price suggests the market may be overly cautious or overlooking the company’s profitability and consistent equity returns.

Result: UNDERVALUED

Our Excess Returns analysis suggests Jackson Financial is undervalued by 61.9%. Track this in your watchlist or portfolio, or discover 933 more undervalued stocks based on cash flows.

Approach 2: Jackson Financial Price vs Earnings

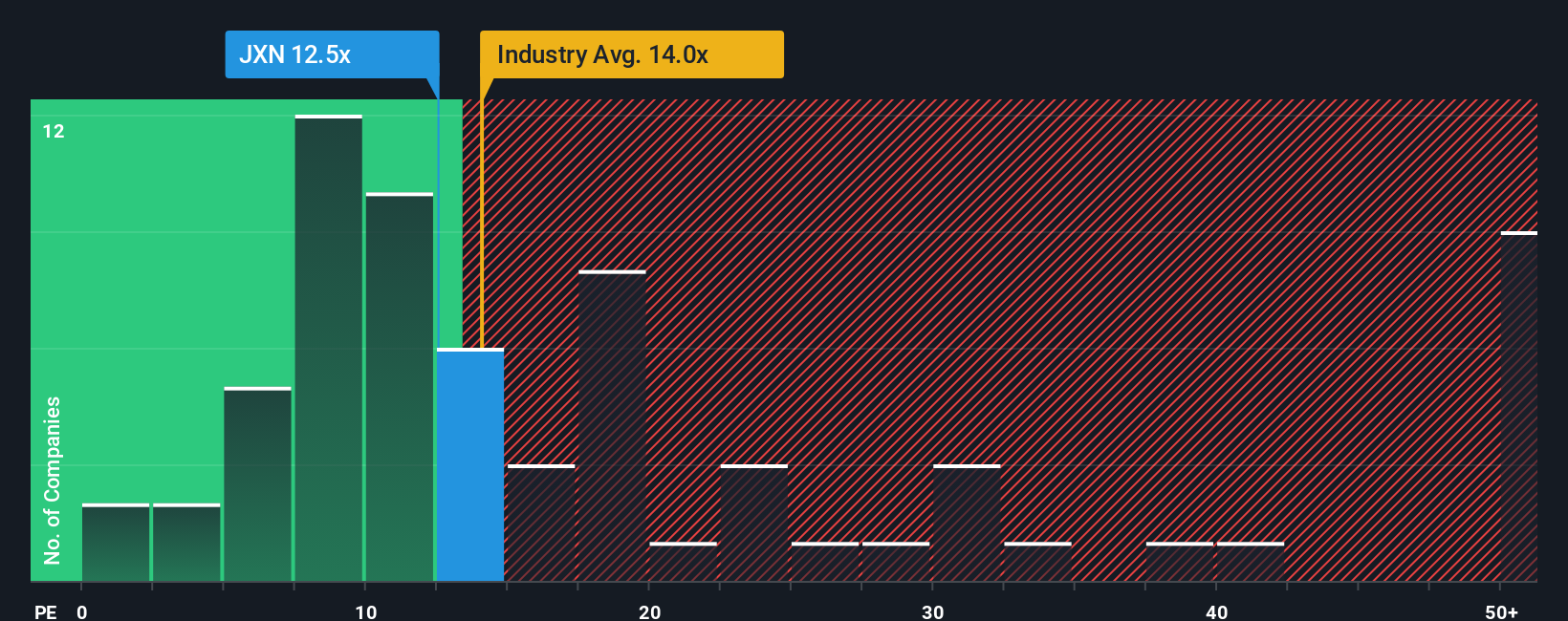

The Price-to-Earnings (PE) ratio is a widely accepted valuation tool for assessing profitable companies like Jackson Financial. It gives investors a quick sense of how much they are paying for each dollar of earnings, making it especially useful for established firms with steady profit streams. When a company is consistently profitable, the PE ratio reflects both current performance and market expectations for the future.

Growth expectations and perceived risk play a major role in what constitutes a "normal" or "fair" PE ratio. Companies expected to grow faster, or those considered safer, often justify higher PE multiples. In contrast, more volatile or slower-growing firms typically see lower ratios.

Currently, Jackson Financial’s PE ratio is 12.5x. This is below both the broader Diversified Financial industry average of 13.6x and the peer average of 14.3x. Simply Wall St introduces the concept of a "Fair Ratio," in this case 15.9x, which is tailored for Jackson Financial’s unique characteristics such as earnings growth, profit margin, industry context, market cap, and company-specific risks.

The Fair Ratio provides a more accurate benchmark than just using broad industry or peer averages. It looks beyond headline numbers and incorporates a wider view of the company’s strengths and weaknesses, ensuring investors do not overlook important factors like future growth prospects and risk profile.

Comparing Jackson Financial’s current PE of 12.5x with its Fair Ratio of 15.9x suggests the stock remains attractively priced. This indicates that the market may not be fully recognizing the company’s earnings potential and risk-adjusted value.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Jackson Financial Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your own story or perspective about a company’s future, beyond just the numbers. It is where you explain why you believe certain revenue, earnings, or margin forecasts are likely and tie those expectations directly to your idea of fair value.

Narratives bring investing to life by connecting a company’s real-world story to a financial forecast and then to a clear fair value, making the decision process more personal, intuitive, and actionable. They are easy to create and share directly within Simply Wall St’s Community, where millions of investors post, debate, and refine their Narratives every day.

This hands-on approach helps you decide whether it is time to buy or sell by letting you compare your own Fair Value with the latest market price. Narratives remain dynamic, automatically updating with new news or earnings reports, so your decisions stay relevant and well-informed.

For example, one Jackson Financial Narrative may be optimistic about continued annuity demand and margin expansion, supporting a fair value of $118 per share. Another narrative might highlight regulatory and competitive risks and value the stock closer to $95. Which one fits your view?

Do you think there's more to the story for Jackson Financial? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:JXN

Jackson Financial

Through its subsidiaries, provides suite of annuities to retail investors in the United States.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative