Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:EVR

Evercore (EVR): Exploring Valuation After Recent Share Price Pullback and Strong Financial Results

Simply Wall St

Reviewed by Kshitija Bhandaru

Evercore (EVR) has caught attention lately, with investors keeping an eye on its recent stock movement and solid financial results. Its steady revenue and net income growth provide an interesting backdrop for those following the financial sector.

See our latest analysis for Evercore.

Evercore has seen its share price slide 11.96% over the past month, giving back some of its earlier gains. Long-term investors have still enjoyed a 14.7% total shareholder return over the past year and over 250% over three years. This recent pullback comes after a strong run and suggests the market is pausing to reassess growth expectations in light of Evercore's ongoing financial momentum.

If you're curious to see what else is catching investors’ attention in fast-moving markets, now is a great moment to discover fast growing stocks with high insider ownership

With Evercore’s impressive revenue and net income growth, yet a recent dip in share price, the question remains: Is the recent pullback a rare buying opportunity, or is the market already factoring in Evercore’s future prospects?

Most Popular Narrative: 18% Undervalued

Evercore’s widely followed narrative assigns a fair value notably above its most recent closing price, signaling ongoing optimism among analysts. This perspective draws on anticipated advisory revenue growth, margin improvement, and the effects of international expansion, providing context that frames the outlook for Evercore’s shares.

The ongoing globalization of capital markets and an accelerating trend in cross-border M&A activity are providing an increasingly fertile environment for independent, conflict-free advisors like Evercore. The firm's continued expansion into key international markets, as evidenced by new offices and hiring in EMEA (France, Spain, Italy, Dubai, UK), positions it to capture an increasing share of growing advisory fee pools and drive top-line revenue over the long term.

Curious about the math powering this bullish outlook? There’s a bold projection for earnings, revenue, and profit margins at the core of this fair value call. Find out which assumptions tip the balance toward Evercore’s global ambitions and forecasted growth surge; the details may surprise you.

Result: Fair Value of $369 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising fixed costs and increasing competition in key segments could pressure margins and limit Evercore’s revenue growth if market conditions change.

Find out about the key risks to this Evercore narrative.

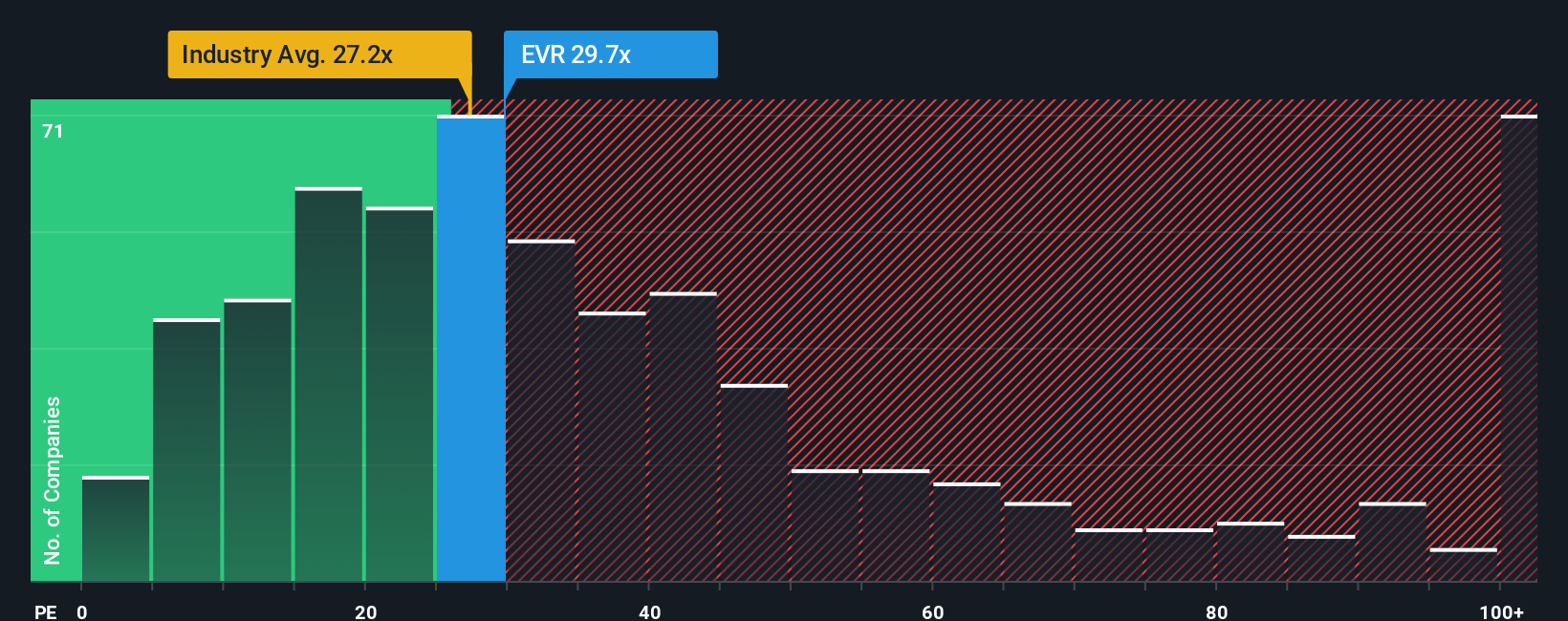

Another View: Market Ratios Raise Questions

Looking through another lens, Evercore trades at a price-to-earnings ratio of 25.1x, which is just above the US Capital Markets industry average of 24.9x and notably ahead of close peers at 19.3x. That is also higher than the fair ratio of 20.8x, offering less margin for error if growth slows. If the market’s optimism fades, could the premium valuation be at risk?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Evercore Narrative

If you see things differently or want to chart your own course, it takes just minutes to analyze the data yourself and create a custom perspective. So why not Do it your way?

A great starting point for your Evercore research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let the next big opportunity pass you by. Simply Wall Street’s screener helps you pinpoint standout stocks before the crowd catches on.

- Unlock potential with these 3585 penny stocks with strong financials, which offer strong financials that could fuel tomorrow’s top performers.

- Spot high yields by checking out these 19 dividend stocks with yields > 3%, featuring companies with consistent dividend payouts above the market average.

- Seize the momentum in next-gen technology by targeting these 24 AI penny stocks, which are transforming industries through artificial intelligence breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evercore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EVR

Evercore

Operates as an independent investment banking firm in the Americas, Europe, Middle East, Africa, and Asia-Pacific.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

934 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative